The first true pharmaceutical biotech company was Genentech.

Launched in 1976 and funded by the now legendary venture capital firm Kleiner Perkins, Genentech would license a new recombinant DNA technology to make insulin safer, faster, and cheaper than the current method of extracting it from live cows and pigs.

Genentech was part of the first wave of biotechnology innovation that transformed pharmaceuticals and agriculture.

Cheap DNA sequencing, increased computing power, powerful new gene editing tools, and AI are setting up the third wave of the biotechnology revolution.

The third wave will still have profound effects on healthcare and agriculture but now a new industry will get caught up in the third wave of biotech innovation, industrial production.

As much as 60 percent of the physical inputs to the global economy could, in principle, be produced biologically—about one-third of these inputs are biological materials (wood or animals bred for food) and the remaining two-thirds are nonbiological (plastics or fuels) but could potentially be produced or substituted using biology.

Mckinsey further states that there are 400 identifiable and scientifically feasible use cases today that would have a direct economic impact of $2-4 trillion over the next 10-20 years.

Like shark-free moisturizer

Squalene is a moisturizer used in skin-care products and it’s traditionally derived from shark liver oil. Now it can be produced more sustainably through the fermentation of genetically engineered yeast.

And cow-free milk.

Milk is simply a mixture of water, sugar, fat, and protein. Why not make it from the molecule up using genetically engineered yeast?

Perfect Day can start making milk from yeast in 72 hours versus waiting 3 years for a dairy cow to mature. Plus, you eliminate animal welfare issues.

And chicken-free egg whites.

Egg whites are a multi-billion dollar market. Egg whites are used in commercial baking, sold in cartons for cholesterol-conscious consumers, and used in protein powders.

But egg whites are 90% water and 10% protein. Instead of putting time and effort into housing and raising chickens until they can start producing eggs, why not modify yeast to produce the proteins, add water, and develop a process to recreate the consistency of egg whites from an egg?

And biodegradable plastics made from yeast and plant oils.

The disruption of industrial production is the next biotech gold rush and who makes the most money during a gold rush? It’s the merchants like Sam Brannan that sold the picks and shovels.

Thermo Fisher sells the biotech equivalents of picks and shovels, and they are in a prime position to benefit from the next wave in biotech innovation.

