Marriott is one of the largest hotel companies in the world but it owns very few hotels.

They run an asset-light business model that avoids the significant capital expenditures associated with acquiring, developing, or maintaining hotel properties. This also reduces the financial risk that comes with owning a large real estate portfolio.

Marriott generates revenue through franchising and management contracts with independent property owners. In a franchise agreement, property owners pay Marriott for the right to use the company's brand and operational support. With management contracts, Marriott takes on the responsibility of managing the day-to-day operations of the property.

Also, the revenue from management contracts and franchise fees are more stable and predictable due to their recurring nature and they help shield Marriott from cyclical downturns in the travel industry.

Marriott’s recurring revenue, asset-light business model generates high returns on invested capital and excess free cash flow. The company doesn’t need to reinvest that much capital back into the business to grow so Marriott aggressively returns excess capital back to shareholders through share buybacks and dividends.

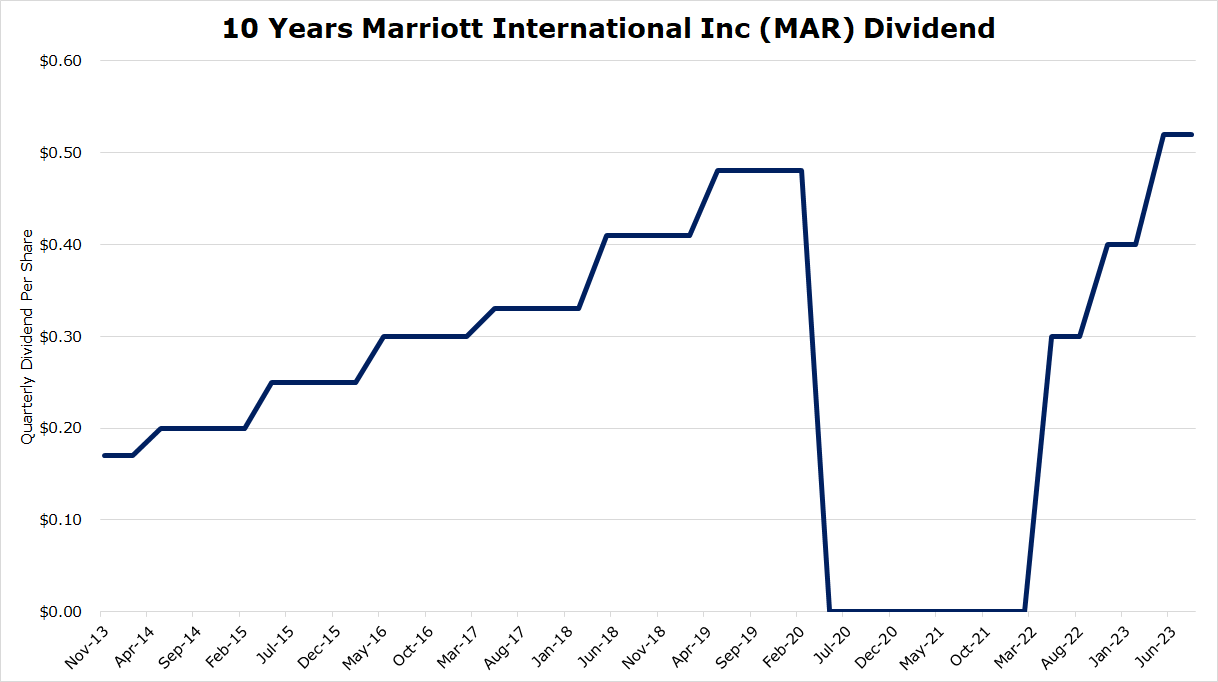

Dividend History

Marriott started paying a dividend in 1998 and increased it yearly until February 2020. In the early stages of the COVID pandemic, Marriott cut their dividend to zero to preserve as much cash as possible.

The strength of Marriott’s asset-light business model can be seen in how quickly they reinstated their dividend and subsequently raised it past its pre-COVID level following the rebound in travel.

