The Big Picture ~ Financial Discipline and Happiness

Global markets are in the midst of a bear market, with developed market stock prices down approximately 20% from the peak reached in early January. This is the 14th of these episodes since 1945. While navigating bear markets is a fact of life for long-term investors, it is never easy. A famous study by behavioral economists Daniel Kahneman and Amos Tversky found that investors feel the pain of loss twice as much as the joy of an equivalent gain. So it is no surprise that bear markets are accompanied by negative sentiment. Add to this the current anxiety around inflation and the seemingly endless pandemic, and the mood of consumers is at the lowest level in more than 50 years.

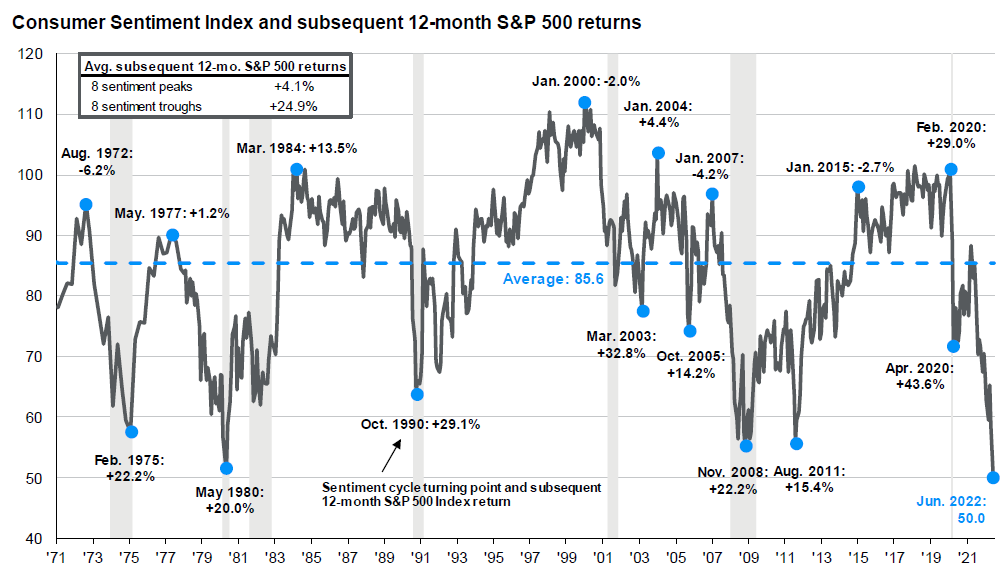

Source: FactSet, Standard & Poor’s, University of Michigan, J.P. Morgan Asset Management Peak is defined as the highest index value before a series of lower lows, while a trough is defined as the lowest index value before a series of higher highs. Subsequent 12-month S&P 500 returns are price returns only, which excludes dividends. Past performance is not a reliable indicator of current or future results.

As with most economic data, these sentiment levels don’t tell us much about the future. In fact, as the nearby chart shows, at inflection points, extremely low sentiment is followed by strong investment returns over the following 12 months. The average 12-month return following a low sentiment turning point was 24.9% over the last 50 years. This highlights a perpetual challenge for the long-term investor. Buying low means buying when negative sentiment is the prevailing attitude. Rowing against this strong current of negativity is difficult, made more so by the fact that additional buying is often followed by more downside in the near term.

There is no easy solution to this challenge. But developing a clear financial plan, and having the discipline to follow the plan is an important first step. A recent study by Northwestern Mutual found that people who work with a financial advisor and those who self-identify as disciplined financial planners not only report lower levels of financial anxiety in their lives, but they enjoy higher levels of happiness and better sleep, too. Shameless plug aside, we don’t think it is a stretch to infer that lower anxiety and more happiness might result from our helping you navigate difficult market environments more successfully. A critical part of a disciplined financial plan is having a plan and following a clear set of investment principles:

AMM’s Investment Principles – Bear Market Edition

Asset Allocation is the Most Important Decision

The diversification provided by asset allocation can help investors better weather bear markets:

- More aggressive investors, those with longer time frames, and those with sufficient liquidity and incomes should view bear markets opportunistically (see below).

- Shorter time horizon investors or those requiring more liquidity from their portfolio should diversify appropriately by incorporating non-stock and historically less market correlated assets.

