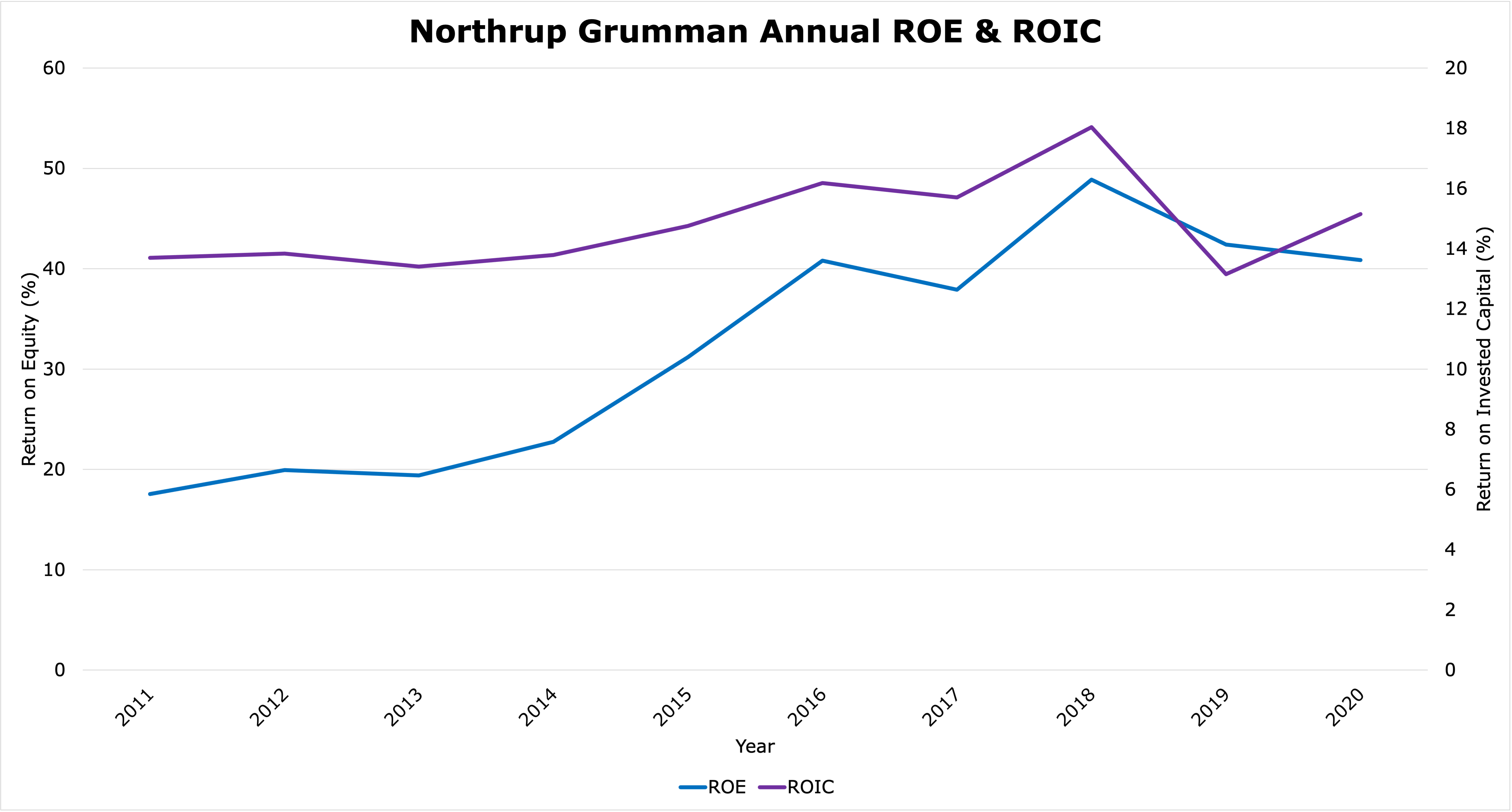

The defense sector consistently generates high returns on equity and invested capital and Northrop Grumman is no exception.

