Few companies have become as central to our daily lives as Alphabet, the parent company of Google.

Founded in 1998 by two Stanford Ph.D. students, Larry Page and Sergey Brin, Google began as a simple search engine. Their goal was to organize the world's information, and they did it so well that "Googling" quickly became a verb. Over the years, Google transformed from a search engine into one of the most dominant companies in the world with a market cap of over $1 trillion.

Alphabet's dominance is built on powerful network effects combined with high barriers to entry.

But maybe Alphabet’s dominance is starting to crack?

The Department of Justice is pursuing an antitrust lawsuit against Alphabet, challenging its search distribution practices and exclusive deals. For the first time in decades, Google Search faces genuine competition. AI-powered search engines have gained traction, showing early promise in rivaling Alphabet's search dominance.

These developments create uncertainty, and while markets typically dislike uncertainty, it can also present a compelling investment opportunity if fears prove exaggerated.

Given Alphabet's robust portfolio of businesses, this short-term uncertainty may be creating an opportunity to invest in a dominant high-quality company at a great price.

Quality Factors

Alphabet boasts a diverse portfolio of businesses, with its strongest competitive advantages lying in search, video streaming, cloud computing, and mobile operating systems. These advantages stem from a powerful combination of network effects, high barriers to entry, and significant switching costs. Rather than dissecting each factor individually, we'll examine each business division and the quality factors that define them.

Google Search

Barriers to Entry

Google Search has some of the strongest barriers to entry in the tech industry. Google processes over 8.5 billion searches daily, and this enormous scale gives it a data advantage that’s nearly impossible for competitors to match. With this vast amount of data, Google continuously refines its search algorithms, improving the relevance and accuracy of its results.

Another significant barrier is the enormous cost of building and maintaining the infrastructure for a global search engine. A new competitor would likely need to invest hundreds of billions of dollars to match Google Search's scale and scope. Few companies possess the financial resources to even contemplate competing with Google.

Additionally, Google’s partnerships with web browsers like Mozilla’s Firefox, device manufacturers like Apple and Samsung, and its browser Chrome give it an entrenched position as the default search engine for billions of users worldwide. This further raises the difficulty for new entrants to gain market share.

