In investing, risk is typically defined as the possibility that actual returns will differ—sometimes significantly—from what you expected, including the potential loss of principal. Although there are many ways to measure risk (e.g., volatility, downside risk, permanent loss of capital, or standard deviation of returns), they all stem from one core idea: risk reflects the uncertainty about future outcomes and the possibility of unfavorable or unexpected results.

Key points that illustrate this definition include:

- Chance of Loss – The potential for losing your original investment (principal) is central to understanding investment risk.

- Variability of Returns – Actual returns may exceed or fall short of expectations; volatility is often used as a proxy for this risk.

- Uncertainty – Even “safe” investments carry some degree of unpredictability related to future performance, interest rates, market swings, or economic conditions.

At AMM, we generally focus on point #1—the likelihood of a permanent capital loss—when evaluating investments. As Warren Buffett famously said, “The first rule of investing is never lose money,” followed by, “Rule number two is never forget rule number one.” Even when the probability of a permanent impairment seems low, the timing and variability of returns always carry some degree of uncertainty, no matter how thorough your research and analysis.

Risk: Bubble (Downside) or Roaring 20s (Upside)?

At its core, risk means that outcomes may deviate—sometimes sharply—from what’s expected, including the potential for capital loss. The current debate over whether we’re in a bubble or only midway through a “Roaring 2020s” illustrates this tension well:

- Historical Observations & Warnings: Goldman Sachs economists point out that historically high price-to-earnings (P/E) ratios tend to precede weaker returns over the following decade. In a report published in the 4 quarter, Goldman’s Chief US Equity Strategist predicted a 3% annualized return for the S&P 500 over the next 10 years, down from 13% annually over the prior decade. This aligns with our belief that “the price you pay ultimately determines your return.” Today’s high valuations suggest a greater possibility of disappointing returns—and increased risk of capital loss.

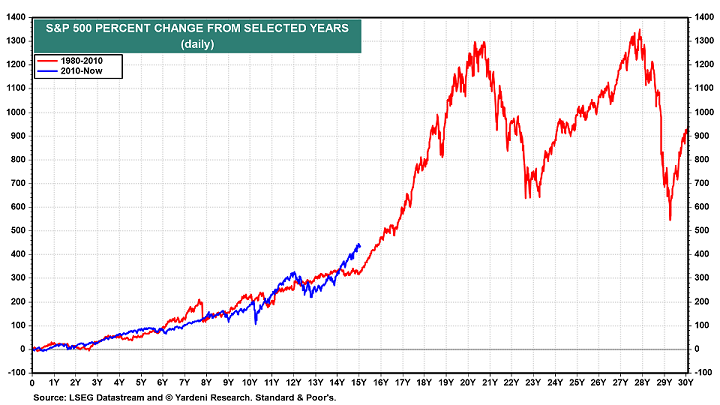

- Counterpoint—Growth-Driven Upside: Alternatively, strong earnings growth and rising productivity could drive the market higher, turning the 2020s into another “roaring” period for stocks. In such a scenario, current valuations might prove justifiable, and bubble concerns could look premature. A Yardeni Research chart comparing the current S&P bull market (launched in 2010) to the 1980–2000 secular bull market raises the question: Are we only in the middle innings of a long rally?

Whether the next decade proves to be a more challenging period or a period of robust growth is unknowable. This very unpredictability—where credible analysts reach opposite conclusions—is the essence of risk. Investors must balance the possibility of overextended valuations against the potential for ongoing economic and earnings growth. This tension underscores why it’s essential to prepare for the unexpected and not rely solely on even the most informed forecasts.

In the end, successful investing isn’t about being certain which scenario will happen; it’s about managing the risk that your predictions might be wrong. Diversification, a well-structured asset allocation, and a clear investment time horizon can help navigate both disappointing markets and continued market strength.

Trump 2.0: Bullish or Bearish?

Few developments illustrate risk and uncertainty quite like a sweeping political shift. The saying “markets prefer gridlock” (where policy changes are incremental) will be tested over the next two years. From our perspective, both upside and downside risks remain in play under the new administration. It is too early to draw hard conclusions about how policies will affect markets and the economy, but below are key considerations:

Bullish Points (Upside Risks)

- Continued Fiscal Stimulus

- Procyclical Government Spending: According to Yardeni Research government spending has risen from a 1.2 to 1.4 ratio of spending-to-receipts, even without a recession, potentially extending economic and corporate earnings growth.

- Tax Cuts & Deregulation: Lower tax rates and reduced regulation can support consumer spending, boost business investment, and raise profit margins.

- Rising Personal Incomes

- Net Interest Income: Higher government debt and interest rates lead to increased net interest payments into the private sector, potentially bolstering consumer demand.

- Energy Expansion

- Oil & Gas Production: Policy-driven support for energy production may stabilize costs, mitigate inflationary pressures, and improve corporate profit margins.

- Potential Productivity Gains

- Lower Costs of Doing Business: Deregulation and tax reforms can stimulate capital investment and enhance productivity, supporting long-term growth.

These factors could underwrite a “Roaring 2020s” environment, fueling higher corporate profits and a buoyant stock market.

Bearish Points (Downside Risks)

- Widening Deficits & Higher Interest Costs

- Federal Debt & Deficits: Tax cuts, defense spending, and rising mandatory outlays can push deficits higher. Larger deficits may raise interest rates, increasing government borrowing costs and potentially crowding out private investment.

- Trade Tensions & Tariffs

- Risk of Trade Wars: Higher tariffs risk retaliation, disrupting global supply chains, increasing costs, and slowing growth.

