The ideal company to own would possess the following 3 attributes.

- Operates in an industry with minimal competition and with high barriers to entry for new competitors allowing the company to generate high Returns on Invested Capital (ROIC).

- Requires minimal capital reinvestment to maintain and grow its business.

- Is riding a long secular growth trend that allows the company to reinvest retained capital at high returns.

S&P Global (SPGI) checks-off on all three attributes.

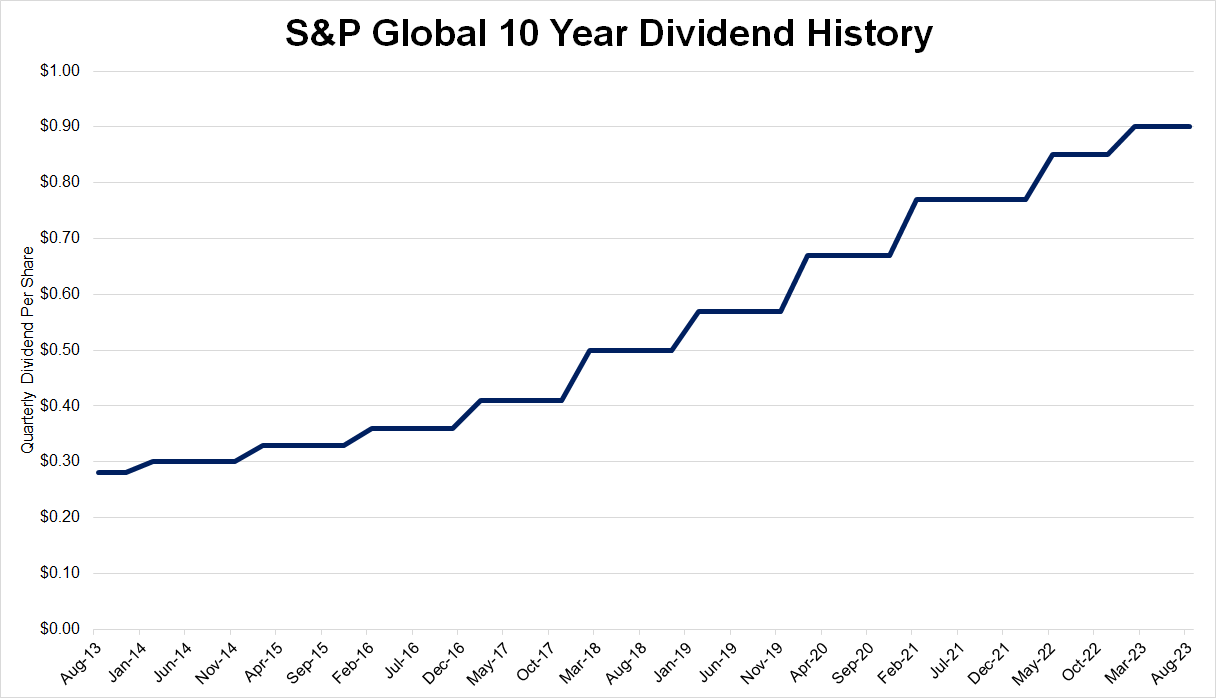

Dividend History

Over the last 10 years, S&P Global has grown its quarterly dividend at a compound annual growth rate of 12.38%, and for the last 5 years, S&P Global grew its dividend at a 12.47% compound annual growth rate.

Over the last 10 years, S&P Global has grown its quarterly dividend at a compound annual growth rate of 12.38%, and for the last 5 years, S&P Global grew its dividend at a 12.47% compound annual growth rate.