Dividend Safety

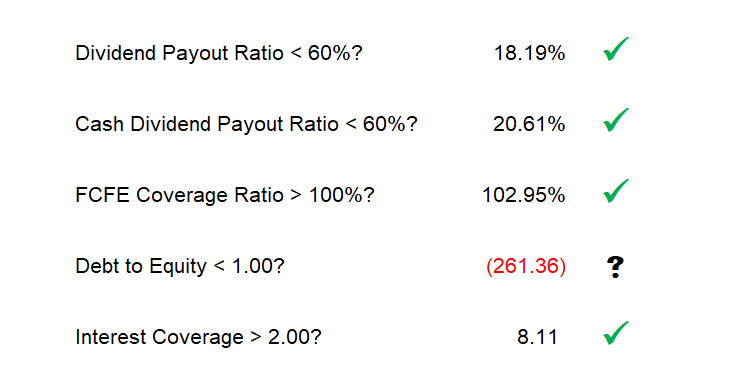

Marriott passes all our dividend safety items except for Debt to Equity. Technically, a negative number is less than 1 but it’s more of an indicator to look deeper into this metric.

Marriott has repurchased so many shares that its equity line item is negative. Marriott’s total debt over the last few years has remained within the $9-11 billion range. Marriott has not been funding its share repurchases with excess debt and its interest coverage ratio of 8x confirms this too.

Quality Factors

Brand

Marriott built its brand on offering consistent high-quality accommodations and amenities. From luxury brands like The Ritz-Carlton to mid-range options like the Marriott Courtyard, Marriott provides its high-quality service to a wide variety of travelers at various price points.

Branding is the weakest competitive advantage. One wrong move can destroy decades of a carefully cultivated reputation. In a highly competitive industry like hotels where consumers have many options to spend their money, you need to use your brand to build stronger competitive advantages like barriers to entry, switching costs, and network effects.

Barriers to Entry

There is an actual physical limit to how many hotels can be built in an area. Then Marriott takes advantage of this scarcity to build a higher barrier to entry with its management and franchise agreements. The average contract starts with 20-year terms with the ability to renew for up to 50 years. Marriott can lock up a prime location and block out competitors for decades.

Switching Costs

Once a property is under contract, Marriott creates switching costs for the hotel owner so that they want to keep renewing their management & franchise agreement with Marriott.

The first cost to switch would be a loss of customer traffic and revenue. If a hotel operator leaves Marriott they’re also leaving Marriott’s reward program which is a big source of bookings.

In 2022, over half of our global room nights were booked by Marriott Bonvoy members. We strategically market to this large and growing guest base to generate revenue.

- 2022 Annual Repor

Do you leave Marriott knowing that your bookings could drop by 50%? Will you join another major hotel brand? Do they have a similar loyalty program? Will it bring in the same amount of traffic & revenue?

The hotel owner is the one carrying the debt on the hotel. A major disruption to bookings could put the hotel in financial distress. If everything is working well with Marriott why would a hotel owner leave Marriott and put their asset at risk?

The second switching cost is incurred if a hotel owner wants to leave Marriott and join another major hotel brand. The hotel owner may have to invest in new amenities, property upgrades, and room remodels to meet the requirements of the new management company. If the hotel owner already meets Marriott’s requirements and if Marriott is delivering on their end then why incur the extra costs to switch brands?

Customer Switching Costs

Marriott also creates the lock-in switching cost for customers with its loyalty program.

The more points you earn in Marriott’s loyalty program the more likely you are to book all your travel through their system to redeem current points and to earn more points for future trips. Marriott essentially “locks” you into their ecosystem because not using your reward points makes you feel like you’re losing money. And loss aversion is a big motivator when we make financial decisions.

Network Effects

Bonvoy is the largest hotel loyalty program in the world and its size creates small network effects for Marriott. The more members Bonvoy has, the more appealing a contract with Marriott is to hotel owners. The more hotels and locations on the Bonvoy platform the more valuable it is for its members. This creates self-reinforcing network effects.

MGM Resorts with over 40,000 rooms in Las Vegas wants access to Marriott’s loyalty program and the revenue it brings.

Beginning in October, several MGM Collection with Marriott Bonvoy resorts will be available for booking on Marriott’s robust digital platforms, including Marriott.com and the Marriott Bonvoy mobile app, with all properties expected to be available by the end of the year.

