Stocks Are Getting Cheaper

In his 1997 letter to Berkshire Hathaway shareholders, Warren Buffet explained why declining stocks are good news for long-term investors:

If you plan to eat hamburgers throughout your life and are not a cattle producer, should you wish for higher or lower prices for beef?

Likewise, if you are going to buy a car from time to time but are not an auto manufacturer, should you prefer higher or lower car prices?

These questions, of course, answer themselves. But now for the final exam: If you expect to be a net saver during the next five years, should you hope for a higher or lower stock market during that period?

Many investors get this one wrong. Even though they are going to be net buyers of stocks for many years to come, they are elated when stock prices rise and depressed when they fall. In effect, they rejoice because prices have risen for the “hamburgers” they will soon be buying. This reaction makes no sense. Only those who will be sellers of equities in the near future should be happy at seeing stocks rise. Prospective purchasers should much prefer sinking prices.

To be clear, we don’t enjoy price declines any more than anyone else. Even for investors with a very long time horizon, it can be painful to watch the erosion of portfolio gains. Even worse, market declines have a way of nudging investors into making unforced errors (e.g. selling at precisely the wrong time). Long-time clients may feel we are overstating the obvious, but this is only because of how important this concept is in investing. The price you pay determines your return; lower is better all else being equal.

The beauty of lower prices should be self-evident for those who are accumulating stocks and other investments, whether by increased savings or through the reinvestment of portfolio income. But what about those in the decumulation phase – namely retirees? The math here is less simple. Drawing down a portfolio into a decline can exacerbate the portfolio drawdown and reduce the longevity of the portfolio. Individual circumstances like other sources of income (pension, social security, rental income, etc.), budget flexibility, and general tolerance for risk certainly play a role. Retirees with a healthy tolerance for risk may benefit more from greater portfolio appreciation during bull markets – which historically last longer and provide greater returns relative to more conservative bonds.

In addition to greater appreciation potential during bull markets, stocks that pay dividends, and regularly increase the dividends paid to shareholders are providing income that can help support portfolio distributions. Nevertheless, most retired investors will generally look to have a mixture of stocks, bonds, and other income-oriented instruments in their portfolios. The bad news here is that “conservative” bonds have provided mostly paltry returns over the last decade plus. 2022 has added a certain “insult to injury” to conservative bond investors as bonds have swooned alongside the persistently high inflation.

But this bad news for bonds may be slowly turning to good news, as higher bond yields are beginning to provide a more fair rate of return to conservative investors. As of this writing, a short-term 1 year US treasury note was paying 4.5%. These are yields that haven’t been seen since the early 2000s, and now offer conservative savers better options for the ballast portion of their portfolio. For investors in high-quality bond funds, the price declines this year have been some of the worst on record; however shorter duration bond funds should ultimately find their footing as portfolio holdings mature, and are likely reinvested at higher interest rates.

Why not just go to cash and wait for prices to go lower?

When times are tough, investors always want to find ways to limit the downside. But limiting the downside is really just synonymous with selling your stocks when markets are down. Investors rarely want to limit the downside when markets are booming. Sure selling after a 25% decline in markets could mean avoiding the next 25% decline – but there is no certainty that there will be another decline near that magnitude. Selling also creates a psychological problem where the seller, waiting for the right time to get back in, now roots for more downside – they certainly won’t want stocks to go up after they’ve sold. Every rally then is met with reasons why this is just a fake out, and further declines are bound to come. This makes it extremely challenging for the market timer to turn bullish at the right time.

