First published in 1949, Ben Graham’s The Intelligent Investor remains highly influential, especially with Warren Buffett, who regards it as “the best book on investing ever written.” Buffett often highlights the book’s focus on long-term investing and managing market cycles. Graham’s famous insight that “In the short run, the market is a voting machine, but in the long run, it is a weighing machine” illustrates how stock prices, though subject to sentiment-driven fluctuations in the short term, ultimately reflect the true value of a company over time.

One of AMM’s five core principles addresses the importance of valuation. “The price you pay determines your return”. Pay too much for any asset, and you will earn a lower return all else being equal. While value investing is a return seeking endeavor, it separates itself from other investing disciplines by inherently focusing on risk. Graham emphasized the importance of reducing risk rather than just chasing high returns, underscoring his philosophy of a margin of safety.

Most investors that read Graham for the first time tend to have a “light bulb” moment. Rather than chasing the next fad investment, or focusing on predicting the future, value investing provides a disciplined, data-driven framework. By analyzing financial data to estimate intrinsic value, investors can target stocks trading at a discount, building in a margin of safety and potential for gains as the stock price converges with its intrinsic value over time. This also allows investors to identify overvalued stocks to avoid.

Of course, if it were this easy, everyone would be a successful value investor. In practice, value investing is challenging for a variety of reasons:

- Valuing a Business is Hard: Valuing a business is difficult because it involves predicting future cash flows, growth rates, and risk—factors inherently uncertain and affected by countless variables. Even with detailed financial models, small changes in assumptions about revenue growth, discount rates, or profit margins can drastically alter a business’s valuation. Moreover, external factors like competition, economic cycles, regulatory changes, and shifts in consumer behavior add layers of unpredictability. Accurately estimating intrinsic value requires not only analytical skills but also insight into qualitative factors, such as management quality and competitive positioning. This blend of art and science makes valuation a complex and, at times, subjective process, with even experienced analysts often arriving at widely different conclusions.

- Bias and Preconceived Notions: Even if you have the technical expertise to value a business, your biases and pre-conceived notions can influence decision-making in ways that may not align with objective analysis. If you have a positive or negative impression of a company or asset, you might unconsciously seek out information that confirms this view while ignoring contradictory data. For instance, if you believe a tech company is revolutionary, you may overlook signals that it’s overvalued or has business weaknesses.

- Market efficiency: The modern computer did not exist when Graham first wrote The Intelligent Investor. Warren Buffett has mentioned that he used to read 10-K reports (annual reports filed with the SEC) at the public library. Buffett would spend hours reviewing company filings, financial statements, and other investment-related materials to gain a deep understanding of businesses. This kind of financial treasure hunt is far different today. SEC financial reports, and a variety of other material public information are now instantly available online and across various financial data terminals. Moreover, analysts at brokerage firms and investment companies pore over this data and incorporate it almost instantaneously into financial and valuation models.

- Time Frame: Even if your valuation is correct and you make an investment, you may lose faith in the investment if the market doesn’t fully reflect your “correct” value over a reasonable time frame. The saying “Being early is indistinguishable from being wrong” is often attributed to Howard Marks, the co-founder of Oaktree Capital Management and a well-known value investor. Marks frequently discusses the importance of timing in investing, emphasizing that even if an investor’s thesis is correct, entering a position too early can lead to poor results or missed opportunities. This insight underscores that successful investing isn’t just about identifying the right assets or trends but also requires a keen sense of when to act.

- Value Traps: Sometimes, stocks appear undervalued based on financial metrics but are actually struggling due to fundamental problems, making their recovery unlikely. These “value traps” can result in poor returns despite appearing attractive based on traditional value metrics. Buffett is widely considered to have improved upon Grahams valuation philosophy by focusing on high-quality businesses with strong brands, competitive advantages (moats), and durable profitability. In his view, better to pay a fair (but not high) price for a high quality and enduring business franchise, than to pay a discount price for a low quality enterprise.