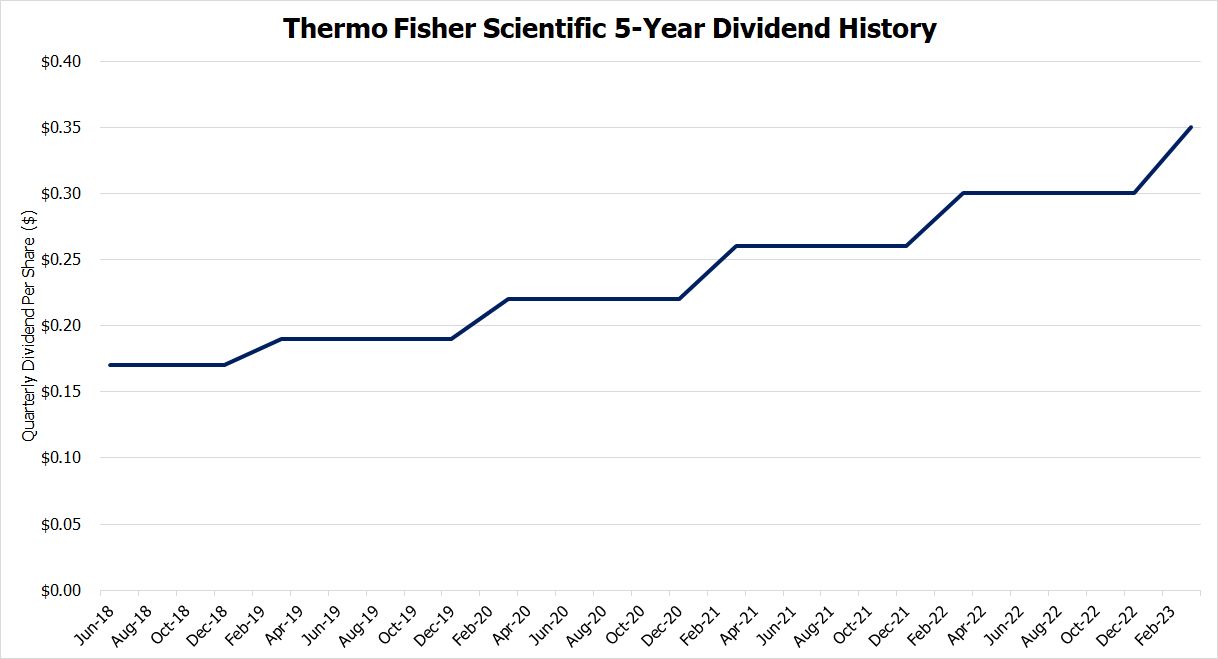

Dividend History

Thermo Fisher has paid a dividend for over 10 years. But from 2013 to 2017 their quarterly dividend never grew. It remained at $0.15 per share.

Then in 2018, Thermo Fisher started growing their dividend in earnest. Over the last 5-years, they’ve grown their quarterly dividend at a compound annual growth rate of 15.54%.

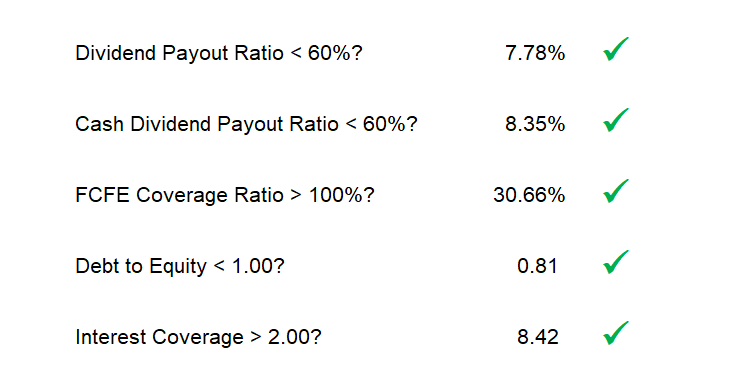

Dividend Safety

Overlooked Growth Metric

Revenue growth and EPS growth are the two most common metrics “growth investors” look at. Given the secular growth trend in biotechnology, We’re not too concerned with Thermo Fisher’s revenue and earnings growth.

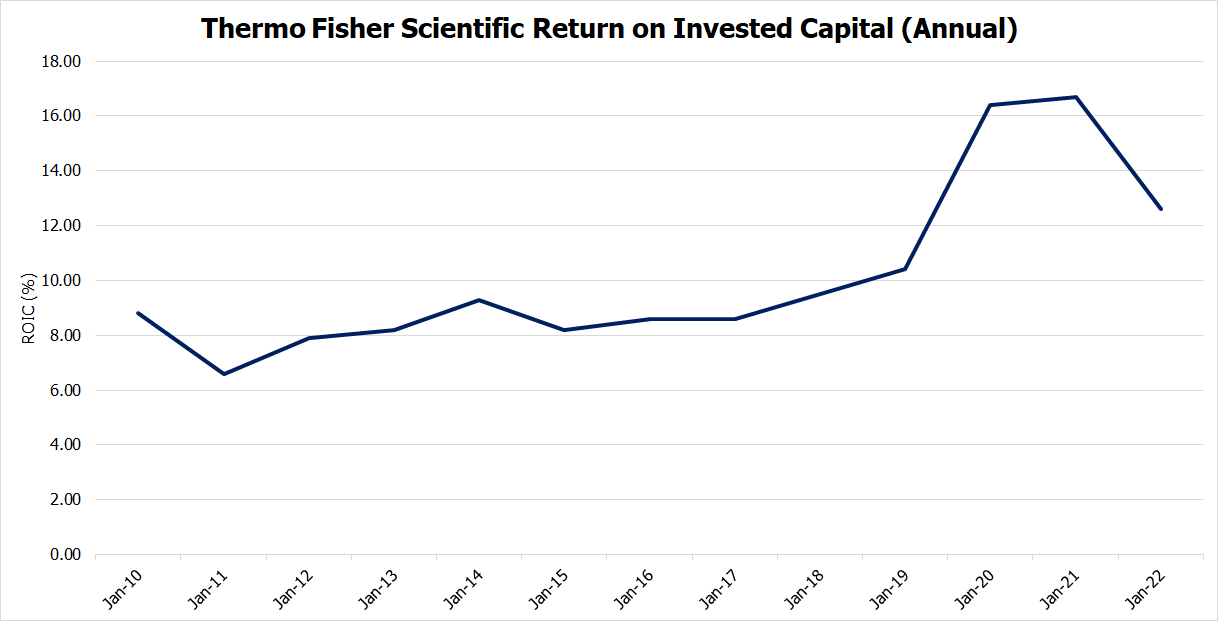

We’re more concerned with the quality of its growth which is captured in its Return on Invested Capital (ROIC) metric. ROIC is an important growth metric that can be overlooked by investors.