Volatility is not Real Risk

Risk is often perceived to increase as stocks go down, but actually, stock declines improve future returns all else being equal. The stock component of a portfolio should be treated as the long duration asset that it is. From this lens, volatility creates an opportunity to increase future returns. While not a guarantee of future outcomes, the S&P has never had a 20-year period of negative returns and only a handful of negative 10-year periods. Important caveats:

- For Individual Stocks: Quality and Price Paid is key so that the odds of permanent impairment remain low (i.e. avoid bankruptcy, or “bubble pricing” that may reduce odds of recovery).

- For Funds: Broadly diversified Mutual Funds and Exchange Traded Funds (ETFs) may exhibit varying degrees of volatility but generally offer low odds of impairment with an appropriate time horizon.

The Price You Pay Determines Your Return (All Else Equal)

The greatest benefit provided by bear markets is to allow investors to invest at more favorable prices. Lower prices are GOOD for prospective future returns, all else equal. Returns over long secular bear markets can be improved via dollar cost averaging at lower prices or investing larger lump-sums after a big market decline (even if prices go lower over the short run). Other bear market strategies related to this principle include:

- Standard Rebalancing: Stocks suffer large declines during bear markets, creating opportunities to rebalance out of more conservative assets in to stocks at more favorable prices.

- “Turn in to Crash”: The opportunity to “overweight” within your general asset allocation parameters. There is no exact timing method here – but a bear market nearing the historical average decline (~40%) is a decent time to consider more aggressive buying where prudent and consistent with an investor’s risk tolerance.

- Quality on sale (specific to individual stock strategies): High-quality shares of companies that were previously too expensive can go on sale, declining to attractive levels, creating a buying opportunity.

Time is Your ally

Bear markets tend to amplify the pain of loss as the losses seem to go on indefinitely. It is important to remember:

- Bear Markets End: Investors often make the mistake of extrapolating the recent past far into the future.

- A few of the common refrains from investors during deep bear markets: “at this rate I won’t have anything left”, “I just need to stop the bleeding until the dust settles”, “I can’t take it anymore”, “my account will never recover”, “a 50% loss requires a 100% gain to get even, that will never happen!”. With an appropriate time horizon and diversified portfolio, the odds of any of these statements being true are very low.

- Focus on Time in the Market instead of Timing the Market: Bear markets are historically short-lived. Of the 13 previous bear markets, they have lasted as long as 5 years and as short as 1 month, with the average bear lasting 20 months and declining ~41%. The average bull market lasts 51 months with returns of nearly 160%.

You Can’t Predict the Future

- It is nearly impossible to know how shallow a bear market will be following the 20% threshold. Attempting to sell after a 20% decline in an effort to save you from greater pain does not usually work, as you are forced to make another decision – when to buy back in. Bear markets are often characterized by higher volatility, relief rallies, and big UP days. If you exit down 20%, you run the risk of major whipsaws as you try to re-enter.

- Don’t be a Perma-Bear: Bear markets are accompanied by scary financial headlines, causing some investors to decide to exit the stock market permanently (at depressed levels). History suggests while this may work for a short period during the depths of a bear market, this is a wealth destructive strategy. Staying invested and riding out the storm within the confines of an appropriate asset allocation strategy is generally the best option.