- Labor Force Constraints

- Deportation & Reduced Government Staff: Policies reducing immigration or government headcount may tighten labor markets, driving wage inflation if productivity doesn’t improve sufficiently.

- Policy Uncertainties

- “Known Unknowns”: From revising major legislation to global geopolitical shocks, ongoing uncertainty can prompt businesses and investors to delay decisions, increasing market volatility.

- Procyclical Stimulus Risks

- Overheating & Boom-Bust Cycles: Extending stimulus in an already-strong economy can trigger inflation or speculative bubbles, which often end in abrupt corrections.

In this bearish scenario, widening deficits, labor constraints, and trade disputes could collectively spark volatility, higher interest rates, and inflation—ultimately undermining growth.

From a risk-management standpoint, Newton’s Third Law of Motion that “every action has an equal and opposite reaction” applies. Each bearish point has a bullish counterpoint and vice versa. Making large portfolio shifts based solely on what might happen has the potential to lead to rapid reversals if events unfold differently. We therefore focus on what we can control in navigating uncertainty: diversification, disciplined asset allocation, a focus on price paid, and maintaining some degree of liquidity and flexibility to adapt to sudden policy or economic changes.

2024 Asset Class Performance & Strategy Commentary*

Domestic Stocks

Year-to-date through 12/31/24

- Large-Cap US Stocks (S&P 500): +25%

- Mid-Cap US Stocks (S&P 400): +14%

- Small-Cap US Stocks (S&P 600): +9%

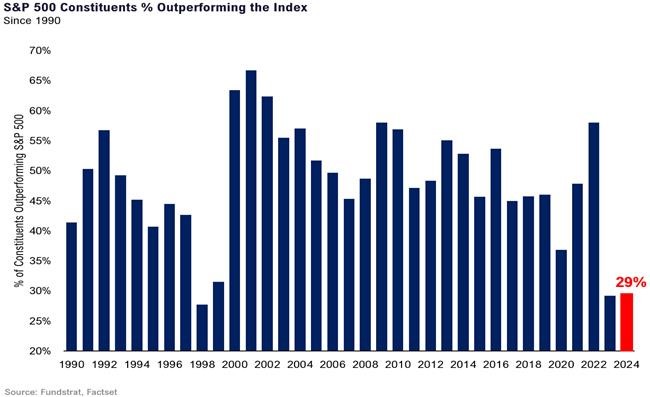

Seven “Magnificent 7” stocks—Alphabet (Google), Amazon, Apple, Meta (Facebook), Microsoft, Nvidia, and Tesla—now represent about 30.5% of the S&P 500’s total market value. They also make up 21.6% of forward earnings and 11.5% of forward revenues, highlighting their powerful influence on the index’s valuations and future profitability. While this concentration creates downside risk if these leaders falter, it also suggests that the remaining 493 S&P 500 stocks may have room to catch up.

Fundstrat research shows that historically few S&P 500 constituents have outperformed the index over the past two years, a level reminiscent of the late-1990s tech bubble. While this might hint at inflated valuations or ‘bubble risk’, the earnings and revenue power of the top stocks is also quite strong. Rather than avoiding these leaders, we believe in owning them at below-index weights, naturally increasing exposure to mid-cap, small-cap, and other large-cap companies. Many of these have more attractive valuations and could benefit if technology-driven productivity gains spread across sectors.

International Stocks

Year-to-date through 12/31/24

- Developed International (EAFE): +4%

- Emerging Markets (MSCI EM): +8%

Developed markets outside the U.S. delivered more modest returns. Europe skirted a mild recession, though its growth remains subdued. Japanese equities experienced a modest increase, supported by corporate governance reforms and shareholder-friendly policies. Emerging markets still face uneven recoveries—especially in China—and geopolitical tensions have continued to limit broader gains. In asset allocation portfolios we continue to hold an effective “under-weight” relative to global market capitalization. However, we continue to see a benefit in allocating a portion of client capital to these investments, given the inherent diversification benefits and significantly lower valuations relative to domestic stocks.

Fixed Income / Bonds

Year-to-date through 12/31/24

- Bonds (Bloomberg US Aggregate Index): +1.25%

After a strong start in 2024, the broad bond market sold off in the Q4 (yields rose) and ended the year with a modest 1.25% gain. Lingering inflation pressures continued to lift yields on bonds of all types in Q4, following the Federal Reserve’s rate cuts, but shorter-term bonds fared much better (Exhibit A). We continue to invest bond portfolios on the shorter end of the maturity spectrum and relative to the aggregate bond index. Expected continued economic strength, worries about an inflation resurgence and concerns about the fiscal deficit should keep bond yields elevated. On the bright side, significantly lower yields abroad have helped sustain global demand for domestic bonds, offering a natural bid that has supported the U.S. fixed-income market overall.

Final Thoughts

If you have any questions about your investment accounts or personal financial plans—or if there have been any recent changes to your investment or retirement objectives—please reach out. We can also provide a current copy of our ADV Part 2 upon request.

As always, thank you for entrusting AMM with your investment and retirement goals.

Your Portfolio Management Team

Individual accounts will vary based on a client’s stated investment objectives, risk tolerance and time frame. We manage several different investment strategies so not every client will have exposure to the securities, asset classes and/or investment strategies described in this section. In addition to growth and/or income oriented asset allocation strategies, we also manage more concentrated equity portfolios that generally carry a higher degree of risk and volatility. Let us know if you want to discuss your specific portfolio strategy in greater detail.