Dividend Safety

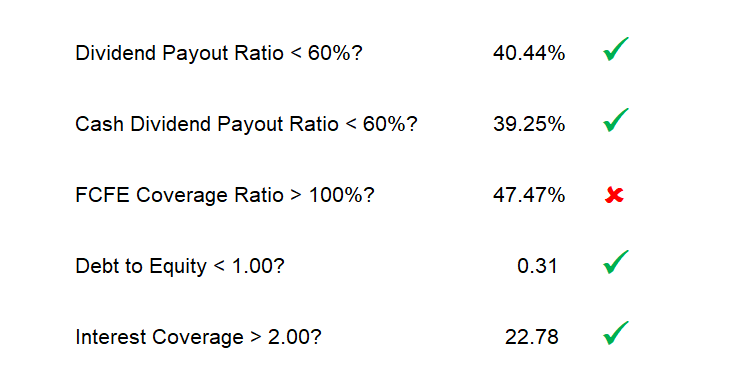

The Free Cash Flow to Equity (FCFE) coverage ratio is FCFE divided by Total dividends paid plus share repurchases. S&P Global misses this checkmark because, over the last twelve months, they bought back over $5.5 billion in stock. This increases the denominator by a significant factor reducing the FCFE coverage ratio.

The Free Cash Flow to Equity (FCFE) coverage ratio is FCFE divided by Total dividends paid plus share repurchases. S&P Global misses this checkmark because, over the last twelve months, they bought back over $5.5 billion in stock. This increases the denominator by a significant factor reducing the FCFE coverage ratio.

The large share repurchase is a one-time discretionary choice made by management. When we back out the large share repurchases, S&P Global passes all our safety checklist items.

S&P Global's dividend is not at risk of being cut and management should be able to raise its dividend safely.

Quality Factors

High Barriers to Entry

S&P Global is a Nationally Recognized Statistical Rating Organization (NRSRO). This is a title and privilege given by the U.S. Securities and Exchange Commission (SEC) and only 10 companies qualify

- A.M. Best Rating Services, Inc.

- DBRS, Inc.

- Demotech, Inc.

- Egan-Jones Ratings Co.

- Fitch Ratings, Inc.

- HR Ratings de México, S.A. de C.V.

- Japan Credit Rating Agency, Ltd.

- Kroll Bond Rating Agency, Inc.

- Moody's Investors Service, Inc.

- S&P Global

The biggest are S&P Global, Moody’s, and Fitch and they act as an Oligopoly within the U.S.

Switching Costs

A debt issuer could use another lesser-known rating company to rate its debt or issue its debt unrated. However, market participants will demand a higher yield on the issued debt to compensate them for the increased risk.

For example, the upfront rating cost for S&P Global on a basic 5-year $500 million corporate bond is about 7bps or around $350,000.

A rating from S&P Global can lower the initial interest rate on the bond by 30-50 bps.

If an unrated bond has an interest rate of 6% then a S&P Global rated bond may pay a rate of 5.5%.

Each year the unrated bond will pay $2.5 million more in interest than the rated bond.

If the bond has a maturity of 5 years, then the unrated debt will pay $12.5 million more in interest over the life of the bond versus a bond rated by S&P Global. The amount of interest expense saved over the life of the bond far exceeds the higher upfront costs S&P Global charges.

Would you pay $350,000 upfront to save $12.5 million over the next 5 years?

Of course, this ensures that debt issuers keep coming back to S&P Global versus using smaller less trusted ratings firms or issuing unrated debt.

Network Effects

Because an S&P Global rating can save a bond issuer millions of dollars a year, it attracts more issuers. Because it has more bond issuers, more regulators and investors rely on S&P Global’s measurement of risks and creditworthiness. S&P Global’s rating service becomes more valuable for each side as more of them use S&P Global’s service. This is a network effect.

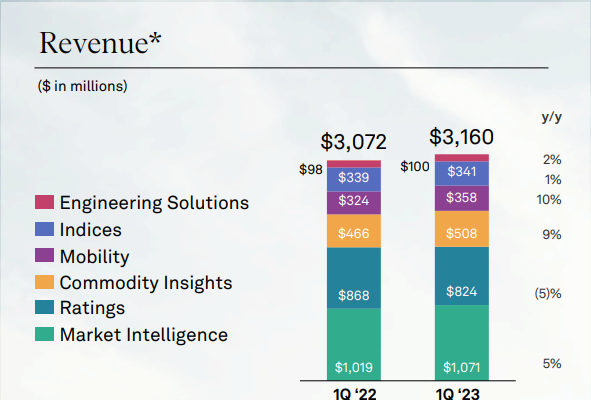

The same effect happens with its data and analytics business. The more data S&P Global collects the more valuable its database becomes to customers. The more customers S&P Global has the more S&P Global can invest in the collection and creation of diverse data sources. This makes it even more valuable to its customers. This too is a self-reinforcing network effect.

