Download AMM’s Q2 2018 Client Letter

Life’s but a walking shadow, a poor player that struts and frets his hour upon the stage and is heard no more.

It is a tale told by an idiot, full of sound and fury, signifying nothing – William Shakespeare, Macbeth

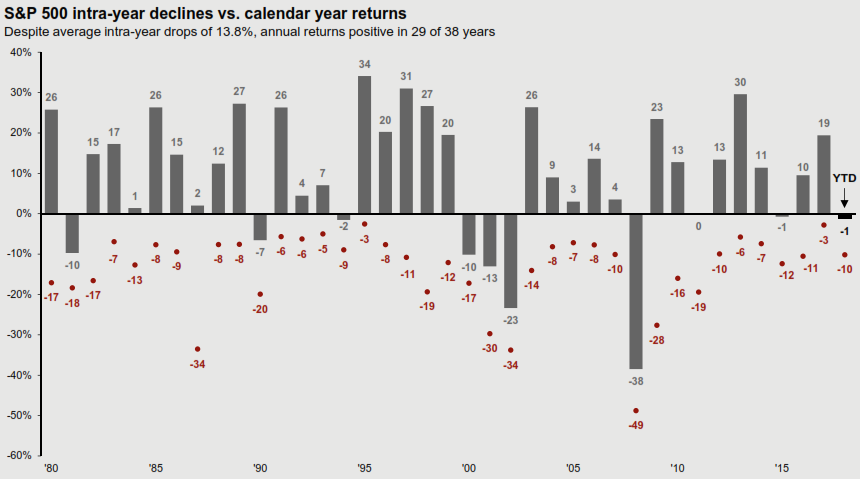

It is not often that we find ourselves quoting Shakespeare in our quarterly missives, but the recent resurgence of “market volatility” reminds us that market fluctuations are not unlike the “story told by an idiot, full of sound and fury, signifying nothing”. In short, day to day gyrations do not mean much to the long-term investor. Exhibit A is our case in point. Despite average Intra year drops of more than 13% since 1980 (red dots), the US stock market (S&P 500) has generated an average annual return of 8.8% over this time frame (grey bars). A $10,000 investment in 1980 would have turned in to more than $226,000 by the end of 2017.

Exhibit A

Source: FactSet, Standard & Poor’s, J.P. Morgan Asset Management. Returns based on price index only and do not include dividends.

This stresses a key point about market timing: An investor’s success comes not from timing the market but from time in the market. Of course, time in the market means exposing your portfolio to market declines and unrealized losses. We are not suggesting that you should ignore “market risk”, but rather that traditional market timing (i.e. reading tea leaves to determine market direction and then deftly trading in and out) is a fool’s errand. The problem with this kind of timing is that it is riddled with false positives. In any given year, there are countless triggers that could lead a seemingly “rational” investor to sell or de-risk. The night of the 2016 presidential election saw the Dow Futures markets drop nearly 1,000 points as it became clear that Donald J. Trump would become president, causing “great policy uncertainty”. The next day, markets rallied because we now had a “business friendly, tax cutting” president in office. In less than 24 hours, the “market” had completely changed its mind about the election.

At their core asset markets, including those for stocks, bonds and real estate, are price discovery machines matching buyers and sellers who possess imperfect information about the present and the future. Determining the appropriate price of stocks at any point in time is, therefore, a messy and imperfect process that invariably generates a lot of noise – signifying nothing. It is not an overstatement to say that not a week goes by without some piece of seemingly important data that “moves markets”. Investors should mostly ignore this noise.

Stocks go from hand A to hand B, from buyer to seller or seller to buyer, and I think it sometimes concerns the true long-term investors. It disturbs the investors because they see this and they think it’s significant. If it’s significant to them, and they panic in a big market decline and get out, they’re the losers. -Jack Bogle, Founder and Former CEO of Vanguard

Furthermore, the math of market timing does not play to the investor’s favor. To correctly market time, you need to get two decisions right: 1) when to sell so as to avoid further declines and 2) when to buy back in. If the odds of correctly timing each decision are equivalent to a coin toss (i.e. 50%) as we contend, then doing both correctly gives you a 25% chance of success. Let us assume, however, that you are deeply skilled and attuned to the markets and that your odds of correctly timing each decision are 70%. In this case, your odds of doing both correctly are 49%, still worse than a coin toss. The odds of achieving a positive return in any calendar year by just staying invested: 76%*.

