Time is often cited as the most important factor in investment success. On average, assets tend to rise in price over time. So “just hang in there”, goes the conventional advice. “You’ll make money over time. Remember, investing isn’t about timing the market, but time in the market”. There is truth in these statements. The great power of compounding interest, a key benefit of investing vs. short-term speculation, can only be realized over time. But advice based around investing time frames is often incomplete. What specifically you invest in, the price you pay, and how the future unfolds are all critical to your investment outcomes.

Long-term investing adages tend to center around stock index returns. For good reason. Individual stocks are subject to idiosyncratic risks, and no prudent investment advisor would suggest investing all or a majority of your assets in just a few stocks. But broad baskets of stocks like those in a stock index can diversify away those idiosyncratic risks.

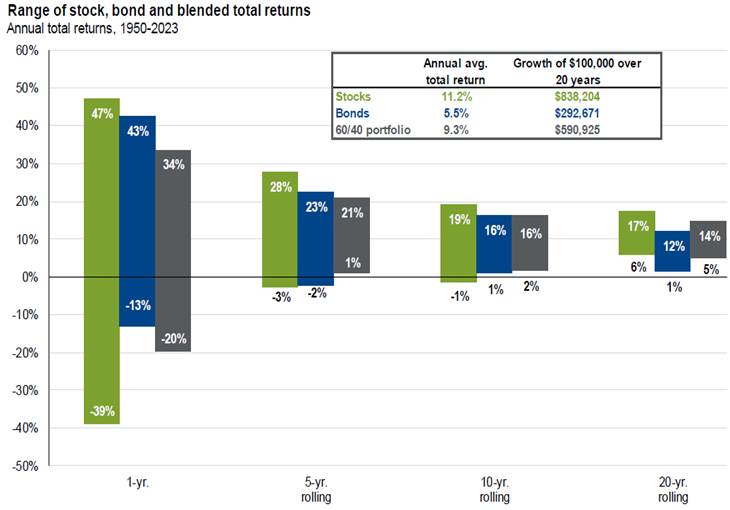

For example the most widely followed domestic stock index (S&P 500 and its predecessor S&P 90) has compounded at an annualized total return of ~ 10% since 1928. Total returns include reinvested dividends. But a typical investing lifetime isn’t 95 years. An astute saver who starts investing young may have 50-60 years, but we suspect for most, the investing time frame is significantly shorter. The “good news” is that the S&P 500 has never had a negative total return over a 20 year period (Exhibit A).

However, since 1950 there have been a handful of 10 year periods where the S&P 500 total return annualized at a negative rate of return. There have been several more 5 year periods of rolling negative returns, with the worst at around -3% annualized.

Exhibit A

Source: Bloomberg, FactSet, Federal Reserve, Robert Shiller, Strategas/Ibbotson, J.P. Morgan Asset Management

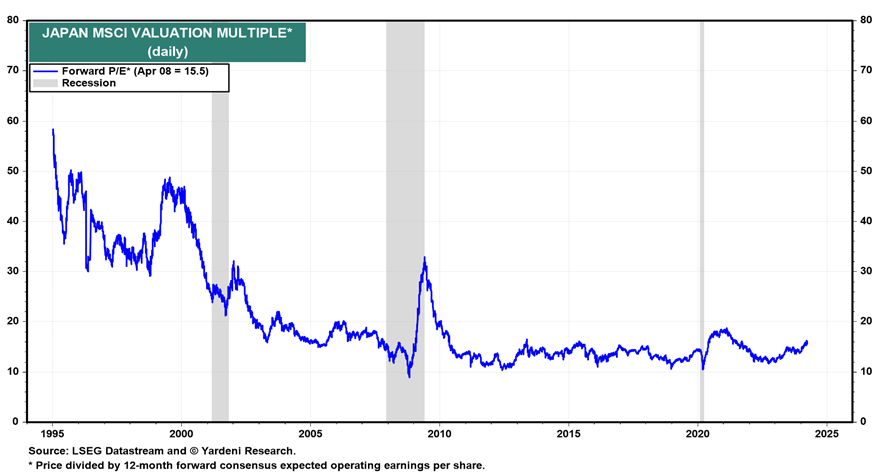

For many investors, 10 years may be considered long-term. But as history suggests, it hasn’t been long enough to avoid negative outcomes in large-cap US stocks. A more extreme example of long-term investing disasters comes from Japan. An investor in the Nikkei 225 over a 35 year period from 1989 to present experienced no return (Exhibit B). After 14 years the investor would have been sitting on a loss of nearly 78%. So yes, invest for the long-run. But be careful about what you invest in!