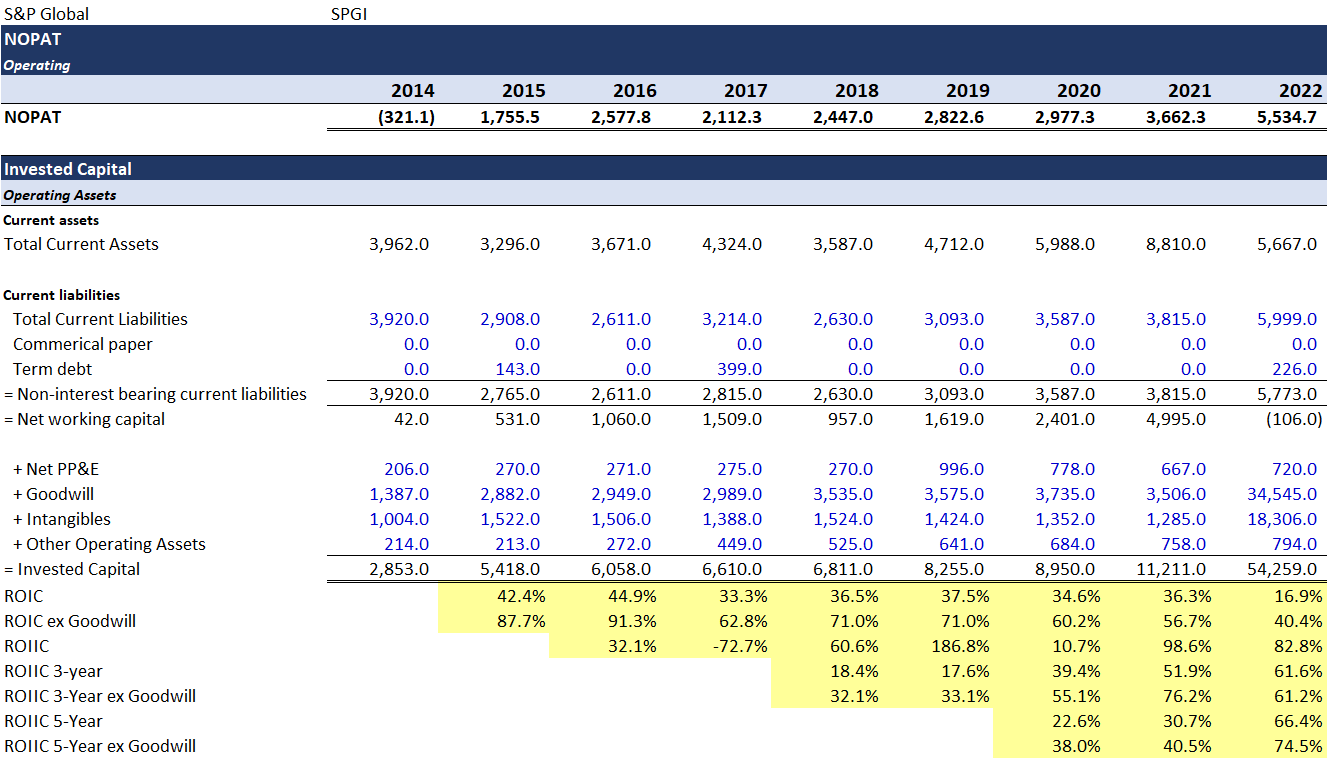

ROIC & ROIIC

High barriers to entry, high switching costs, and network effects create durable competitive advantages for S&P Global and it allows them to generate high returns on invested capital.

S&P Global also has high returns on incremental invested capital (ROIIC). This indicates that S&P Global's new projects are generating returns over the cost of capital, increasing its competitive advantage, and strengthening its future competitive position.

Part of the reason S&P Global has such high returns on incremental invested capital is that it runs an asset-light business and is reinvesting capital into several secular growth trends.

Part of the reason S&P Global has such high returns on incremental invested capital is that it runs an asset-light business and is reinvesting capital into several secular growth trends.