Data from Sentieo

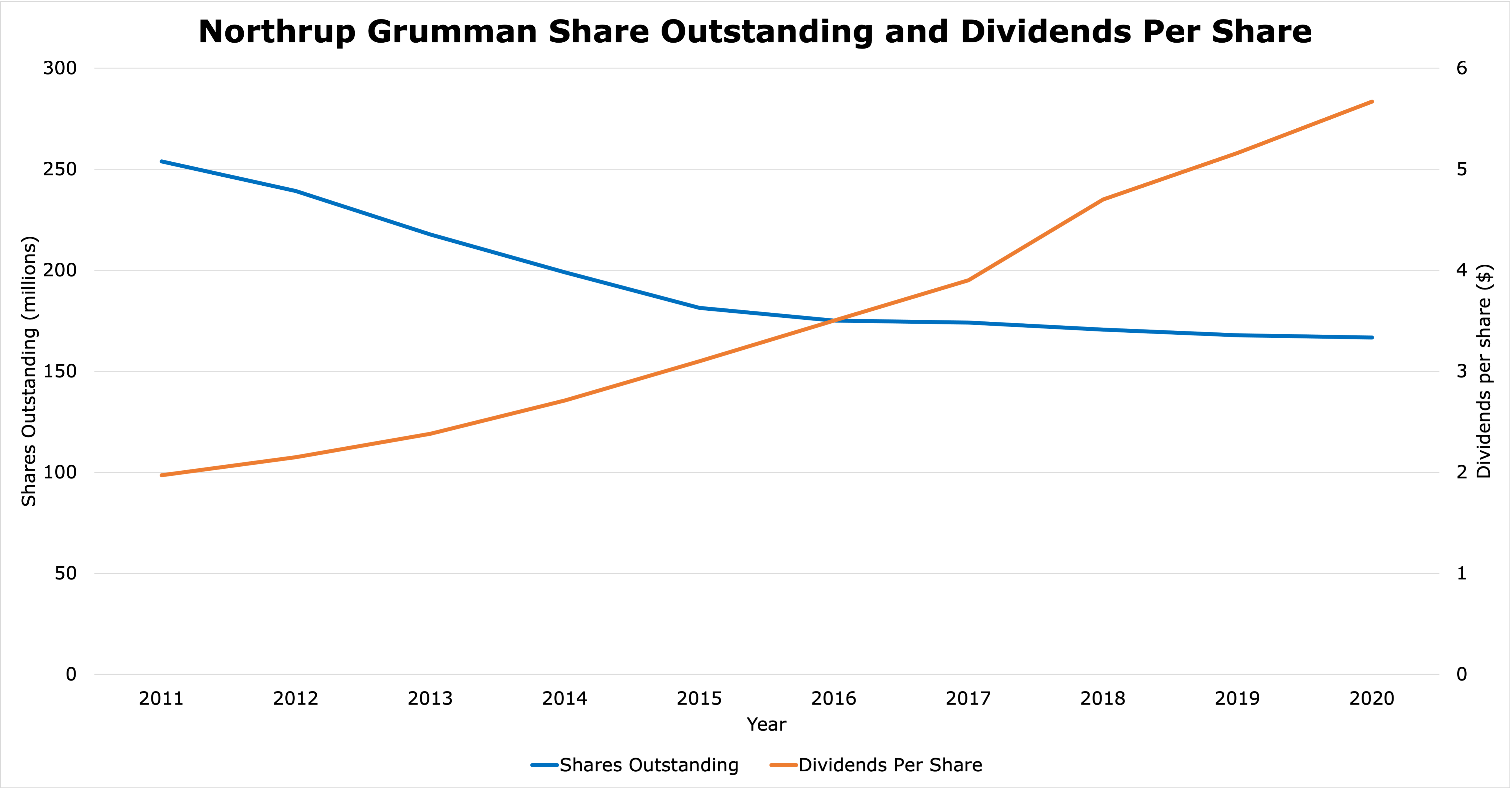

And the defense sector has a history of consistently returning large amounts of capital back to its shareholders. Over the last 10 years Northrop Grumman reduced its share count by 34% and increased its annual dividend per share by 188%.

