AMM First Quarter 2019 Client Letter

The 4th quarter of 2018 saw one of the largest jumps in volatility in years. The reasons for the volatility are now widely “known”. Political uncertainty, trade uncertainty, fears of a policy error by the Fed, earnings uncertainty, presumed increase in recession risks, etc. Interestingly, all of the aforementioned risks were present prior to the 4th quarter, but this is nature of markets. Risks go from being over-priced to underpriced without any rhyme or reason as to why. Markets are less like a well-greased machine than they are a temperamental three year old. Sometimes moody, sometimes elated, rarely rational and never predictable.

Perhaps what we saw in the 4th quarter of 2018 was truly a sign of a market predicting a looming recession. But equally as likely, in our opinion, is that this action was a healthy de-risking. Healthy in that a bubble can’t burst if there is no bubble. Market corrections and bear markets are normal. They introduce caution in to the market narrative and price investment assets back to reasonable levels. This isn’t bad – for the long-term investor.

We don’t mean to downplay current market risks, but to point out that risk is always present in markets. What varies is how much risk is priced in at any point in time. The riskiest markets are bubbles where risks are vastly underappreciated – and we would argue that we aren’t in that kind of market today. A spike in volatility re-prices investments in accordance with new or underappreciated risks. At some point the market finds an equilibrium where risk and reward are fairly balanced.

Recession Watch 2019

The reality is that a recession will occur again at some point in the future. Whether this is caused by a trade war, overly hawkish fed, or some unknown exogenous event, the business cycle will at some point shift from expansion to contraction. While most economists expect GDP growth to slow this year, few expect an outright recession. Unemployment is low, and interest rates, though rising, remain very low by historical standards. While this is now the longest post war expansion on record, it is also the weakest. Some argue a “lower for longer” outcome for this economic cycle – meaning that the expansion will last much longer than the post-war average but at a lower level of growth.

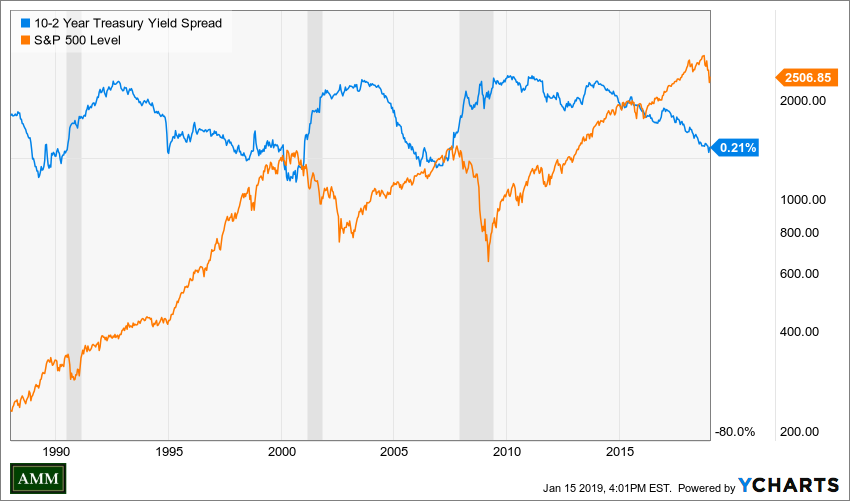

One of the more widely watched recession indicators is the spread between 10 year and 2 year treasury notes (blue line in exhibit A below – shaded areas indicate recessions). When the spread turns negative this is meant to indicate a recession is near. A negative yield spread has preceded every recession since 1956. The basic theory is that when short-term interest rates exceed long-term rates, market sentiment suggests that the long-term outlook is poor and that yields offered by long-term fixed income will continue to fall. Effectively investors are eschewing purchasing growth oriented long-term assets like stocks and buying, and thereby reducing the yields, on more conservative longer term bonds.

While inverted yield curves have a strong predictive track record, there is one big problem. They don’t provide any reliable prediction of how deep the recession will be, or more importantly to investors, how bad the market reaction will be. Will the next recession result in a mild 15% market correction like the early 1990s recession? This is barely a blip on the chart above. Or will it be a long drawn out affair like the bursting of the tech bubble in 2000?