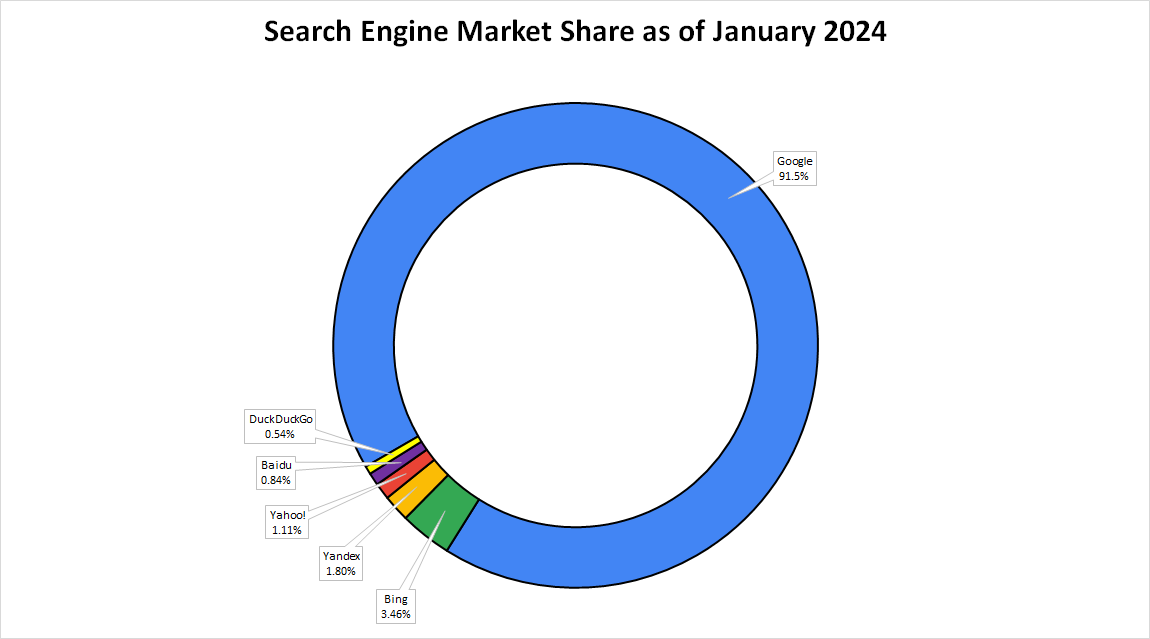

As of January of this year, Google Search’s worldwide market share was 91.5% and since 2015 Google’s market share has held steady between 91 to 92.5%.

Switching Costs

Although it's easy for users to switch search engines, Google has created some switching costs for its users with trust. They trust Google is providing them with the highest quality information as fast as possible.

The highest switching cost exists with advertisers.

Google Ads dominates the digital advertising space, accounting for over 39% of the global digital ad market in 2023. Many businesses have tailored their online marketing strategies around Google's platform. Switching to a different system would require not only relearning new interfaces but also reworking and possibly rebuilding entire ad campaigns. This time and effort make it costly for advertisers to move away from Google.

Network Effects

Google Search benefits from powerful network effects. As more people use Google, the company collects more data, which helps it deliver even better search results. This attracts more users, creating a self-reinforcing cycle. The more users and data Google has, the more attractive its advertising platform becomes to advertisers. They can precisely target potential customers, increasing their return on ad spend and boosting profits per campaign.

YouTube

Network Effects

YouTube's main competitive advantage comes from its strong network effects. YouTube has over 2.5 billion monthly active users worldwide. Creators flock to YouTube because of this massive audience base seeking to build a name and business for themselves, while viewers are drawn to the endless variety of content—whether it's educational videos, entertainment, or live streaming. This dynamic creates a self-reinforcing cycle that has made YouTube the go-to platform for video content, making it difficult for competitors to gain traction.

Barriers to Entry

The scale of YouTube's content library and user base creates a significant barrier to entry. YouTube is often described as the second-largest search engine in the world with 3 billion searches per month. Any new video platform would struggle to match the variety and volume of content available on YouTube. More than 500 hours of video are uploaded every minute. Additionally, the costs of storing and streaming such vast amounts of video content are substantial, deterring potential competitors.

Google Cloud

Switching Costs

Google Cloud's main competitive advantage lies in its high switching costs. Once a company has built its IT infrastructure on Google Cloud, migrating to another provider is often complex, time-consuming, and expensive. Many businesses rely on Google Cloud for critical services like data storage, machine learning, and software development tools. Rebuilding these systems on another platform can result in downtime, costly system overhauls, and a significant investment in training employees to use new tools. According to research, nearly 80% of businesses experience vendor lock-in with their cloud provider, which means they are more likely to stick with Google Cloud even if competitors offer lower prices.

Barriers to Entry

The cloud computing market has extremely high barriers to entry due to the massive infrastructure investments required. Google has invested tens of billions of dollars in its global network of data centers to support its cloud services, providing a vast infrastructure that is difficult for any new player to replicate. In 2023, Google Cloud operated in over 200 countries and territories, with 38 cloud regions and over 100 availability zones. These vast investments and extensive reach create a significant obstacle for potential competitors, as it would take years—and billions of dollars—to build a comparable infrastructure.

Android and Google Play

Network Effects

Android benefits from strong network effects in the mobile operating system market. The large number of Android users attracts app developers, which in turn makes Android more attractive to users. This creates a self-reinforcing cycle that strengthens Android's position.

Barriers to Entry

The smartphone operating system market has extremely high barriers to entry. Developing a new operating system and convincing device manufacturers to use it would be an enormous challenge. The existing ecosystem of apps and services for Android creates a significant hurdle for any new entrant.

Devices & Other Bets

These divisions lack the strong competitive advantages of Alphabet's core businesses. However, the Hardware/Devices segment can create some switching costs for users deeply invested in the Google ecosystem and its software services.