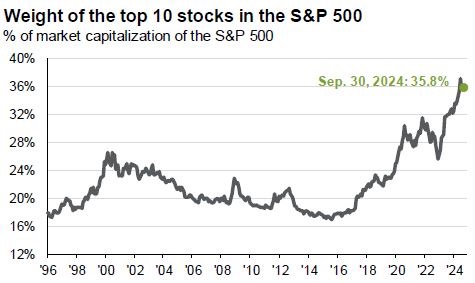

Given the challenges and factors above, it is no surprise that investors big and small have been moving more of their investments to passive index funds. As of May 2024, nearly 60% of the U.S. stock fund market was held by passive index funds. This compares to 6% in 1996 and 21% in 2012. Passive index funds simply buy the stocks in their underlying reference index at the prevailing market price, with no attention paid to the fundamental value of the underlying holdings.

While passive investing has many attributes including simplicity and low cost, there is very little if any risk management in a truly passive strategy. Since most indexes give more weight to the biggest companies in the index, they can become significantly concentrated in only a small number of holdings. In bull markets this may be a feature rather than a disadvantage. Passive index investors will inherently end up with a higher concentration in the top performing stocks. But this feature can become a problem if the most highly concentrated businesses reach bubble valuations. All bubbles eventually pop, and index investors would be left holding the bag.

Exhibit A

Source: FactSet, Standard & Poor’s, J.P. Morgan Asset Management. U.S. Data are as of September 30, 2024

Our purpose here is not to try and predict a market bubble, or to suggest there is not a place for index investing. There are good fundamental reasons that the top stocks today represent such a large portion of the index, and we often use various indexes in portfolio construction. But we are suggesting that a portfolio strategy that is blind to valuation is inherently unstable, and lacks a core component of true risk management. To better balance risks we consider the following in portfolio construction:

- Asset Allocation: Asset allocation is the strategic distribution of capital across asset classes such as stocks, bonds, and real estate to align with our clients individual risk tolerances, goals, and time horizons. This approach helps manage risk by balancing high-risk, high-reward assets like equities with more stable, low-risk assets like bonds, ensuring that the overall portfolio volatility is in line with the investor’s preferences.

- Diversification: Diversification spreads investments across various assets, sectors, or regions to reduce risk. By holding a variety of assets, the impact of any single asset or sector underperforming is minimized. This strategy helps stabilize returns by balancing potential downside with gains in other areas, thus protecting the portfolio from concentration risk.

- Quality: Focusing on quality means prioritizing investments in companies with strong fundamentals—such as solid balance sheets, consistent earnings growth, and strong competitive positions. High-quality companies are generally more resilient during economic downturns and market volatility, reducing the real risk we all strive to avoid — permanent capital loss.

- Valuation: Valuation, even with all the challenges outlined above, continues to play a key role in risk management. By assessing a company’s intrinsic value through methods like discounted cash flow (DCF) analysis or relative valuation metrics (e.g. Price to Earnings, Price to Sales), we can seek to avoid or under-allocate to potentially overpriced assets. Overpaying increases downside risk and reduces long-term return expectations, so maintaining discipline around valuation helps reduce the likelihood of the inherent downside of overpriced assets.

In short, fundamental risk management is of prime importance, and understanding the proper asset allocation, as well as having some reasonable assessment of value can help you construct a more resilient portfolio.