2022 Mid-Year Review and Outlook

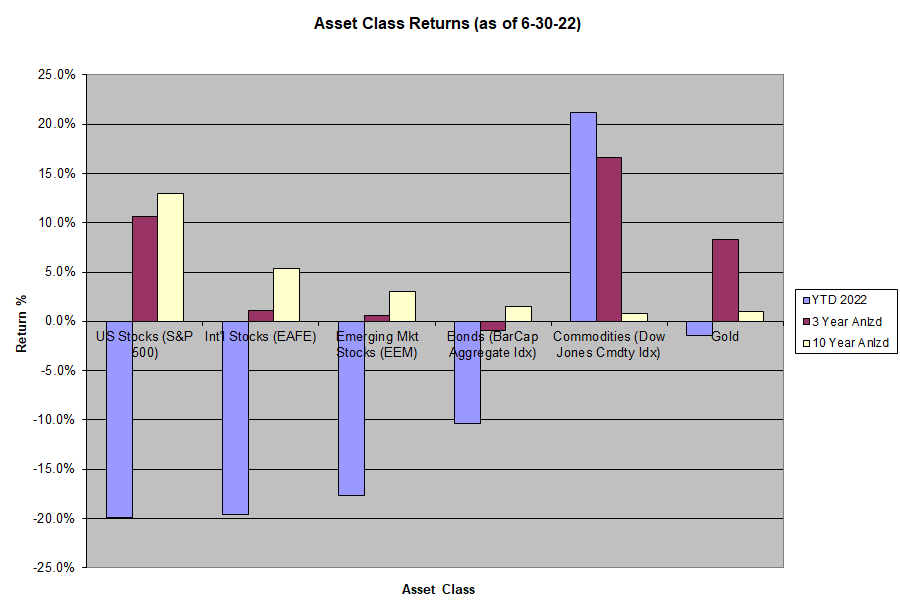

Year to date through 6/30/22.

- Domestic stocks (S&P 500) declined 20%

- Developed international stocks (EAFE) declined 19.6%

- Emerging market stocks (EEM) declined 17.6%

- Bonds (Bar Cap Aggregate) declined 10.4%

- Commodities (DJCI) were up 21.2%

- Gold declined 1.4%

We have updated our asset class return chart to reflect year-to-date returns through June, along with three and ten-year annualized returns for the aforementioned asset classes.

We remain cautiously optimistic that the current bear market will be garden variety in nature, as opposed to more significant downturn akin to the ’08-09 bear market that declined more than 50%. This is based in part on our optimistic case outlined below. We counter this with the bearish case – though we do not view this as the most likely outcome.

Optimistic Case – The Mid-Cycle Slowdown

The Federal Reserve is raising interest rates in an effort to bring down inflation. While this is tightening financial conditions and has increased market volatility, this is occurring against the backdrop of a strong economy experiencing high nominal growth and low unemployment. There is an estimated $2 trillion in excess consumer savings relative to pre-pandemic levels, which, so far has helped to further soften the blow from a higher interest rate regime. While inflation is at the highest levels in decades, some important components of inflation are moderating. Copper, energy products, used-car prices and agricultural commodities have all fallen significantly from their highs reached earlier this year. This bodes well for a softening inflation environment going forward.

Perhaps most notably on the inflation front, is that the growth in money supply has been contracting. In a recent Wall Street Journal Op-Ed, Donald Luskin of Trend Macro noted that “the relationship between money-supply growth, as measured by M2 (currency in circulation plus liquid bank and money-market fund balances) and subsequent inflation has been statistically near-perfect in the pandemic era, with a 13 month lag.” He further noted that “if the relationship with inflation continues, core inflation will be at only 2.3% in 13 months, in June 2023.”

While tightening financial conditions always present unique challenges to businesses and consumers, the weight of the evidence suggests to us that the economy entered this period in a strong enough condition to weather the tightening cycle without significant economic destruction; a “soft landing”. If softening inflation comes to pass, we would expect that the Federal Reserve will back-off from significantly more hiking by year-end. We would expect this to be a bullish outcome for markets and the economy.

Bearish Case – Credit Bubble Bursts

Until recently, markets have been skeptical of the optimistic case as both stocks and bonds have sold off significantly this year. Bearish investors note that the Federal Reserve doesn’t have a great track record at engineering soft landings. Attempts in the late 90s and mid-00s ended badly, causing significant demand destruction in the economy and two severe bear markets. The concern is that the Federal Reserve will go too far in its tightening regime and ultimately “break something”. This could include a significant drop in real estate prices and large corporate sector defaults – both affected by the higher financing costs associated with higher rates. Unemployment would likely spike in this scenario. Inflation could also prove stickier and more entrenched which would mean the Federal Reserve would likely continue on its aggressive rate-hiking path for longer. These are valid concerns and markets have reacted this year to “price in” these possible outcomes.

While we lean towards the bullish case above, ultimately we cannot be 100% certain about any outcome. But regardless of how the future unfolds, by following our investment principles we hope to mitigate real risk, and set portfolios up for better returns when markets eventually recover.

Should you have any questions regarding your investment account(s) and personal financial plans, or if there have been any recent changes to your investment and/or retirement objectives, please contact our office. We can also provide you with a current copy of our SEC Form ADV Part 2, at your request. As always, we thank you for entrusting AMM to help you achieve your investment and retirement objectives.

Your Portfolio Management Team