Other Bets represent investments in potential technologies that could develop significant advantages if successful. Waymo, Alphabet's self-driving car company, is the most advanced and holds the highest potential to create network effects and high barriers to entry.

Catalysts

Digital Advertising

People are spending an increasing amount of time online.

In 2024, the average person spends about 7 hours online daily using computers and smartphones. Businesses must establish a presence where their potential customers are, especially as e-commerce claims an increasing share of total retail sales.

Digital advertising platforms offer unparalleled precision in targeting specific audiences. Through data analytics, businesses can reach potential customers based on their demographics, interests, and online behavior. This precision increases a business's return on ad spend (ROAS).

While total ad spending will grow alongside the economy, digital advertising spending will grow much faster as ad dollars shift increasingly toward digital channels.

From Quartr

PwC forecasts that digital advertising will grow at a 9.1% CAGR from 2022 through 2026, reaching $723 billion by 2026. It is also on track to become a $1 trillion market shortly thereafter.

This rising demand for digital advertising will drive up costs per impression and click. Companies with the most extensive digital advertising real estate stand to gain significantly from this ongoing trend.

Alphabet owns two of the world's largest digital ad platforms: Google Search and YouTube. YouTube's user base alone exceeds 2.5 billion.

Cloud Computing

In 2023 the cloud computing market was valued at $677 billion. From 2024 to 2032 the cloud computing market is expected to grow at a compound annual growth rate of about 15%. By 2032 the cloud computing market is expected to be $1.87 trillion.

4 main factors are driving this growth.

- Digital Transformation: Businesses across industries are increasingly adopting cloud services to modernize their operations and improve efficiency.

- AI and Machine Learning: The rising demand for AI and ML capabilities is pushing more companies to leverage cloud infrastructure.

- Edge Computing: The integration of edge computing with cloud services is opening new growth opportunities.

- Multi-cloud and Hybrid Cloud Strategies: Organizations are increasingly adopting multi-cloud and hybrid cloud approaches, driving overall cloud adoption.

Google Cloud with a 10% market share is the third largest cloud infrastructure provider behind Amazon AWS (33% market share) and Microsoft Azure (20% market share).

As long as Google Cloud remains a leader in cloud computing it is well-positioned to capitalize on this long-term secular growth trend.

AI

AI is an emerging technology with the potential to become a major technological advancement, impacting the entire economy and society. It's tempting to label AI as a disruptive force that will upend the current global tech hierarchy, with major companies like Alphabet being outcompeted by new AI-first tech companies.

But, what if AI is a sustaining technology, allowing current global tech leaders to maintain and extend their lead?

Building the AI future is capital-intensive. It demands more data centers with vast amounts of GPUs, CPUs, and networking equipment. It requires further cloud infrastructure investment to increase AI use and distribution. Companies must hire the best AI researchers, data scientists, software engineers, and data engineers. They also need to continually invest in research and development to keep their AI products at the forefront of technology.

Who's better positioned to lead in AI than current major tech leaders like Alphabet?

They already possess the computing resources and data centers to deploy AI. They have the cash flow and balance sheet to fund massive investments in AI infrastructure expansion. They can attract top AI talent. Most importantly, they have distribution. Alphabet's integration of AI across its wide product offering—Gmail, Search, Android, Google Cloud, YouTube, Workspace, and NotebookLM—creates an ecosystem where every service reinforces the others. This enables growth across multiple platforms and strengthens Alphabet's competitive advantages.

Risks

Anti-trust

Google faces an antitrust lawsuit due to its widespread search distribution and exclusive deals with Apple, Samsung, and Mozilla.

From the Judge’s opinion on August 5

“roughly 50% of all general search queries in the US flow through a search access point covered by one of the challenged contracts,” including 28% covered by the Google-Apple Internet Services Agreement (ISA), 19.4% through Android OEMs and carriers, & 2.3% through other 3rd-party browsers.

The DOJ recently submitted its formal remediation plan and the most impactful provisions are:

- Terminating exclusive search deals like it has with Apple to be the default search engine.