Exhibit B

Source: St. Louis Federal Reserve Bank

To paraphrase famed investor Howard Marks, “there are no bad assets, just bad prices”. Put another way, the price you pay for any investment determines your return. Pay too high a price, and even the highest quality asset will yield poor investment results. Pay a low enough price, and even an asset of below average quality will earn a handsome return. It is not coincidental, in our view, that Japan’s poor multi-decade stock market performance followed a massive stock market bubble with some of the most expensive stock valuations (by P/E ratio) in history (Exhibit C).

Exhibit C

Further complicating matters for the long-term investor is the future. Human beings are pretty bad at predicting it. But to invest is always about foregoing consumption today in the hope of having more wealth in the future. This leads many investors to assume that predicting the future correctly is the key to investment success. Unfortunately the track record of most in the prediction industry is fairly dismal.

At the start of 2023 the majority of Wall Street economists predicted that the US economy would fall in to recession in 2023. These are smart, astute and generally well paid economists, but they resoundingly missed the resilient economy of 2023. It would be one thing if this were an aberration but it’s not. Professional forecasters who spend a large part of their working hours trying predict future market and economic outcomes tend to have a predictive track record akin to a coin toss. Economists and analysts serve a variety of purposes at large banks and in government, so this track record doesn’t dismiss their work – but it does suggest that following expert predictions about the future is not a winning investment strategy.

So how do we reconcile the fact that the future is important in long-term investing, but we don’t know with certainty what it will bring? Rather than predict the future, we seek to buy investments at prices that make economic sense and that have low odds of permanent capital impairment. Knowing that the future represents a vast range of potential outcomes, we invest in a diversified portfolio of assets that meet our investment criteria for price, and quality, and is not dependent on a specific outcome for success. This is the classic principal of diversification. We also have a general bias towards businesses with a history of dividend growth. Dividends represent the real cash component of a stock’s investment return (a “bird in the hand”), and companies that increase their dividend regularly provide a “pay raise” to shareholders. Of course portfolios will only include assets that are aligned with a specific client’s objectives, risk tolerance and time frame.

Q1 Asset Class Performance Summary & Q2 Commentary

Domestic Stocks

Year-to-date through 3/31/24

- Large-Cap US stocks (S&P 500) increased 10.6%

- Mid-Cap US stocks (S&P 400) increased 10%

- Small-Cap US stocks (S&P 600) increased 2.5%

We view the risk/reward in broad US equity markets as balanced. While valuations are above their longer-term averages, revenue, earnings and profit margins appear to remain supportive of these valuations. There is an ongoing concentration risk in the market-cap weight indices where seven stocks (The MAG 7) have been responsible for an outsized portion of gains in recent years. This has caused some to compare this period to past market peaks.

But valuations under the surface of the index remain reasonable. Backing out the mega-cap stocks, we see more reasonable valuations and room for a continued broadening out of the market rally to include participation from more large companies (the remaining “S&P 493”), as well as small and mid-sized companies.