Growth

ETFs & Index Investing

One of the biggest secular growth trends in financial markets is the transition from mutual funds to ETFs which is driven by the rise in index investing.

U.S mutual funds have over $18 trillion in assets.

Equity-focused ETFs have over $5.6 trillion in assets and bond ETFs have over $1.3 trillion in assets.

The ETF market should continue to grow from overall economic/market growth but we expect it will grow faster than the general market as it takes market share from mutual funds.

S&P Global benefits from the growth of ETFs and indexing in the following ways.

Index Licensing

S&P Global creates and maintains a wide range of stock market indices, including the S&P 500, S&P 1000, and various sector-specific indices. These indices serve as benchmarks for many ETFs and S&P Global generates revenue by licensing the use of its indices to ETF providers.

Custom Indices

S&P Global also offers custom index services, where it collaborates with financial institutions and asset managers to create tailor-made indices based on specific criteria or investment strategies. These custom indices can be used by ETF providers to launch specialized ETFs. S&P Global earns fees for designing and maintaining these custom indices.

Data & Analytics

ETF providers may also subscribe to S&P Global’s financial data, analytics, and research services for historical and real-time data on market indices, individual stocks, and other financial instruments.

Data & Analytics

The best product is one that you make once and then can sell over and over again for minimal to no cost.

That’s data.

The cost to create it or collect it is minimal and then you can sell it in many different ways to many different customers. S&P Global sells and repackages its data in the following ways.

Subscription Services

S&P Global provides a wide range of subscription-based data and analytics services to financial institutions, corporations, and other market participants. These services include access to market data, financial research, credit ratings, risk assessments, industry reports, and other proprietary insights. Subscribers pay fees based on the level of access, the scope of the data they want to access, and the specific services they require.

Data Feeds and APIs

S&P Global offers data feeds and application programming interfaces (APIs) that enable clients to integrate S&P Global's data directly into their systems, applications, and platforms. S&P Global charges licensing fees based on factors such as the volume of data consumed, the number of users, and the specific use case.

Research Reports and Publications

S&P Global produces in-depth research reports, market analyses, and industry publications across various sectors and asset classes. S&P Global monetizes these publications by selling individual reports, offering subscriptions to specific research products, or bundling them with other services.

Custom Solutions and Consulting

S&P Global provides customized data and analytics solutions to meet the specific needs of individual clients. This may involve creating tailored datasets, building analytical models, or delivering specialized consulting services. The pricing for these custom solutions is typically negotiated on a case-by-case basis, accounting factors such as the complexity of the project, the level of expertise required, and the value provided to the client.

ESG

ESG investing is becoming a bigger interest to investors and ETF providers. The two largest ESG data providers are S&P Global and MSCI.

The data and methodologies that generate an ESG score are opaque. The EU has proposed regulations to make the process more transparent and uniform. Regulations tend to favor the incumbents who have the money to invest in compliance, the staff to build out the compliance structure, and the ability to acquire and invest in smaller ESG data providers.

A.I.

The large Language Models (LLM) that are A.I. today have a voracious appetite for data and S&P Global owns much of the financial data LLMs want.

“While the core of its business is steeped in Wall Street, S&P's end markets are a cross-section of corporate America... governments... municipalities... and even farming, mining, metals, banks, insurance, chemicals, biofuels, oil, and mining companies. The list goes on.

Need data on energy carbon capture units? S&P has it.

Battery cell data for electric vehicles? It has that, too.

The history of millions of used cars sold in America? Sure, that's because S&P owns Carfax, which collects the mechanical history on used cars. But S&P also has auto supply chain and marketing data. No wonder it counts 45,000 auto dealers and all major auto makers among its customers.”

S&P Global could license its data to the LLMs but the more lucrative play would be to bundle an A.I. service with its data feed at a premium price. This is probably why they bought Kensho in 2018.

“S&P Global (NYSE: SPGI) announced today that it has signed an agreement to acquire Kensho Technologies Inc. ("Kensho"), a leading-edge provider of next-generation analytics, artificial intelligence, machine learning, and data visualization systems to Wall Street's premier global banks and investment institutions, as well as the National Security community.” [emphasis added]

We’re in the very early stages of A.I. but its growth should be another way for S&P Global to repackage and sell its data at a premium and strengthen its market position.