Q3 Asset Class Performance Summary & Q4 Commentary

Domestic Stocks

Year-to-date through 9/30/24

- Large-Cap US stocks (S&P 500) increased 22.1%

- Mid-Cap US stocks (S&P 400) increased 13.5%

- Small-Cap US stocks (S&P 600) increased 9.3%

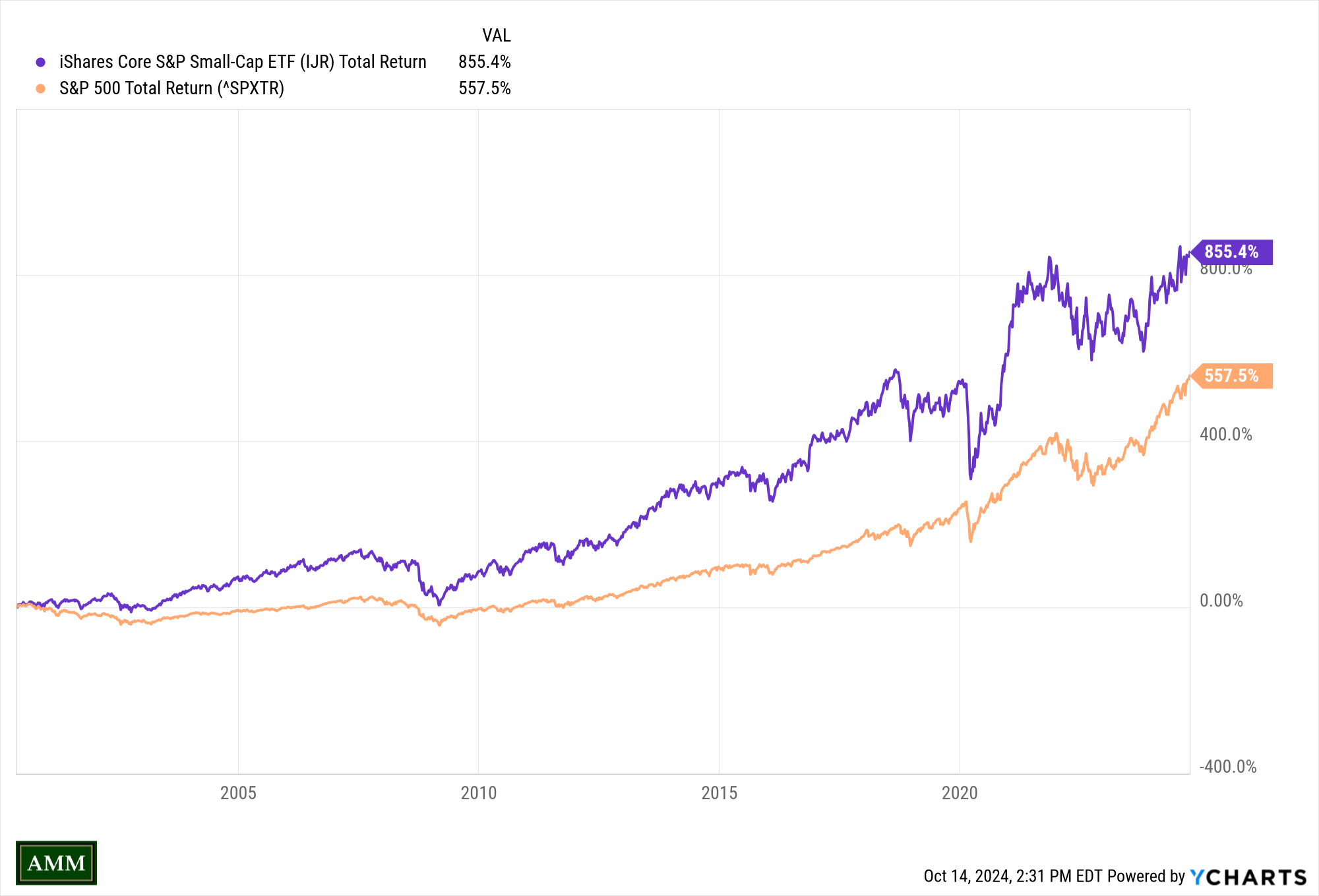

While large high quality domestic companies make up the bulk of our clients’ stock allocation, our research continues to suggest small and mid-cap stocks as an attractive and relatively inexpensive opportunity in the current environment. According to research firm FS Insight, small-cap stocks currently trade at an approximate 40% discount to their large cap peers, while offering higher forward earnings growth. The last time small caps traded at a similar discount to large companies was in 1999. What followed was a long period of small-cap outperformance vs. large companies.

Over very long time periods, small-cap stocks have outperformed large companies (Exhibit B). This makes sense given that these businesses tend to have high growth potential but with a higher degree of risk and uncertainty. Therefore investors should be compensated accordingly. However in the years since the 2008/09 financial crisis, small-cap stocks have mostly underperformed their larger peers. This has been for a variety of factors (anemic economic growth and low interest rates in the twenty teens, the ongoing dominance of mega-cap technology stocks, etc.). We view this opportunistically, and have recently increased small-cap exposure in most client asset allocation oriented portfolios.

Exhibit B

Source: AMM, Ycharts. Data as of October 14, 2024.