International Stocks

Year-to-date through 3/31/24

- Developed International stocks (EAFE) increased 5.7%

- Emerging Market stocks increased 2.1%

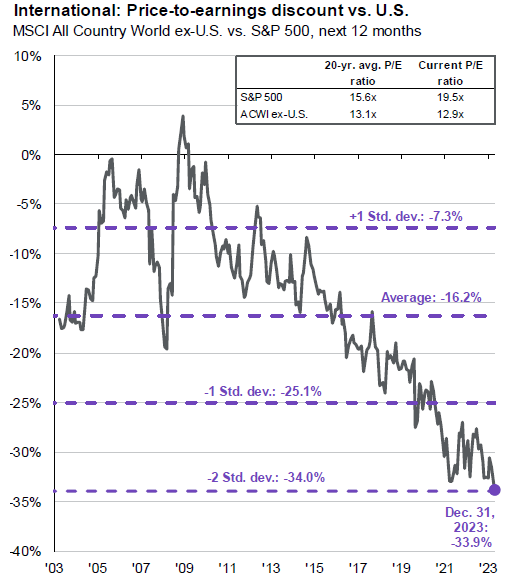

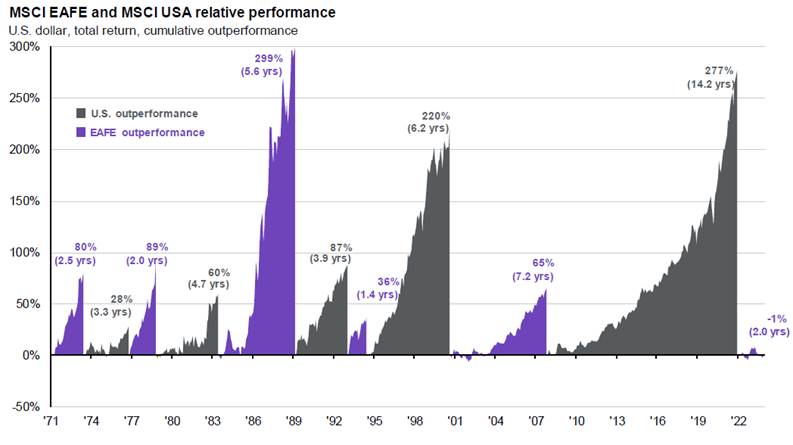

International stocks continue to trade at steep historical discounts to their domestic counterparts (Exhibit D). While there are unique risks associated with international investing, including currency fluctuations and geopolitical concerns, we view the long-term benefits of incorporating these assets in to a diversified portfolio as out-weighing the risks. Domestic stocks have experienced such a long period of out-performance relative to international stocks, that some investors may have forgotten that International stocks also experience long periods of relative outperformance (Exhibit E).

Exhibit D

Source: FactSet, MSCI, Standard & Poor’s, J.P. Morgan Asset Management

Exhibit E

Source: FactSet, MSCI, J.P. Morgan Asset Management

Fixed Income / Bonds

Year-to-date through 3/31/24

- Bonds (Bloomberg US Aggregate Index) declined -0.78%

We continue to favor exposure to shorter-duration fixed income assets including treasuries, treasury inflation protected securities (TIPS), and corporate fixed income. With the rise in interest rates over the last two years, we have added some additional duration via high quality intermediate-term fixed income securities. While higher yields relative to recent history make these securities more attractive at the margin, they are generally more volatile than shorter-term securities. Most of our clients’ fixed income allocation continues to serve a dual purpose of income generation and as a volatility ballast. For this reason we do not see a need to significantly over-weight longer duration fixed income securities at this time. Of course a much higher move in rates could change our thinking here. In addition to traditional fixed income investments, we are also recommending allocations to private collateralized first trust-deed loans. These assets meet our criteria for income generation and low impairment odds, and are available to qualified investors only (details and offering documents available upon request).

Q2 Commentary

Over the preceding decade, investors often bemoaned the stock market’s “addiction to cheap money”, in the form of low interest rates. Following the Great Financial Crisis, the Federal Reserve (“Fed”) maintained a near zero interest rate policy for a most of the period up and through COVID. This easy-money policy included the expansion of their balance sheet via quantitative easing – (e.g. buying government bonds thereby increasing the public money supply). Over this period, worries about Fed policy tightening would periodically spook markets. Concerns that the Fed would go too far in their mini tightening cycle that began in 2015, resulted in a swift market sell-off of 14% over the course of 3 weeks at the end of 2018. This resulted in the Fed Chairman Powell’s famous policy pivot. The Federal Funds rate peaked during that cycle at a mere 2.5%, and a new round of cuts ensued in August of 2019.

The post COVID inflation surge forced the Fed’s hand and they had no choice but to raise rates aggressively in an attempt to contain inflation. This was met with an S&P 500 decline of nearly 25% peak-to-trough in 2022. But since then markets have recovered to near all-time highs, even though the Fed continued to raise rates through the summer of 2023. Until now there have been no rate cuts. Is the market no longer addicted to cheap money? Some may argue that baked-in rate cut expectations are keeping the market aloft. But in January of this year the fed funds futures markets predicted that the Federal Reserve would cut interest rates between 5-6 times in 2024. Now expectations are for 1-2 cuts this year, with some Fed officials suggesting zero cuts in 2024.

So far, markets have remained resilient in the face of evolving rate expectations. We suspect this is in no small part due to the fact that conservative investors and savers are now earning a real return (above inflation) on their risk-free assets. Treasury-bills, CDs and money market funds all pay around 5% at a 1 year maturity. This is the bright side of higher interest rates, and suggests that high rates aren’t all bad for the market and economy. In fact by historical standards, today’s higher rates are near the low side of normal. A real risk-free rate increases the opportunity cost of capital and tempers speculative excess, offers a fair rate of return for conservative savers, and provides room for policy makers to reduce rates during a real economic downturn. We think this is a good thing.

Should you have any questions regarding your investment account(s) and personal financial plans, or if there have been any recent changes to your investment and/or retirement objectives, please do not hesitate to contact our office to speak with one of us at your convenience. We can also provide you with a current copy of our ADV Part 2, at your request.

As always, we thank you for entrusting AMM to help you achieve your investment and retirement objectives.

Your Portfolio Management Team