- Require device manufacturers to show a choice screen for users to choose which search engine they want to use in their browser.

- License its search engine query data to others.

- Block Alphabet from buying or investing in other search and advertising companies including new AI companies.

- Divest from its Chrome Browser Business

The termination of exclusive search deals could benefit Alphabet in the short term, saving it about $20 billion in payouts that directly impact its bottom line. But in the long term, will the end of exclusive deals and adding a choice screen weaken Google's search dominance?

Fewer searches mean less data for Google to improve its search algorithm, potentially leading to less accurate results. This could cause both users and advertisers to gradually migrate to competing platforms, creating a negative feedback loop that erodes Google's dominant market position.

Blocking Alphabet from investing in advertising and search companies could put them at a real disadvantage just as competition is coming from new AI-focused search and advertising companies. While this prevents new competition from being stifled through acquisitions, it also prevents Alphabet from catching up in AI if its homegrown endeavors falter.

The most perplexing provision is the divestiture of Chrome. Alphabet did not acquire Chrome to prevent competition, Chrome was built internally. Chrome has earned its 67.53% global market share as of November 2024 by being better than its competition, not through anti-competitive backroom deals.

Chrome's market share likely wouldn't change after a sale, but this would remove a major search query source from Alphabet, especially if Chrome must let users choose their primary search engine. As mentioned earlier, fewer Google searches means less data to improve its search algorithm. This could lead to less accurate results, causing Google's network effects to work in reverse and weakening its dominant position in search.

AI Search

The argument against Google Search is that its entire advertising platform relies on serving text-based ads alongside 10 blue links generated for each query. In contrast, new AI-powered search engines will provide more comprehensive answers, potentially drawing users away from Google's traditional format and eroding its search dominance.

A related concern is that if Google abandons the 10 blue links model and shifts towards AI-powered search, its costs per query will increase significantly.

From BG2 Podcast

it costs a hell of a lot more, right, to provide answers than it did to provide ten blue links. So if you say like, what's it cost to provide ten blue links, it's about a third of a penny or less per query. Now what does it cost to do that for 750 tokens today? And of course this will go down over time. But it's ten x more, right? It's four cents per query. And then if you look at the refinement of queries that's really going on. So a lot of times, Bill, what they do is they, they'll send back these ten blue links and then they'll use that as their prompt. Right, to re query, the engine. This could be up to 50 x more expensive to serve an answer, a high quality answer to the consumer versus ten blue links. So your cost goes up a lot.

Google faces potential market share loss to AI-first search engines and a possible margin collapse. However, these higher search costs also impact AI search engines, which currently depend on external funding for their operations. Whereas Google leverages its substantial cash flow to fund its AI initiatives.

Consumer behavior presents another challenge. While Google is free, Perplexity and OpenAI's ChatGPT require paid subscriptions for full AI search features. Will consumers pay for search after decades of free access? Or can these new players rapidly develop and scale advertising networks to self-finance their growth?

Distribution is another hurdle.

Google Search is integrated into the most popular web browsers. Chrome holds a 67.5% market share, Safari (which uses Google Search) has 18.22%, and Firefox (with Google as its default) claims 2.6% — totaling around 88% market share as of November 2024.

OpenAI is considering building its own web browser. Apart from user experience and the time needed to build a web browser, OpenAI also has to overcome the switching costs involved with converting current Chrome Users to a new browser.

For the time being, Google Search remains the default search engine for Samsung phones and iPhones, two of the world's most widely used smartphones. While it may seem trivial, accessing Perplexity and ChatGPT requires opening a separate app, creating an additional mental barrier for users.

Google hasn't faced real competition in a long time. AI-driven search, however, could be classified as a disruptive technology, potentially reshaping the search landscape.

AI Capital Cycle

The capital cycle theory, as described in Capital Returns: Investing Through the Capital Cycle, argues that fluctuations in capital supply within an industry affect long-term investor returns.

The capital cycle tends to go through 4 phases.