If a company’s ROIC is higher than its cost of capital, then growth creates shareholder value. If a company’s ROIC is less than its cost of capital, it will need to continually raise outside capital eroding shareholder value.

For the last 10 years, Thermo Fisher’s ROIC hovered in the mid-single digits and looked like it was barely covering its cost of capital, if at all.

During this time Thermo Fisher was on an acquisition spree. They were filling in the gaps in its product offering. The shopping spree culminated with the acquisition of PPD, a contract research organization (CRO).

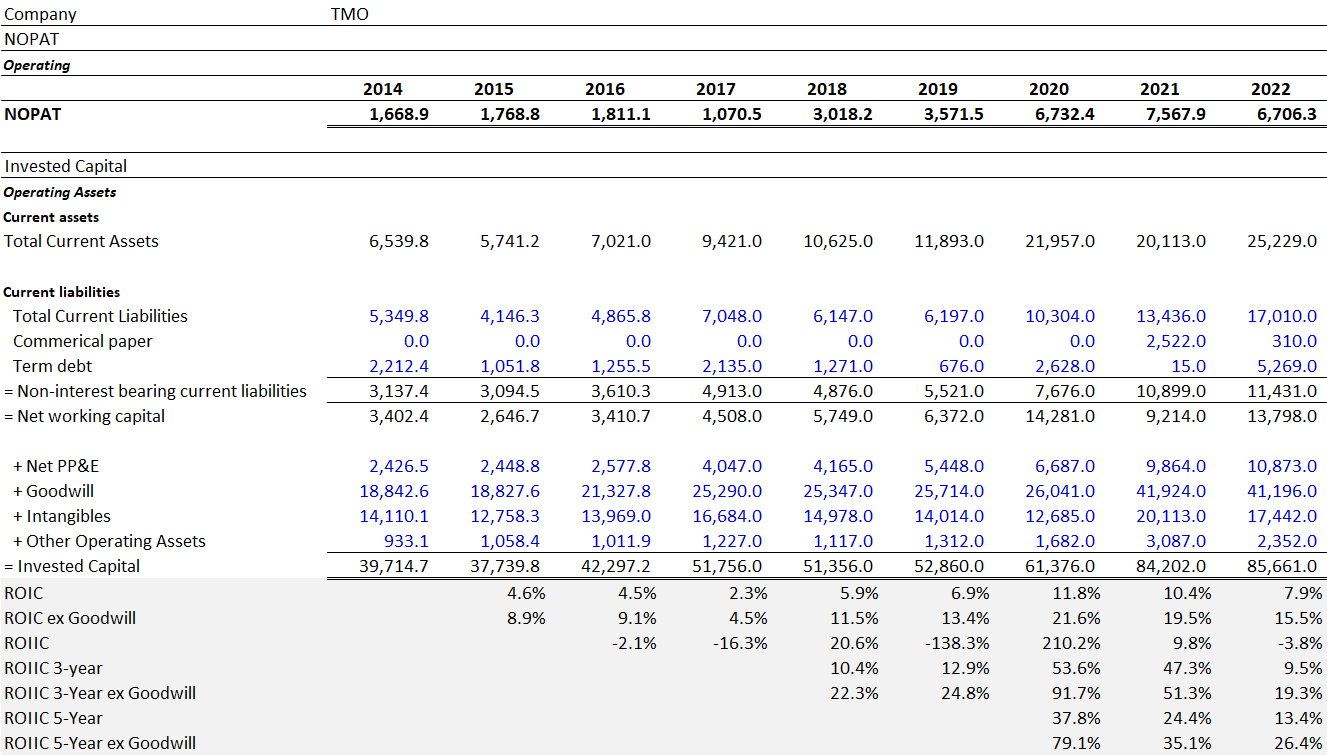

Even though Net Operating Profit After Taxes (NOPAT) grew during this period, the large capital investments needed to complete its acquisitions depressed its ROIC. If we look at Thermo Fisher’s Returns on Tangible Capital, ROIC less Goodwill, these numbers improve. (see table below)

Thermo Fisher will continue to buy companies that complement its product portfolio, but Thermo Fisher is so large now that these acquisitions will have less of an effect on its total capital invested. NOPAT should continue to grow and Thermo Fisher’s returns on invested capital should grow too.