Data from Sentieo

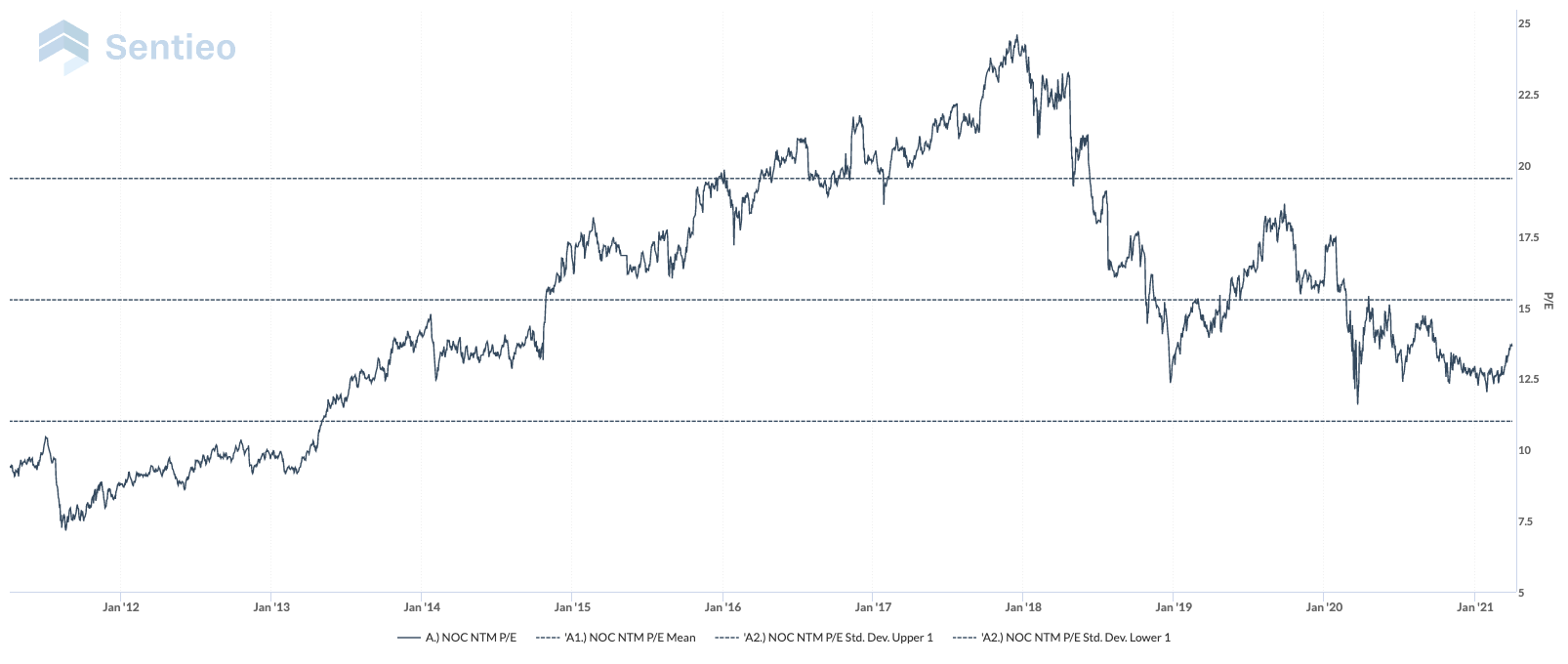

Consistent performers within the defense industry should be rewarded with above average market multiples; but lucky for us these stocks fall out of favor from time to time. Mostly due to short-term fears about the federal budget and defense spending.

Chart from Sentieo

We must go back 10 years with the fears of a government shutdown and defense sequestration to find a lower multiple for Northrop Grumman.

The stock could get cheaper but at these levels we believe the potential long-term rewards are worth the risk.