International Stocks

Year-to-date through 9/30/24

- Developed International stocks (EAFE) increased 13.0%

- Emerging Market stocks (MSCI EM) increased 16.9%

AMM continues to under-allocate to International Stocks relative to the MSCI All Country World Index. While international valuations may appear relatively attractive, weaker economic and earnings/revenue growth in these markets suggest that their valuation discount relative to the USA is warranted.

Fixed Income / Bonds

Year-to-date through 9/30/24

- Bonds (Bloomberg US Aggregate Index) increased 4.5%

The much anticipated Federal Reserve interest rate cutting cycle began on September 18th, with a .50% reduction in the federal funds rate. The current yield on the ten year treasury note responded in the following weeks by actually rising .50%, instead of falling. While this may seem counter-intuitive, a better than expected jobs report and a spike in forward inflation expectations has suggested further interest rate cuts this year may not be warranted. We continue to allocate a majority of our clients’ fixed income allocations to shorter-term investment grade (corporate and government) fixed income securities with a reduced exposure to interest rate risk.

Q4 Commentary

With Election Day only a few short weeks away, many investors are considering possible portfolio moves ahead of or immediately after the election. According to a recent Investor’s Business Daily article, green/renewable energy stocks should be good for Harris, while traditional oil and gas stocks should do well under Trump. However, making these kinds of investment decisions on expected or actual election results is typically unwise.

First, markets are forward-looking and often already price in anticipated political outcomes. First level thinking like “Clean energy = good for Harris”, and “Oil and gas = good for Trump” ignores both the complexity and forward looking nature of markets. This is the reason for the classic market adage “sell the news”. Second, market movements are more heavily influenced by fundamental economic factors like interest rates, corporate earnings, and global events rather than transient political shifts. Finally, studies have shown that market returns do not consistently favor one political party over another, and the long-term trend of the market has been upward regardless of the party in power.

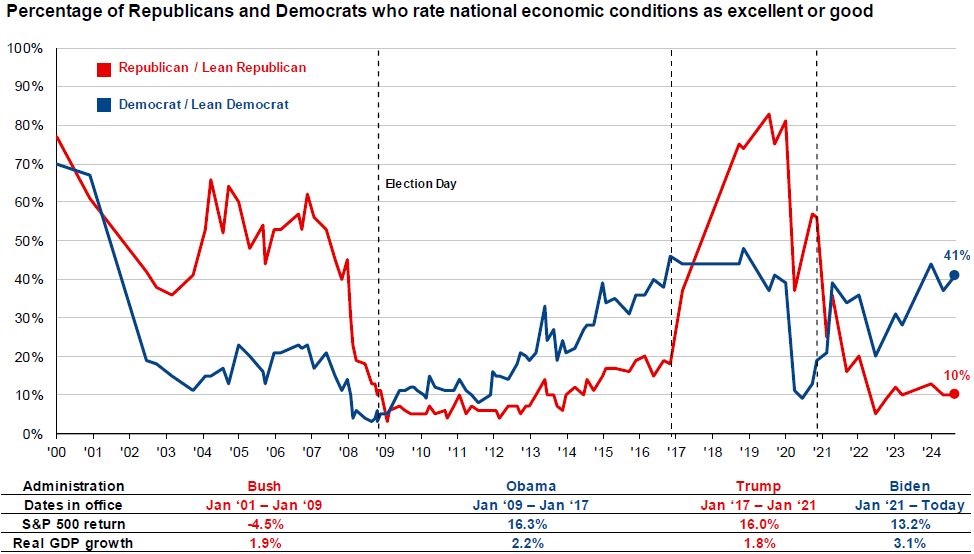

However, election results do seem to affect how one feels about the economy (Exhibit C). It seems entirely natural that a person may not feel great about the economy when their team is out of power. But reacting to these feelings by abandoning an otherwise well-conceived investment strategy is generally a bad idea. Instead, staying the course with a well-diversified, goal-aligned portfolio is generally a more successful strategy than reacting to election cycles, which are often unpredictable and short-lived relative to a long-term investment horizon.

Exhibit C

Source: Pew Research Center, J.P. Morgan Asset Management. U.S. Data are as of September 30, 2024

Should you have any questions regarding your investment account(s) and personal financial plans, or if there have been any recent changes to your investment and/or retirement objectives, please do not hesitate to contact our office to speak with one of us at your convenience. We can also provide you with a current copy of our ADV Part 2, at your request.