The addition of another 40,000 rooms in Las Vegas increases the value of Marriott’s loyalty program for its customers too. If you’re booking a trip to Las Vegas your first stop is Marriott’s Bonvoy platform to find any membership deals or to use your reward points.

Catalysts

Bleisure Travel

The ability to work from anywhere is changing how people travel. A new trend in business travel is adding an extra day or two of personal time to a business trip. The trend is significant enough that the term Bleisure, business + leisure, has been created by the travel industry.

Additionally, changing stay patterns have accelerated consumer demand for extended-stay lodging options across multiple product tiers. You heard Tony mention bleisure earlier. I think we've all talked about bleisure. I personally am ready to move on from the term, but it's very, very clear that the blended trip purpose of travel is here to stay, and that's driving incremental room night demand especially what have been traditionally shoulder nights. And it's also clear that a greater portion of the workforce is looking for extended-stay lodging options as they work from new locations, and they have flexibility in terms of where they find themselves officing day-to-day. [emphasis added]

- From Security Analyst Meeting September 2023

The increased demand for rooms due to increased length of stays flows through to Marriott in two ways. First, through Base Management fees which are calculated on the revenue of the hotel. Second, through Incentive Fees which are based on the profitability of the hotel.

Fragmented International Market

Outside the U.S., branding is less prevalent, and many markets are served primarily by independent operators, although branding is more common for new hotel development compared to the past. We believe that chain affiliation will continue to become more attractive in many overseas markets as local economies grow, trade barriers decline, international travel accelerates, and hotel owners seek the benefits of centralized reservation systems, marketing programs, and loyalty programBased on lodging industry data, we have an approximately 16 percent share of the U.S. hotel market and a four percent share of the hotel market outside the U.S. (based on number of rooms)

- 2022 Annual Report

Hotel branding is less common outside the U.S. with a lot of international markets being served by independent operators.

As international travel continues to grow and trade barriers decline, partnering with a global brand like Marriott that has a large loyalty program to drive traffic to your hotel becomes more enticing.

Marriott recently bought the City Express brand of hotels. The acquisition brings in another 17,356 rooms that serve the countries of Mexico, Costa Rica, Colombia, and Chile and Marriott will help accelerate the brand throughout the Caribbean and Latin American markets.

Risks to Consider

Tarnished Brand

Marriott’s success is built on maintaining strict brand standards and quality assurance, ensuring that properties bearing its brand name provide consistent and high-quality experiences for guests. If Marriott loses this operational focus then the customer experience will deteriorate and bookings will decline.

Marriott’s franchisees are a part of Marriott because of its stellar brand reputation and the increased revenue Marriott’s booking platform generates. If revenues decline for Marriott’s franchisees because of Marriott’s tarnished brand then its franchisees will look to switch brands further eroding the value of Marriott’s platform and network.

Once the perception exists that Marriott is low-quality then it takes a very long time to win customers back and to change their minds. By the time Marriott fixes its reputation, it might be too late.

Higher Interest Rates

Because of Marriott’s asset-light business model, it is highly reliant on the financial health of its franchisees and their properties.

The construction or purchase of commercial properties like hotel buildings are typically financed with floating rate debt. When times are good and interest rates are low, floating rates allow borrowers to access low-cost financing to build new hotels, to operate their hotels at a greater level of profitability, to prepay or refinance loans into long-term lower fixed rates, or to sell their assets at a profit.

But when interest rates are higher, borrowers have to pay more interest on their debt and the cost to hedge their interest rate risk increases. These higher finance costs decrease the hotel’s profitability. Only Marriott’s incentive fee revenue is based on each hotel’s profitability and incentive fees accounted for 2.55% of Marriott’s total revenue in 2022. But if the hotels are no longer profitable because of their higher financing costs then the hotels may go out of business diminishing the revenues Marriott earns on management contracts and franchise fees.

Higher rates and higher borrowing costs lower the market value of a hotel. Any potential buyer wants a lower price to compensate them for the higher finance costs and the extra risk that comes with it. The lower market value increases the loan-to-value ratio on the property for the current owner increasing the financial risk to the property owner.