Dividend History

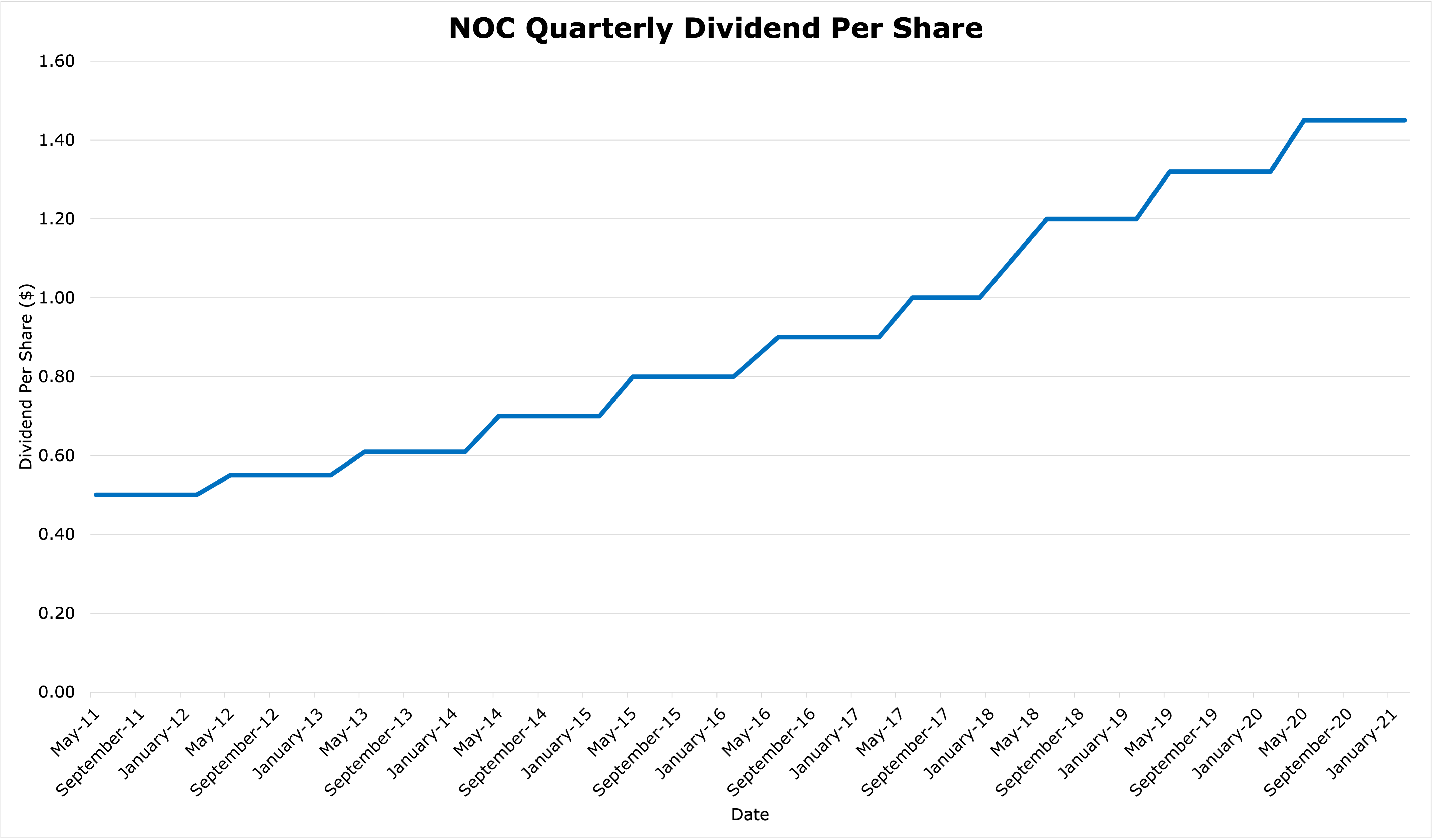

Over the last 10 years Northrop Grumman grew its annual dividend at a compound annual growth rate of 11.23%.

Data from Sentieo

And as we discussed above, Northrop is also a big buyer of its own shares. The company reduced its share count by 34% in the same time span.