We’re seeing that growth now.

Returns on Incremental Invested Capital (ROIIC)

Return on invested capital is heavily influenced by past investment decisions. What we want to know is, does Thermo Fisher still have new high-returning reinvestment opportunities? We can look at the Return on Incremental Invested Capital (ROIIC) to help us answer this question.

In the table above, we calculated 1-year ROIIC, 3-year ROIIC, and 5-Year ROIIC based on operating assets. 1-year ROIIC tends to be volatile whereas 3-year and 5-Year ROIIC tends to be a better gauge of a company’s reinvestment opportunity.

Based on Thermo Fisher’s 3-year & 5-year ROIIC, the company still has high reinvestment opportunities to grow its competitive advantage and increase shareholder value.

2020 and 2021’s ROIC and ROIIC were positively skewed by the Covid pandemic. ROIIC is coming back down as profits and NOPAT normalize but they still remain high and on-trend with Thermo Fisher’s pre-Covid years.

Quality Factors

Thermo Fisher’s business model is protected by two intangible qualitative factors that will keep its incremental returns on capital high, Switching Costs and Search Cost Reductions.

Switching Costs

The simple definition of biotechnology is:

technology that utilizes biological systems, living organisms or parts of this to develop or create different products.

The process is the product.

A prime example is biologics, large molecule therapeutics, like AbbVie’s Humira.

Small molecule drugs are made through a chemical process. The process can be tweaked to reduce costs and increase production efficiency if the result is the exact same chemical compound as before.

Biologics are based on human proteins but modified and optimized to provide therapeutic effects. Biologics are manufactured using microorganisms. The entire process to create, produce, isolate, and purify the biologic is the drug. A change in any step can create a different product.

The production process needs to remain uniform. This creates large switching costs for the tools and systems used in the process.

Reducing Search Costs

Outside of Biopharma, the switching costs aren’t as high. So, Thermo Fisher relies on search cost reductions to lock in customers from the rest of the biotech industry.

Search costs are usually associated with consumer goods. You buy Tide laundry detergent because it’s a trusted brand that will get the job done. Time is money and you don’t need to waste your time comparing different laundry detergents.

The distributor business model reduces search costs too.

If a distributor like Thermo Fisher has everything you need then you don’t need to waste your time shopping with multiple vendors. You also have the peace of mind that what you’re ordering is effective and of high quality. Plus, you’ll receive better pricing the more products you order through Thermo Fisher.

Risks

Some risks outside of the normal business and valuation risks.

Higher Interest Rates

Yes, higher interest rates will increase the cost of capital for Thermo Fisher and increase the costs for any future acquisitions.

But the real issue is the delay of the third wave of biotechnology disruption. The companies that will usher in the era of shark-free lotions and chicken-free egg white are not profitable. Many of them haven’t even been formed yet. They will burn through a lot of capital to get where they need to go. They need regular access to the capital markets.

The higher the interest rates, the less access these young companies will have to the capital markets to fund their growth. Delaying the gold rush and lowering the present value of Thermo Fisher.

Introducing Cyclicality

The industrial sector is cyclical. As the industrial biotech revolution ramps up, it will add more cyclicality to Thermo Fisher’s business model.

For biotech companies, Thermo Fisher is an operating expense, not a capital expenditure. Companies will have to buy Thermo Fisher’s products to run their business. But operating expenses will decline during an industrial slowdown. A cyclical business can’t command the 34x P/E that Thermo Fisher has right now.

Valuation

A growing ROIC combined with revenue and earnings growth should generate significant shareholder value in the coming years.

But we’re not price agnostic.

Based on a discounted cash flow model we’re willing to buy Thermo Fisher Scientific (TMO) below $618 per share.