Risks

Outside of normal business risks, we highlight below some key risks that could negatively affect S&P Global.

Rising Rates

Bond ratings are S&P Global’s second-largest revenue source.

Higher interest rates should slow the pace of corporate bond issuance. Companies that issued debt during the period of ultra-low rates to buy back shares might prioritize deleveraging and paying off their debts instead of refinancing them. Mortgage originations will slow which reduces the issuance of mortgage-backed bonds. The same with commercial real estate and commercial mortgage-backed bonds.

In the short term, S&P Global’s debt rating business is under pressure but even more so if rates continue to rise.

ESG

ESG is a valuable high-growth data niche for S&P Global but they may have to divest of the business or restructure the ownership to reduce “conflicts of interest”. Regulations proposed by the EU would prohibit ESG data providers from providing consulting services, credit ratings, benchmarks, investment activities, audit, banking, insurance, or reinsurance services. All services currently provided by S&P Global.

A divestiture of its ESG business will deprive S&P Global of a growth engine.

A.I.

This is more of an unknown risk.

A.I. could be very beneficial for S&P Global but could it be a major business risk later on. Could an LLM be a better analyst of credit risk? Could a new A.I. rating agency get an NRSRO rating from the SEC and take market share away from S&P Global or disrupt them completely?

Valuation

"When looking for quality companies, the desired outcome is always clear: strong, predictable cash generation; sustainably high returns on capital; and attractive growth opportunities."

- From Quality Investing

The problem for investors is high-quality companies with strong predictable cash flows, sustainable returns on capital, and attractive growth opportunities usually trade at a premium to the market. This makes it hard to initially invest in them because they appear overvalued.

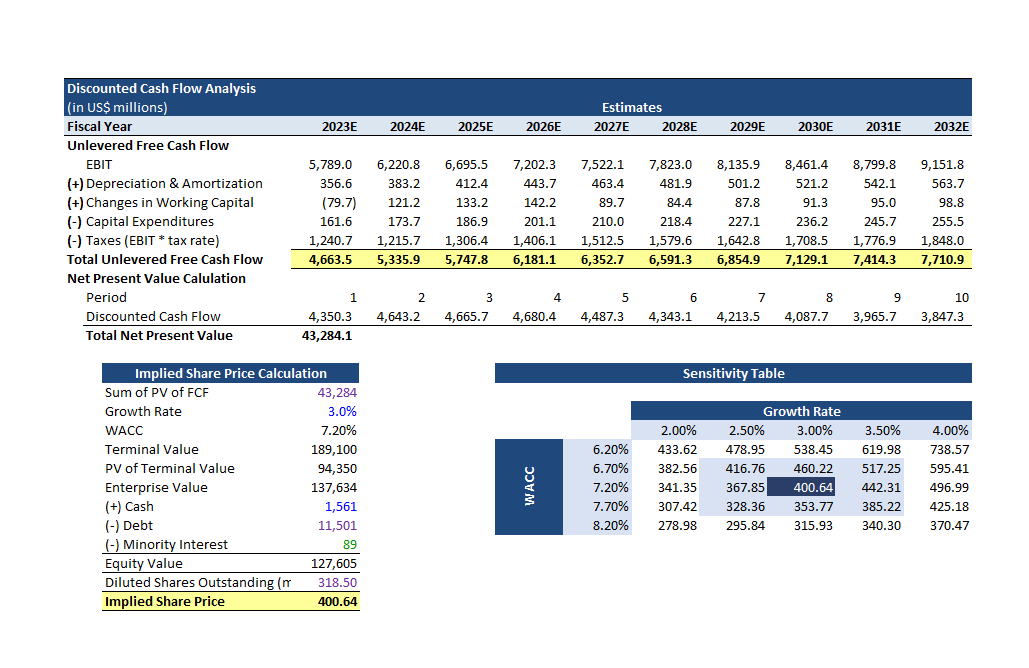

S&P Global is no exception. It currently trades at a premium to our estimate of fair value based on a discounted cash flow model.