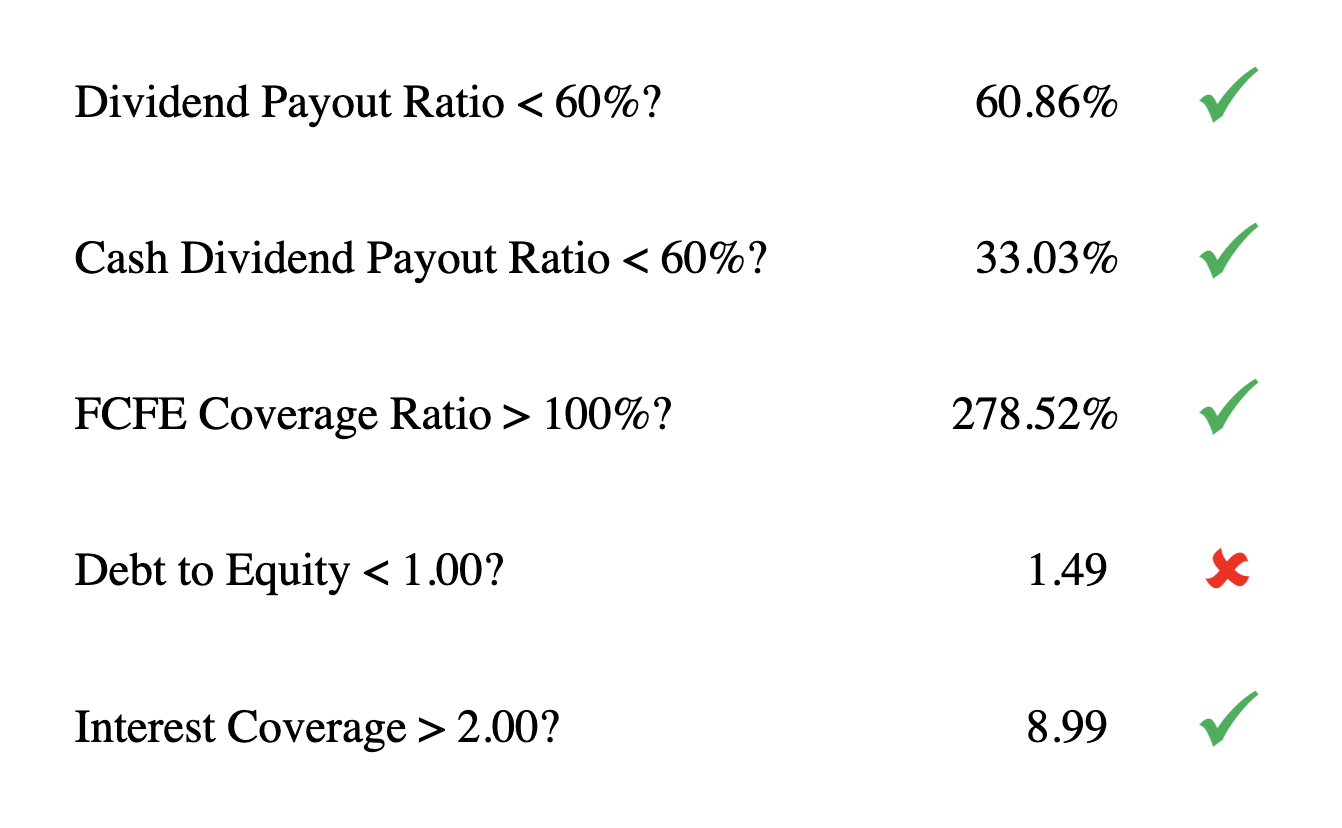

Dividend Safety

Northrop Grumman passes all our dividend safety checklist items except for its Debt-to-Equity ratio. But with an interest coverage ratio of 8.99x and the stability of Northrop’s business, we’re OK with its current level of indebtedness.

Catalysts for Future Price Appreciation & Dividend Growth

Nuclear Triad Monopoly

The United States’ nuclear arsenal is old. A $1.2 trillion program is in the works to update our nuclear triad and its delivery systems: Submarines, a new long-range bomber, and ICBM delivery systems. Northrop is involved with all of it both directly and indirectly.

Sea

Northrop makes the solid rocket engines for the Navy’s sub-launched missiles.

Air

It won the contract to build the new long-range B-21 Stealth Bomber, nicknamed the Raider.

The new bomber will replace the B-1 and B-2 bomber and it might replace the B-52 bomber. The USAF expects a minimum order of 100 bombers with a possible operating fleet of 175-200 bombers.

The cost per plane is estimated to be in a range of $553-$651 million and a total spend of $55 billion for the first 100 planes. This does not include the ongoing costs paid to Northrop for upkeep and upgrades. Full cost details are not being released due to the top-secret nature of the new stealth bomber, but estimates are nearing $80 billion.

The B-21 will be large source of revenue over the next several decades. Northrop's B-2 long range stealth bomber has been in service for the last 30 years and the B-21 is expected to have a service life of 50 years.