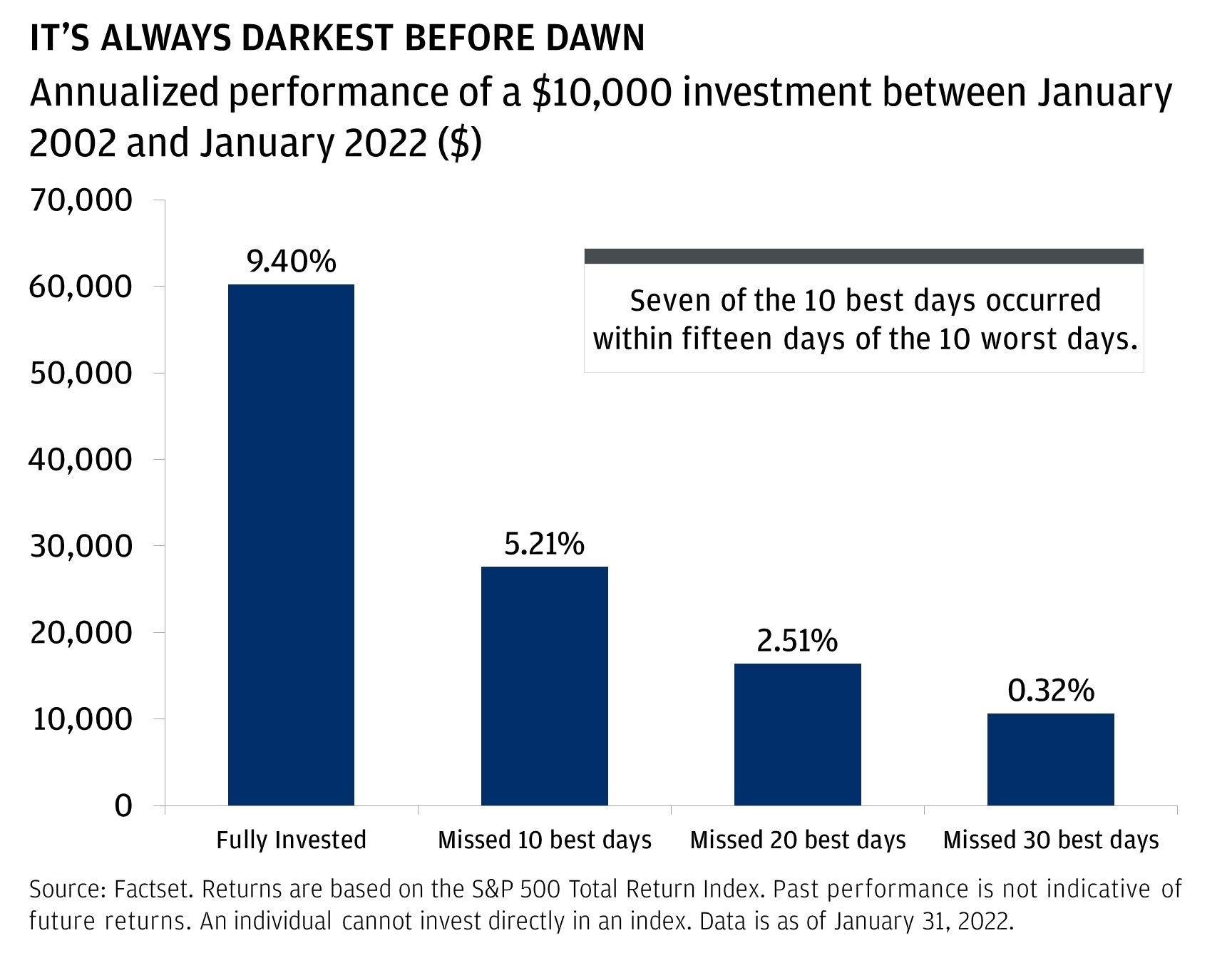

Perhaps the biggest reason not to sell everything and go to cash can be gleaned from market history. Strong up days for the stock market are often clustered around big down days. According to research from JP Morgan, over the past 20 years (as of 1/31/22) seven of the best 10 days for the stock market (S&P 500) occurred within just two weeks of the 10 worst days. Further, missing the 10 best days in total would have resulted in an annual market return of 5.21% vs. 9.40% for a portfolio that had stayed fully invested in the market over the entire time frame (Exhibit A).

Exhibit A.

Click to enlarge.

Year-to-Date Review & Outlook

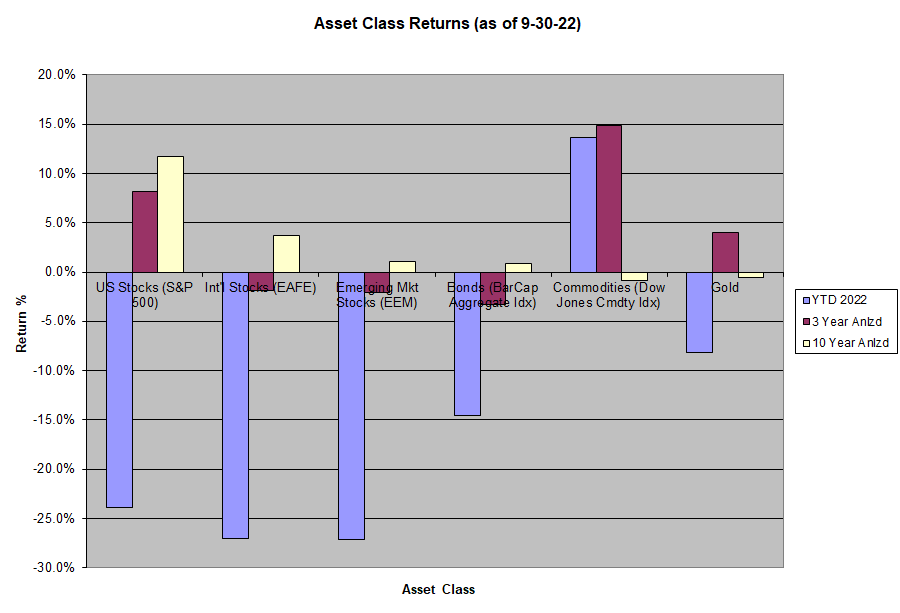

Year-to-date through 9/30/22:

- Domestic stocks (S&P 500) declined 23.9%

- Developed international stocks (EAFE) declined 27.1%

- Emerging market stocks (EEM) declined 27.2%

- Bonds (Bar Cap Aggregate) declined 14.6%

- Commodities (DJCI) were up 13.6%

- Gold declined 8.2%

We have updated our asset class return chart to reflect year-to-date returns through June, along with three and ten year annualized returns for the aforementioned asset classes.