Unfortunately, this information is often disregarded when a real market storm hits. Investors, chastened by portfolio declines, seek the safety of cash and sell to “stop the bleeding” until markets “calm down”. Calm markets are usually parlance for higher prices, which means that investors find themselves engaging in the wealth destructive behavior of selling low and buying high. One of our firm’s core investment principals is “volatility is not risk.” We believe real risk is more accurately defined as the “likelihood of permanent capital loss”. In the case of market declines, it is not volatility itself that increases risk, but rather the investor’s reaction to this volatility (i.e. selling in to a decline) that increases risk which may lead to a greater likelihood of permanent capital impairment.

Preparing for the Big One

Much like the earthquakes we are occasionally subjected to here in California, periodic market storms are a fact of investing life. Most of the time, these storms are mere tremors, corrections of 10-20% that cause no lasting harm. Once in a while, the Big One hits, and a lengthy and deep market decline ensues. This occurred most recently when the market peaked in October of 2007 and bottomed in March of 2009, an affair that lasted 16 months and included a peak to trough decline of well over 50%. If we invest as if each tremor is the start of the Big One, then your long-term returns will suffer, as we will be whipsawed by all of the market noise. Instead, we take a disciplined approach to risk management that includes the following steps:

- Asset Allocation: Develop an appropriate asset allocation strategy for your specific risk tolerance, life stage and investment objectives. If you are in your 30s or 40s and have a 20 year+ time horizon, than a fully invested stock portfolio will likely give you the best odds of maximizing returns over time. If you are nearing retirement and plan to begin drawing down assets soon, than a more balanced approach that incorporates conservative fixed income would likely be more appropriate. Every situation is unique, but this decision is crucial to appropriate risk management.

- Asset Segregation: Consider segregating assets by time horizon. Maintain a 1 year fund of readily available cash, CDs or money market funds for any near term needs. A second balanced investment account may be viewed as appropriate for intermediate term needs (1-10 years). Finally, consider a more aggressive account for time horizons longer than 10 years. This way, when the inevitable market storm hits, you can feel confident that your shorter term cash needs will not be impaired, making it psychologically easier to ride out the storm with your longer term money.

- Invest Throughout the Market Cycle: If you are regularly investing money, you may be tempted to stop when markets decline. Shoring up reserves and simply having money that is not “at risk” can be comforting during these periods. However, market declines can provide the best time to invest since you are able to invest at lower prices. The lower the price paid, the higher your return all else being equal. From a total portfolio perspective, these additional investments during market declines will lower your cost basis and shorten the time it takes to get the portfolio back to its prior highs.

- Rebalance: AMM periodically rebalances client portfolios back to their pre-determined asset allocation levels. This means that if markets have gone up for an extended period, a portfolio rebalance would likely result in selling stocks or taking profits. Alternatively, an extended period of declines would result in buying stocks. Rebalancing is a mechanical way to buy low and sell high.

- Invest in Businesses not stocks and bonds: This is a key behavioral point. Understanding that your investment is in a business rather than a piece of paper that can easily be traded for something else is helpful in keeping a steady hand during market storms. Discussing the proper mindset to avoid overreacting to news events, Warren Buffet famously said, “If you are not willing to own a stock for 10 years, do not even think about owning it for 10 minutes.”

- Focus on Valuation: The higher the price paid for an investment, the lower your expected return and vice versa. When investing in any asset, we pay attention to price and ask whether it makes economic sense at prevailing prices. Investments that we believe are significantly overvalued will be trimmed. Similar to the rebalancing process, this allows us to reduce portfolio risk systematically rather than on “market noise”. A focus on valuation also allows for a more opportunistic mindset during market downturns.

- Focus on Dividends: Stocks generate return via price appreciation and dividends. A focus on businesses that pay and, ideally, increase their dividend distributions to shareholders can help to alleviate the concerns that accompany severe market corrections. More importantly, companies that annually grow their dividends are essentially providing a “pay raise” to their shareholders every year. This is an excellent way to hedge against inflation and build a future retirement income stream.