Land

Boeing and Northrop were bidding for the nuclear missile program with Boeing expected to win as an under the table bailout for its 737 Max issues. But then Boeing dropped out making Northrop the sole bidder. Boeing dropped out because of Northrop’s 2018 acquisition of Orbital ATK, a major producer of rocket engines. Boeing cited the unfair cost advantages this merger gave Northrop. Northrop now has the power to set the pricing for a $264 billion project.

F-35

The F-35 Joint Strike Fighter is a big catalysts for our position in Lockheed Martin but it’s also a catalyst for Northrop Grumman. Northrop makes the fuselage, avionics, the Distributed Aperture system, and several other components for the jet. In total the F-35 accounts for about 8% of Northrop’s revenue.

The F-35 program is ramping up its production and deliveries to the U.S. and our allies. Over 600 have been delivered to the U.S. out of the 2,456 ordered. Exports to our allies are expected to be in the range of 500-1,000.

Trusted Partner

The U.S Defense Department is risk averse when it comes to procurement. They want to work with companies that they know, trust, and that have delivered in the past. This creates a large barrier to entry for competitors.

The procurement process is also a long cycle with large upfront costs. Competitors need to have the financial resources to survive the bidding process if they hope to win a big defense project. This favors the large incumbents.

The relationship also ensures that the Department of Defense will negotiate contracts that benefit Northrop Grumman to keep them in business for future projects. Most defense contracts are cost plus. The burden of cost overruns falls to the customer maintaining the contractor’s margins and returns. The remaining fixed cost contracts are on older projects where the costs are known making these contracts profitable for the defense contractor too.

Risks

Lower Growth

Large projects like the new bomber and the missile will take time to ramp up and to meaningfully add to Northrop’s revenue, earnings, and cash flow growth. Over the next year or so Northrop might experience below average revenue earnings growth. During this time margins will also come under pressure as the B-21 and missile defense system move into development. We expect margins to come back to higher levels when the programs move into the production phase. We believe the relative weakness in defense names over the last few months and Northrop’s current stock price already reflect these expectations. We believe this short-term weakness gives us a favorable entry price to be rewarded long-term by Northrop Grumman.

Budget Cuts to Defense

Another reason for the short-term price weakness is an expectation for defense budget cuts. This always seems to be a concern when a Democrat is elected President. We saw a slight decline in Clinton’s second term. Then another spending decline in Obama’s first term due to ratcheting down the “War on Terror”. But the long-term trend remains intact.

We have yet to see Biden’s budget plan. Given the increased government spending related to coronavirus we may see defense budget cuts.

The relationship between our military and defense contractors is so intertwined that we can’t risk losing the key providers of our mission critical systems and weapons. Defense budget cuts tend to be mild if at all.

We think the most likely adverse outcome is defense spending remains flat.

Specific Program Cuts

Cuts to specific programs, especially the big ones, will reduce our expectations for future growth. Less orders for the F-35 and new B-21 Raider. Could the new ground base nuclear missile system get cut? Some legislators are questioning the need for our ground-based defense system when we have new nuclear submarines and the new long-range bomber. We think it is unlikely to get cut. You want redundancy in your defense systems especially in something as critical as your nuclear defense systems.