Click to enlarge.

The third quarter began with a strong rally. By mid-August the S&P 500 was up ~ 14% from the end of June. However by the end of the quarter ongoing concerns about persistent inflation and Federal Reserve hawkishness had reasserted themselves, with markets closing near the lows for the year by the end of September. We have not materially changed our outlook from our Q3 client communication, and still give higher odds to a “soft landing”. Asset prices have already adjusted a great deal to this new regime of higher rates and stickier inflation. A combination of good news and/or incrementally less bad news could be poised to lift both markets and investor sentiment. Consider:

- Peak inflation: Since March, the price of crude oil has declined 40%, a broad based commodities index (S&P GSCI) is down 30%, and the 10 year US breakeven inflation rate has dropped to 2.19% (barely above the Fed’s long-term target).

- Peak Fed Hawkishness: The Federal Reserve has raised rates quicker than at any time in the last 40+ years. Saint Louis Federal Reserve President James Bullard has recently commented in public about the possibility of 2 more hikes (one each at the November and December Federal Open Market Committee meetings), then pausing and taking a “wait and see” stance on 2023 (from Yardeni Research). The end of rate hikes could be within sight.

- Valuation: The S&P 500 P/E multiple has contracted by ~ 7 points as of the time of this writing. This is unsurprising given the gravitational pull that interest rates have on valuation. But stocks now trade at much more reasonable valuation levels. A good amount of bad news may be priced in, while any good news on the inflation front may spark an expansion in multiples (i.e. higher stock prices).

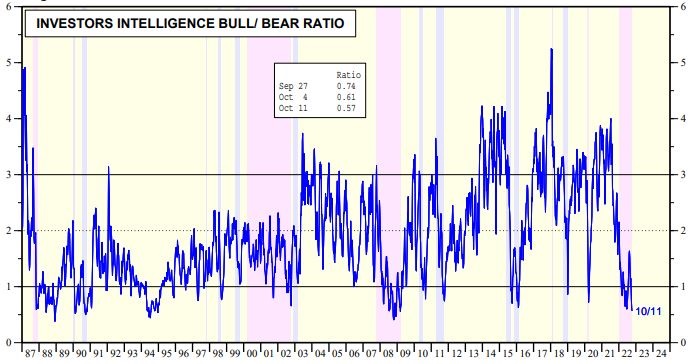

- Sentiment: Ironically the brightest spot of all could be the sheer level of negativity in markets. For the week of October 11, 2022 the Investors Intelligence Bulls & Bears ratio hit a level of .57 (Exhibit B), the lowest level since the nadir of the Great Financial Crisis in March 2009. That was arguably the best time to buy stocks in a generation. While this indicator can stay depressed during lengthy bear markets, readings below 1.0 have historically indicated good buy levels for long-term investors.

- Election cycle: mid-term elections tend to be weaker for the stock market, and so far 2022 has been no exception. According to research from Bespoke Investment Group, stocks return 5% less on average in mid-term election years than in non-mid-term years (date going back to 1946). Further, mid-term election years tend to have larger maximum peak to trough sell off’s with these declines averaging -16.6% vs. -10.8% for non-mid-term years. The good news, according to equity strategists at Strategas, since 1946 U.S. stocks have never traded lower 12 months after a mid-term vote, and have averaged gains over that time frame of 15% excluding dividends.

Exhibit B

Source: Investors Intelligence; Yardeni Research, Inc.

Note: Shaded red areas are S&P 500 bear market declines of 20% or more. Blue shaded areas are correction declines of 10% to less than 20%. Yellow areas are bull markets.

One might call the above a bullish wish list, and there is no certainty or guarantee any of the above will come to pass. The market may very well have more to fall and/or more time to pass before it transitions to a new bull market. But with sentiment so negative, it is important to remember what could go right in the quarters and years to come.

Should you have any questions regarding your investment account(s) and personal financial plans, or if there have been any recent changes to your investment and/or retirement objectives, please contact our office. We can also provide you with a current copy of our SEC Form ADV Part 2, at your request. As always, we thank you for entrusting AMM to help you achieve your investment and retirement objectives.

Your Portfolio Management Team

Individual accounts will vary based on a client’s stated investment objectives, risk tolerance, and time frame. We manage several different strategies, so not every client will have exposure to the securities, asset classes, or investment strategies described above. In addition to growth and/or income-oriented asset allocation strategies, we also manage more concentrated equity portfolios that generally carry a higher degree of risk and volatility.