There are other indicators worth watching to get an overall sense of where we are in the business cycle, but none of them help in terms of providing what everyone really wants to know. How bad will it be, when do I get out, and when do I get back in? This makes a kind of perverse sense. If such an indicator existed, everyone would use it and we’d likely already be in a recession because the indicator would have become a self-fulfilling prophesy. Which leads us to our most important point: like the temperamental three year old – markets are naturally meant to disappoint, frustrate and confuse as many participants as possible.

For these reasons we avoid making portfolio decisions based solely on price action or on a “predictive” indicator. Instead we have developed 5 core principles that help guide the day to day management of client portfolios. These principles are evergreen – and are applied to client portfolios regardless of market conditions.

Five Core Principles

Asset Allocation is the Most Important Decision: The decision of how much of your portfolio to invest in stocks, bonds, real estate and other asset classes is the primary factor in both the long-term return and level of fluctuation in your portfolio. More stock generally equals greater long-term returns but higher volatility vs. a more bond heavy portfolio. Determining the appropriate allocation for your unique time horizon, tolerance for volatility and portfolio objectives is the critical first step in managing your portfolio.

Volatility is Not Risk: Real risk is the likelihood of permanent capital impairment. This is our biggest concern when investing client money. Volatility or the second to second fluctuation of your account is not the truest definition of risk. Volatility is only “risky” to the degree that it causes investors to make a decision that causes permanent capital impairment. The real risk of volatility is that it spooks investors to abandon a well thought out investment policy and sell out of a fundamentally sound position at a loss. Making matters worse, the financial press and market pundits tend to treat every bout of volatility as if it is news of great import that requires ACTION now. We don’t suggest investors ignore risk – just that they focus on the right risk (i.e. odds of capital loss).

The Price you Pay Determines your Return: Pay too high a price for any asset and your return goes down and risk goes up. Investor Howard Marks famously said, “there are no bad investments, just bad prices”. Take for example the experience of investors in CSCO in the late 1990s (exhibit B). Investors purchasing CSCO at a nosebleed earnings multiple of 198 at the end of 1999 would have paid ~ $53 per share. Today the stock trades for $43, and even with dividend reinvestment shareholders would not have made money in this stock over the last 18 years. But over the same time the company has nearly tripled their earnings (EBITDA). The stock simply performed poorly because all of that future earnings growth (and then some) was baked in to the price in late 1999. This is an example of a good company (competitive advantages, good earnings growth) but bad stock investment – if bought in late 1999. To help minimize this kind of outcome we focus on investing only at prices that make economic sense. The quality and prospects of a business matter, but price matters too!

Time is your Ally but Returns are Not Linear: At the end of 2009 investors in an S&P 500 index fund had endured 10 long years of negative annualized returns. $10,000 theoretically invested in the S&P 500 on the last day of 1999 had turned in to $9,089 10 years later. One can’t blame an investor for bailing on stocks at that time – they appeared to not work anymore. But 9 years later as of the end of 2018, that same initial investment of $10,000 would now be worth $23,375 more than double the original value. Asset class returns come from being invested, and your odds of making money increase greatly the longer you are invested.

No one can predict the future: Investors too often develop a prediction and then marry themselves (and their portfolio) to the predicted outcome. In complex systems like the stock and bond markets, the likelihood that you make an error by not fully incorporating all of the potential variables that will affect your prediction is very high. Add to this the probability that even if your prediction is right, it may be wrong for a long-time before it is right. This may lead to a behavioral error of abandoning your otherwise appropriate investment at the wrong time. Married to one outcome almost ensures failures. Instead of investing on predictions, we focus on trying to understand the present and then invest accordingly. This generally means focusing on odds and making portfolio adjustments at the margin, as opposed to big all or nothing decisions.