Valuation

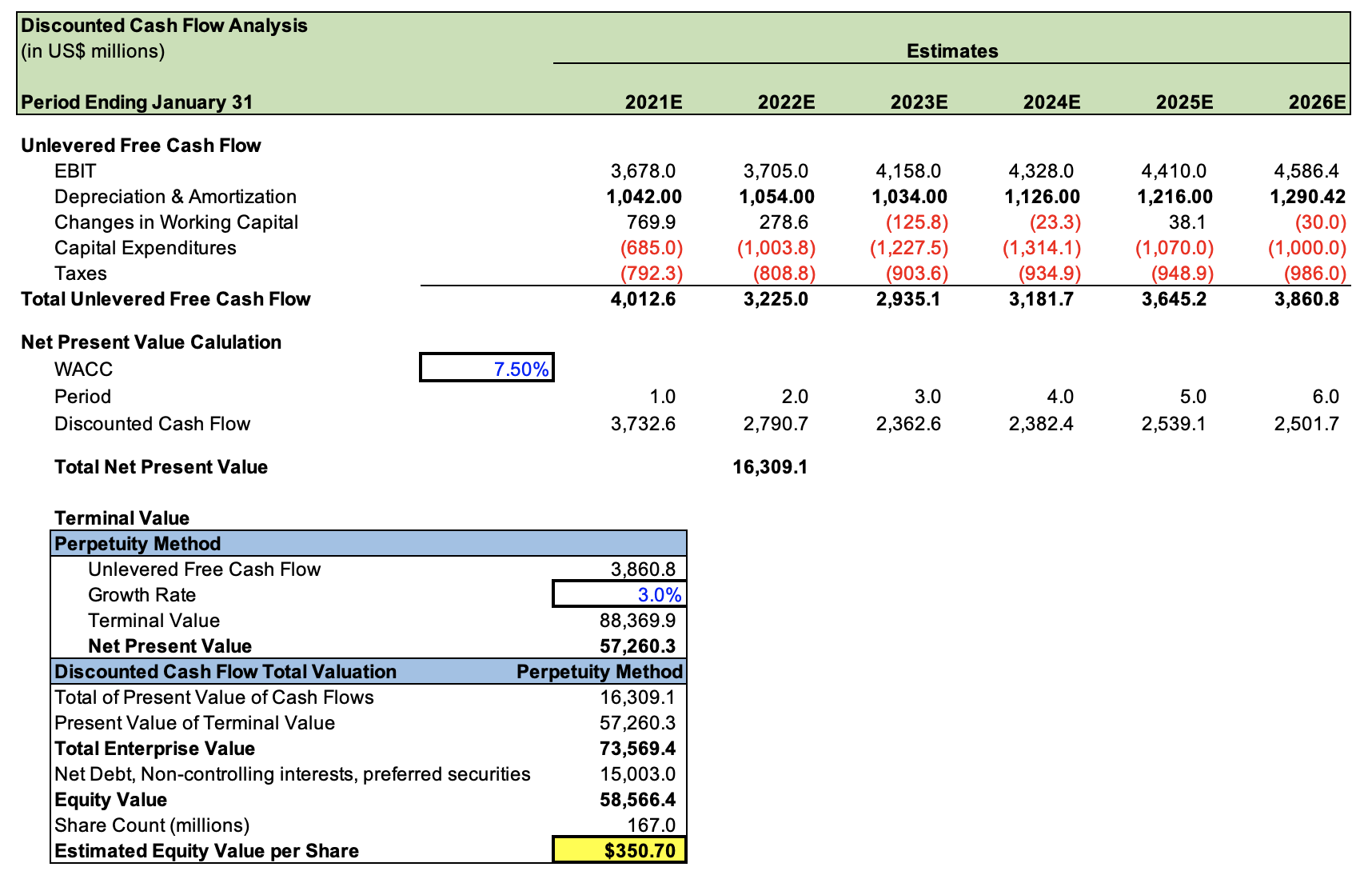

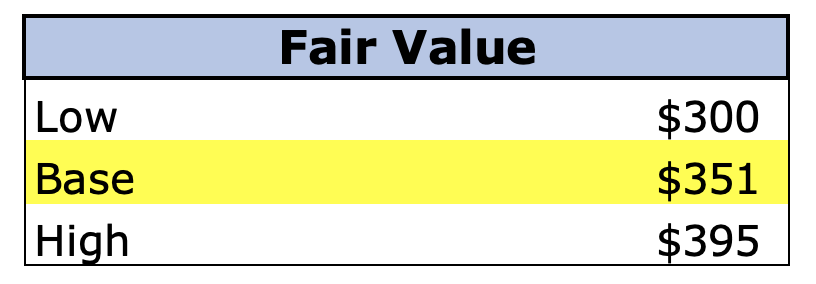

Our base case fair value is about $351 per share based on our DCF model.

Our range of fair value is $300 on our low end and $395 on our high end.

At today’s prices we believe we’re paying a fair price for a high-quality company with the potential for higher returns if our best-case scenario plays out. Given the recent multiple contractions and underperformance of the defense sector, we think our low estimate of fair value is less of a probability than our base case estimate and our high estimate of fair value.