Higher rates make it more expensive for its franchisees to buy existing properties or build new hotels which can slow Marriott’s growth.

Marriott also has its own outstanding debt. Higher rates increase its borrowing costs and its refinancing costs cutting into the company’s profitability.

The borrowing costs for consumers increase too lowering their propensity to spend. Travel isn’t a necessity in life so it’s easy to cut it from a budget.

Pandemics

We just witnessed what a global pandemic can do to the travel industry. Before COVID, the last global pandemic of a highly transmissible virus was the Influenza pandemic of 1918. This does not mean another pandemic won't happen for at least another 100 years. We had some recent near misses with MERs, SARs, Bird Flu, and Swine Flu. We hope another pandemic doesn't happen for at least another 100 years but we can't predict it and we don't base our investing process on hard-to-predict, low-probability, high-impact events.

We focus on high-quality companies that lead their industry, generate high returns on capital, and return significant amounts of excess capital back to their shareholders. This is Marriott. But if we’re looking for non-standard business risks that could significantly impair our investment we have to acknowledge what another global pandemic could do to Marriott.

War

There’s a war in Ukraine and Israel just declared war.

Right now these conflicts are contained within their respective regions. But there is always a chance that a “contained” conflict expands and engulfs more of the world. The desire to travel and the ability to travel could decline if these regional conflicts expand.

Also, International growth is a big focus for Marriott and broader global conflicts will hinder Marriott’s plan to grow internationally.

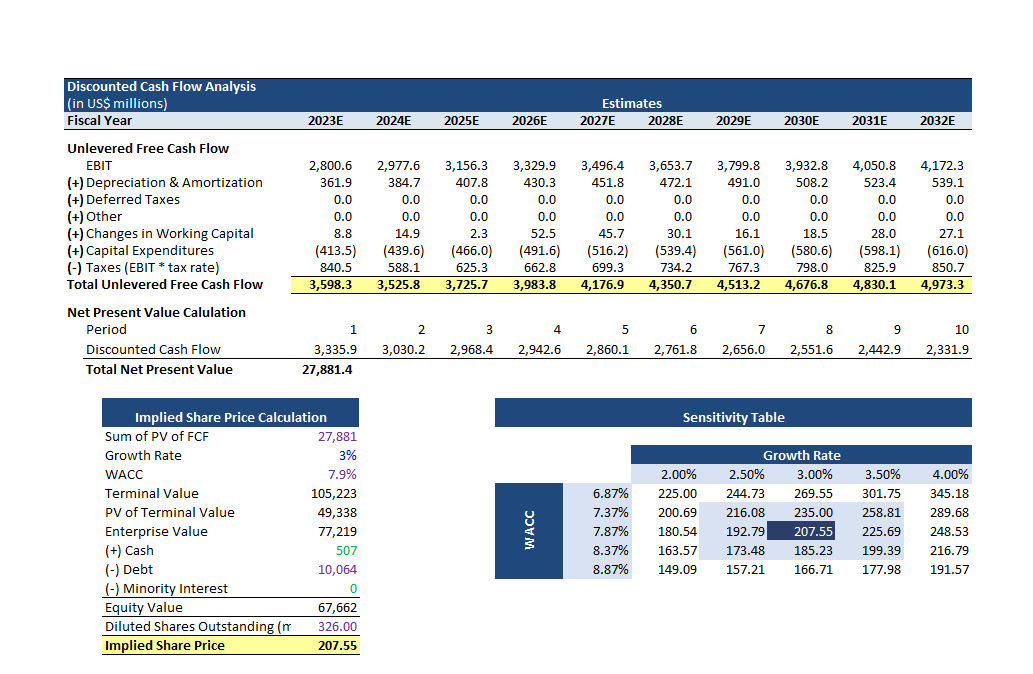

Valuation

Our base case discounted cash flow model has Marriott’s EBIT margins at 12.6% and revenue growing 7% next year and then declining to 3% over the next 10 years. This creates a fair value estimate of $207 per share.

Marriott’s EBIT margin last year was over 16% and management believes they can get to 18%. If they can't get to 18% but management can maintain 16% EBIT margins with the same growth rates as our base case then Marriott is drastically undervalued.