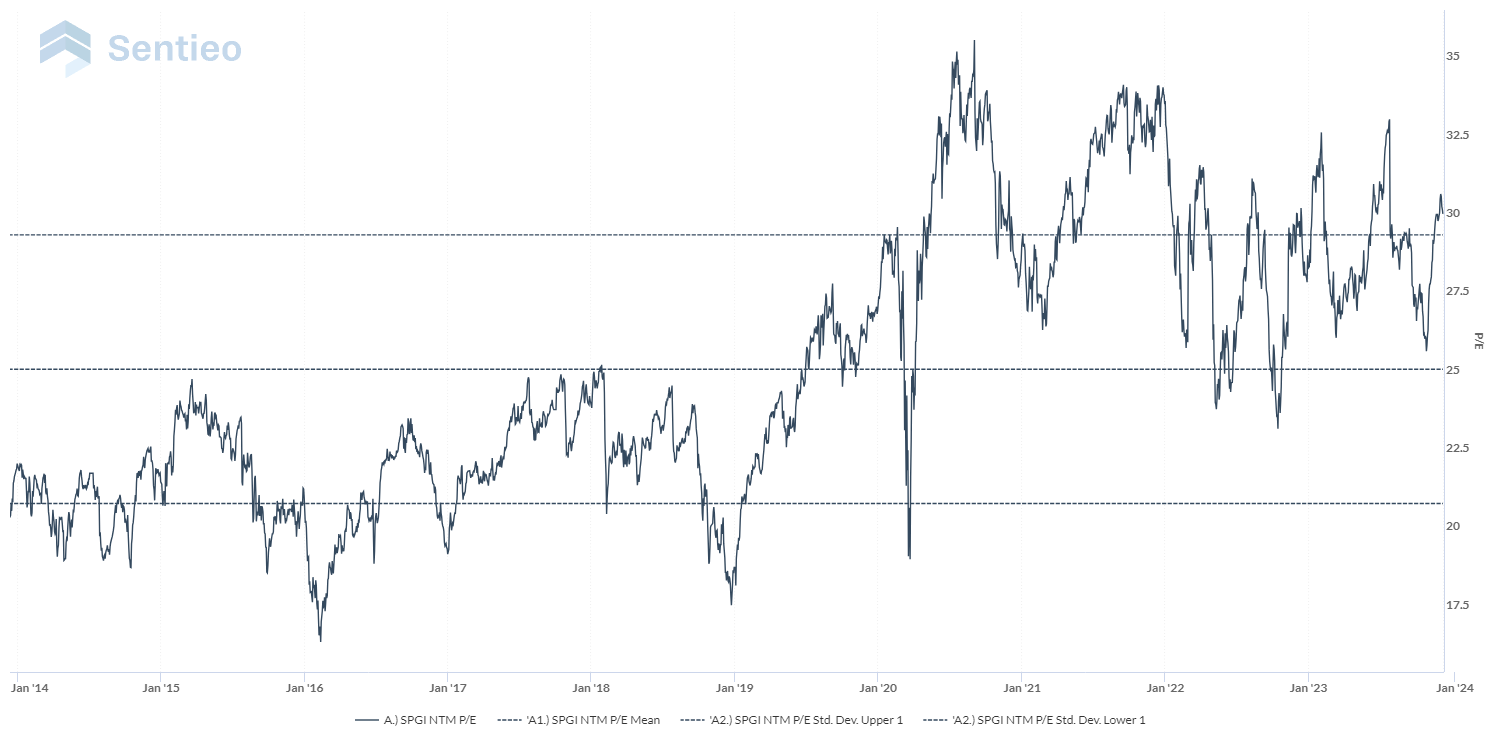

And its P/E ratio is currently near the high side of its 10-year range.

However, according to What Valuations Tell Us (and don’t tell us) About Future Factor Returns, the starting valuation for quality companies has a weak relationship with their future returns.

In contrast, valuations for the minimum volatility, momentum and quality factors have shown a weak relationship with subsequent performance. In general, investors have pursued strategies based on these factors because of inefficiencies resulting from behavioral biases than from relative valuation.

Durable competitive advantages give quality companies like S&P Global a longer period to reinvest retained capital. If over this period a company can reinvest its retained capital at a high rate of return then its long-term earnings growth will exceed current expectations and today’s high valuation will look cheap in the next 5-10 years.