- Boom Phase: In the early stages of the cycle, high profitability and attractive returns lure new capital into the industry. Investors and companies often overestimate future demand growth, leading to excessive capacity expansion.

- Overcapacity: As capital pours into the industry, competition increases. Prices may fall, profit margins shrink, and returns on investment decline. Excessive supply leads to overcapacity.

- Downturn Phase: As profits fall and returns deteriorate, capital exits the industry. Some firms may go out of business, and others may halt expansion plans. This creates a leaner competitive environment.

- Recovery Phase: With less capital in the industry and reduced competition, survivors are able to benefit from increasing profitability. The reduction in supply and capacity positions remaining firms to thrive, improving their returns.

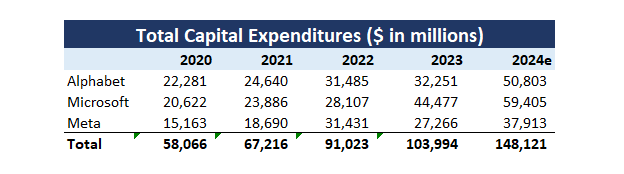

The CAPEX spend at just Microsoft, Alphabet, and Meta is set to grow by around 48% in 2024. The total expected CAPEX spend between these three companies is expected to reach $148 billion.

This insane sum of money is going towards building out their AI applications and the Capital Cycle immediately comes to mind.

- Boom Phase (Current): Unprecedented capital investment in AI from major tech companies. This surge is driven by high expectations for AI's potential and the fear of falling behind competitors.

- Potential Overcapacity: As these companies rapidly expand their AI capabilities, we might see an oversupply of AI products and services. This could lead to price pressures and reduced profit margins as companies compete for market share.

- Possible Downturn: If AI applications don't generate the expected returns or if demand doesn't meet the inflated expectations, we could see a slowdown in AI investments.

- Eventual Recovery: After a potential shakeout, surviving companies with the most efficient and effective AI solutions could benefit from a less crowded market and potentially higher returns.

If Alphabet invests excessively in AI and the economic reality doesn't match current optimistic assumptions, its returns on investments could be disappointing. Then we as investors should expect lower returns from our investment in Alphabet.