First Quarter Review

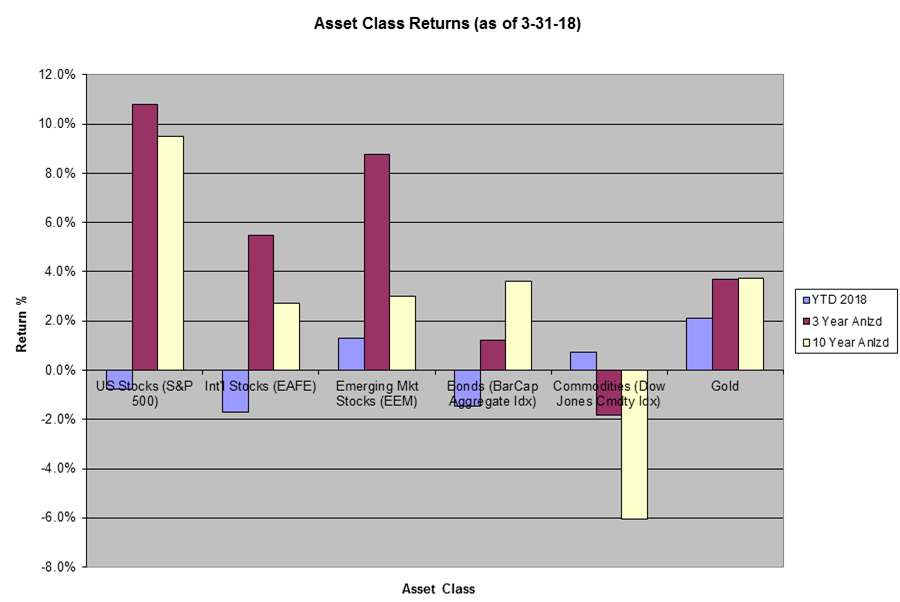

Through 3/31/18, domestic stocks (S&P 500) declined -.76%, developed international stocks (EAFE) declined -1.7%, and emerging market stocks (EM) increased 1.3%. Bonds (Bar Cap Agg Idx) declined -1.5%, commodities were up .7%, and gold gained 2.1%. We have updated our asset class return chart (Exhibit B) to reflect YTD 2018 along with three and ten year annualized returns for the aforementioned asset classes.

ExhibitB

The first quarter saw the first correction (a decline of more than 10%) in three years, which dragged returns down from a roaring start to the year. Industry pundits have many triggering effects to point to, from chaos in the White House to the possibility of a global trade war, to fears of inflation or higher interest rates, to the simple fact that US stocks have been priced much higher than their historical averages. They are not getting much explanatory data from the economic statistics as the unemployment rate is testing record lows and new jobs are being created at record levels. More importantly, annual earnings estimates for S&P 500 companies rose 7.1% during the first three months of the year, the fastest rise since FactSet began keeping track in 1996.

Ironically, the small first quarter downturn plus the jump in earnings may have forestalled a bigger corrective bear market later. The S&P 500, by some measures, is now trading at 16.1 times projected earnings for the next year, compared with 18.6 in late January when the markets were extraordinarily bullish. At current levels, US stock valuations are roughly in line with their 25 year average. The corporate tax cut could lead to higher reported earnings throughout the year, which would provide further valuation support. While not a screaming bargain, we do not see the kind of over-pricing that would suggest an extreme underweight position in domestic stocks.

International and Emerging Market stocks remain relatively more attractive than US stocks from a valuation perspective. For asset allocation oriented portfolios, we continue to overweight these holdings relative to our long-term strategy targets. There are clear risks to both domestic and global stocks posed by the possibility of a trade war; but, at this juncture, such an outcome remains possible but not necessarily probable.

Finally, the market continues to digest the risks posed by rising interest rates. While rising rates are generally bad for bonds, we think that a normalizing of the interest rate environment (i.e. higher rates) will be better for long term savers down the road. Short-term declines and volatility in the bond market are to be expected and should not be cause to abandon bonds. Bonds remain an important component in conservative and balanced client portfolios (i.e. they exhibit much less volatility than stocks); and, ultimately, bonds that mature in a rising rate environment may be reinvested in higher yielding bonds.

In March, we filed the annual amendment of our firm’s ADV brochure dated March 22, 2018 with the Securities and Exchange Commission. Pursuant to regulatory requirements, we have included a document that itemizes the material changes to the last amended brochure. We can provide you with a full copy of the ADV filing at your request.

Should you have any questions regarding your investment account(s) and personal financial plans, or if there have been any recent changes to your investment and/or retirement objectives, please do not hesitate to contact our office to speak with one of us at your convenience.

As always, we thank you for entrusting AMM to help you achieve your investment and retirement objectives.