2018 Review & 2019 Outlook

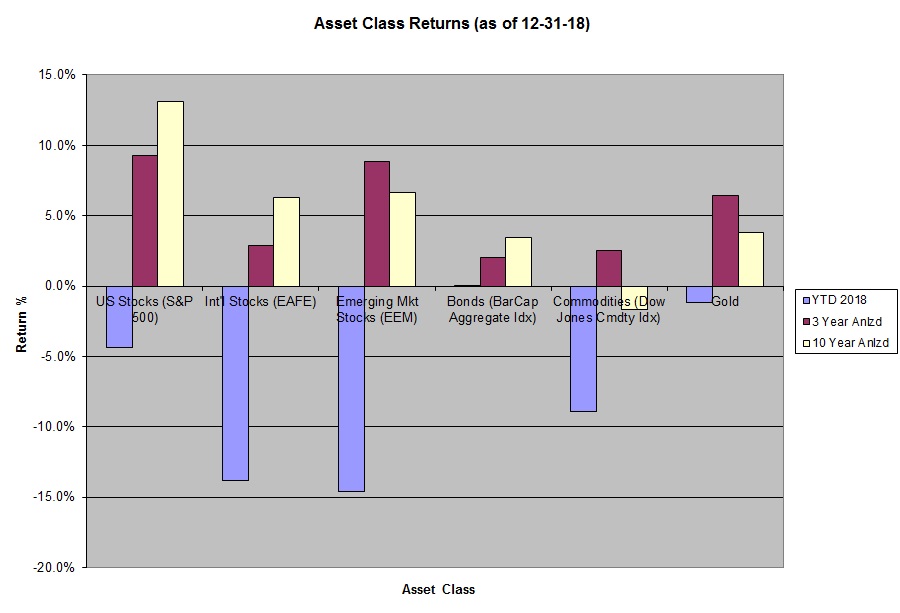

For the year ending 12/31/18, domestic stocks (S&P 500) declined -4.4%, developed international stocks (EAFE) declined -13.8%, and emerging market stocks (EM) declined -14.6%. Bonds (Bar Cap Agg Idx) were flat, commodities declined -8.9% and gold declined -1.2%. We have updated our asset class return chart (Exhibit C) to reflect YTD 2018 along with three and ten year annualized returns for the aforementioned asset classes.

Two things can be said about investing in 2018: 1) It was a bad year for asset class returns where nearly everything declined. This was the near perfect opposite of the prior year where nearly every asset class had increased in value. 2) As far as bad years go, this one was pretty ho-hum. Single digit downside in the S&P, worse for international and emerging markets, roughly flat for bonds and gold. As far as bad outcomes go, things could have been much worse.

In stocks we continue to see more value in International and Emerging Market stocks vs. their domestic peers. On average these markets have underperformed the US for many years, a trend that we expect to reverse at some point in the future. For asset allocation oriented portfolios we continue to “overweight” exposure to these investments relative to our normal allocation targets. Likewise, we are slightly underweighting US stocks in asset allocation oriented portfolio strategies.

For Bonds we continue to allocate fairly heavily to unconstrained strategies which we feel offer better return potential in a rising rate environment, vs. traditional fixed income. The flat year for bonds doesn’t really tell the whole story, since as recently as November the aggregate index was down ~ 2% with intra-year returns as low as 3% at one point during 2018. The December market panic in riskier assets sent money flooding in to the perceived safety of high quality government bonds which bailed out their returns for the year. Still, in a year when the aggregate bond index was flat, our unconstrained position was up +.88%. We view these positions as a compliment to traditional fixed income exposure, where they may provide some support in a difficult rate environment.

Finally, diversifying assets like gold and commodities, while putting in weak returns for 2018, remain of interest both because of their diversification benefits, and because they are generally unloved. After peaking in 2008, commodities have been on a fairly steady down trend. Likewise for Gold which peaked in 2011. Gold saw some light at the end of 2018 though, rallying 7.5% in the 4th quarter while most risky assets saw significant declines.

*Individual accounts will vary based on a client’s stated objectives, risk tolerance and time frame. We manage several different portfolio strategies, so not every client has exposure to the securities, asset classes or investment strategies discussed above. In addition to growth and/or income oriented asset allocation strategies, we also manage more concentrated equity portfolios that generally carry a higher degree of risk and volatility. Let us know if you want to discuss your specific portfolio strategy in greater detail.

Should you have any questions regarding your investment account(s) and personal financial plans, or if there have been any recent changes to your investment and/or retirement objectives, please do not hesitate to contact our office to speak with one of us at your convenience. We can also provide you with a current copy of our SEC Form ADV Part 2, at your request.

Finally, we launched an online client portal in 2017 and have received positive feedback from clients who have signed in to the portal. The portal provides a wealth of information about your portfolio strategy, performance and holdings. If you are interested in having access to the portal please contact our office and will activate your account.

As always, we thank you for entrusting AMM to help you achieve your investment and retirement objectives and wish you a very happy, healthy and prosperous new year!

Sincerely,

Your Portfolio Management Team