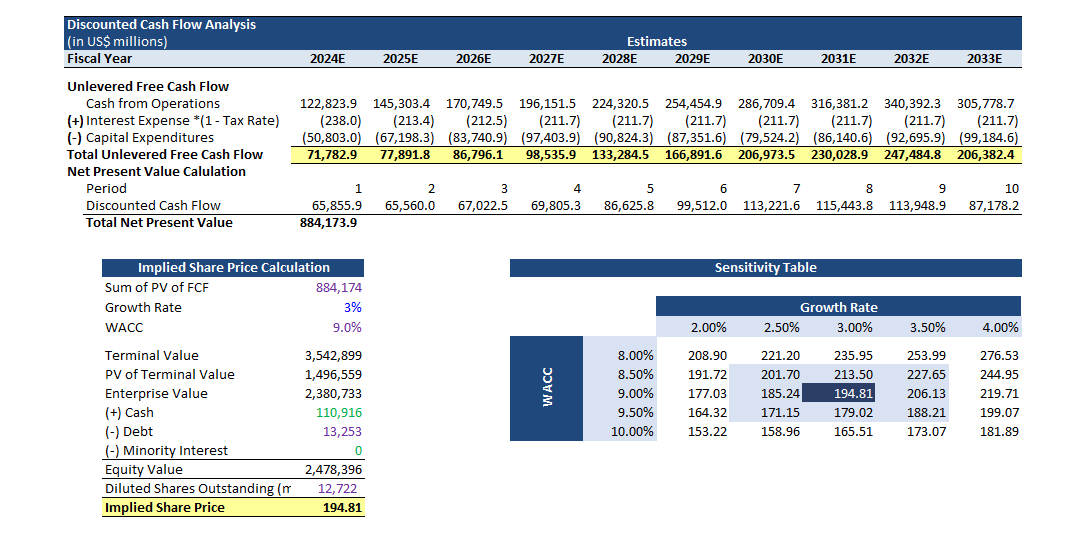

Valuation

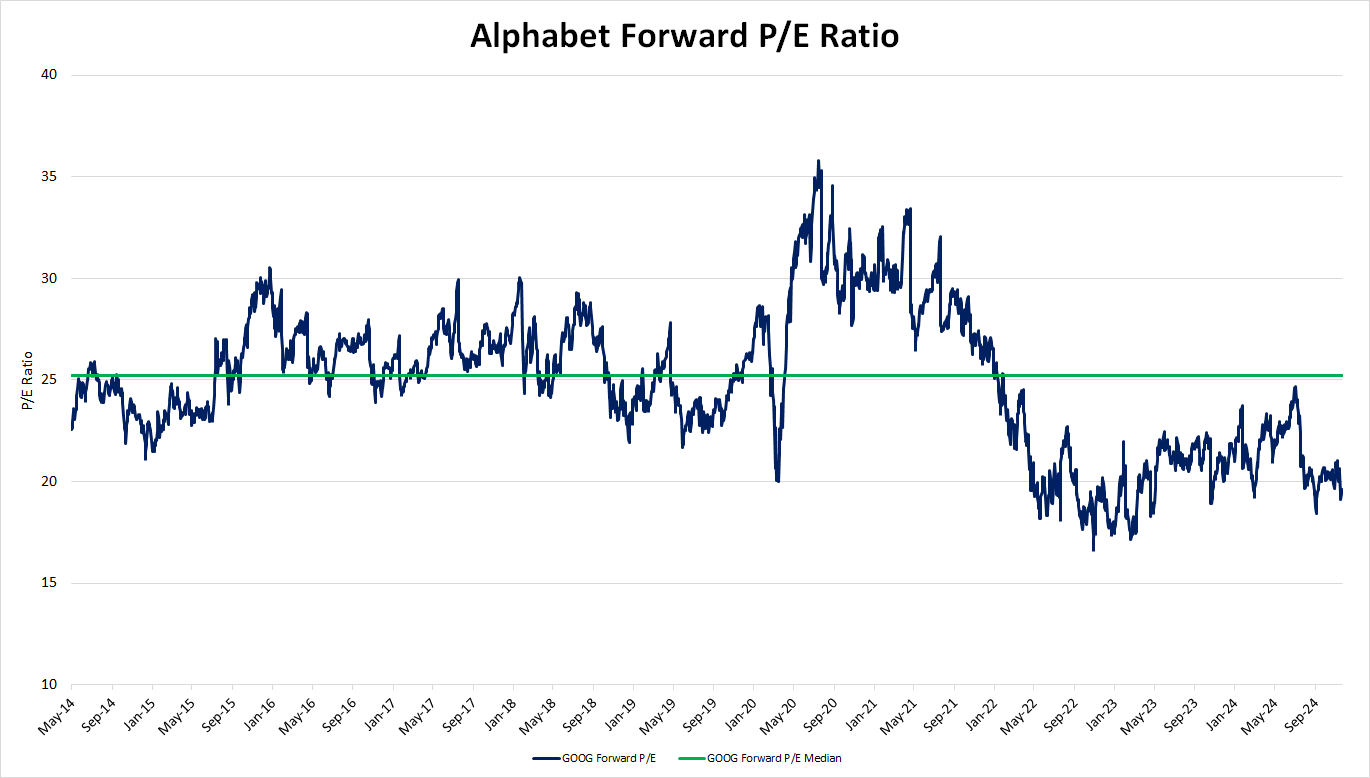

Alphabet's stock is trading at nearly its lowest Forward P/E ratio in a decade.

And based on a traditional discounted cash flow model our estimate of fair value is ≈ $195 per share.

Alphabet (GOOG) currently trades around $172.98 a share.

The Recency Bias often leads stock market participants to place too much weight on recent information. Current concerns about AI competition and the DOJ lawsuit, while valid, are overshadowing Alphabet's long-term structural advantages. This creates an opportunity to invest in a high-quality company that dominates several industries experiencing long-term secular growth trends.