Suppose the next time we see you we lay out the following 4 cards in front of you like this.

Then we give you the following statement.

If a card has a vowel on one side then it has an even number on the other side.

Our question to you is what two cards do you need to flip over to prove this statement true?

- A & 4

- A & 7

- D & 4

- D & 7

Did you choose A & 4?

Then you’re like the majority of people, wrong.

People flip over these two cards to confirm the statement. If they flip over the A card and a vowel appears the statement is correct. If they flip over the 4 card and a vowel is on the other side then the statement is also proved correct.

Instead of asking you to prove the statement true, what if we asked you to prove the statement false. Which two cards would you flip over now?

A & 4- A & 7

- D & 4

- D & 7

The answer is A & 7.

Flipping over the A card can confirm the statement but also disprove the statement if an odd number is on the other side. You would flip over the 7 card because you can disprove the statement if a vowel was on the other side.

This test is the Wason Selection Test and it shows our confirmation bias in action.

Confirmation Bias

Confirmation bias is probably the cognitive bias you are most familiar with. It is the process of seeking out information that confirms a previously held belief. We are more than twice as likely to seek out information that confirms and conforms to our opinion than information that contradicts or disproves our opinion.

Only seeking out information that confirms our current opinion is a hindrance to expanding our knowledge base and making a truly informed decision. The blinders caused by confirmation bias can hurt us when investing too.

How can we overcome our confirmation bias?

Think Like a Scientist

The goal of a well-designed scientific experiment is not to prove the hypothesis correct but to try and prove it wrong. Can you reject the null hypothesis? If an experiment can reject the null hypothesis then the scientist might be on to something. It would still require more experiments testing different variables.

You can’t run a controlled experiment with investing like you could in a lab but you should still try to disprove your opinion.

If you are bullish on a particular company, instead of reading every article and research report that confirms how great an investment the stock is, you need to seek out the credible information from reliable sources that claim the opposite.

Can you rationally counter argue the bearish argument and can you back it up with unbiased data?

If you can’t it doesn’t mean you’re wrong. It means you have a new set of questions to answer and research to pursue.

Be Your Own Devil’s Advocate

Argue against yourself.

Come up with at least three data points that you can use to argue the other side of your position. Then actually do the research to back up these arguments. It will force you to think hard about why you could be wrong. Not only does it force you to expose yourself to non-confirming ideas and data but it can strengthen your original opinion and enhance your overall knowledge level.

It is easy to fall in love with a stock. When our initial response to an investment is, “this sounds great” an immediate negative feedback loop should trigger. It should force us to ask, “How are we wrong?” It doesn’t mean we’ll always argue against ourselves effectively and avoid stocks that we shouldn’t own. But it at least forces us to research it further and to come up with a list of reasons why we could be wrong.

If we can’t counter the new data as to why we might be wrong then it tells us that we don’t really understand the business and we should move on to something else.

Also, a list of why we might be wrong can also help us exit a position quicker. If what we think could go wrong starts going wrong then we should sell the position and move onto something else.

Dividend Stock in Focus:

eBay, Inc. (EBAY): $37.84

Price as of the close April 5, 2019

A myth about dividend paying companies is when a company starts paying a dividend it means the company can no longer grow.

The thinking is that if the company has favorable growth projects to invest in then the company will retain all earnings and invest in these projects.

If a company is returning all or part of their earnings to shareholders through dividends then the company no longer has viable growth projects to invest in.

The evidence does not back this up.

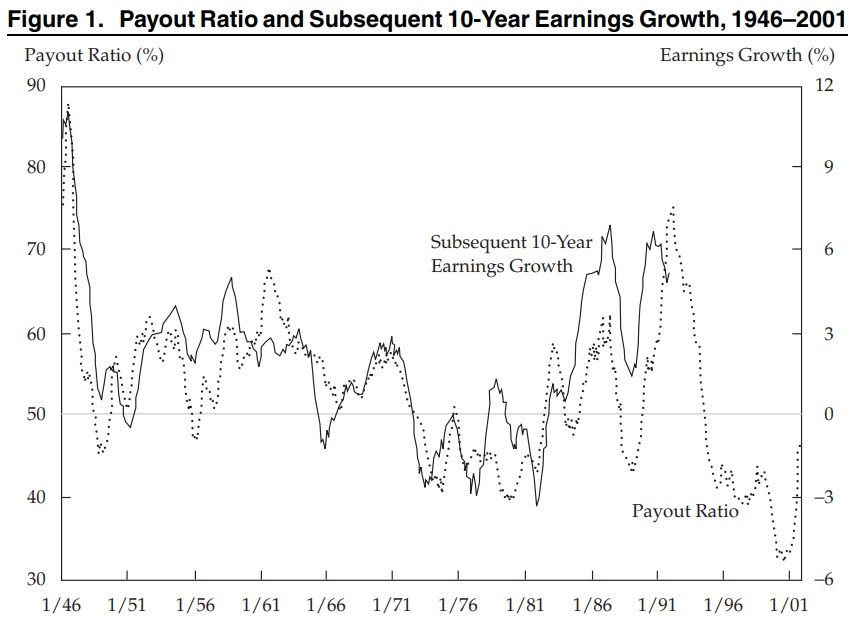

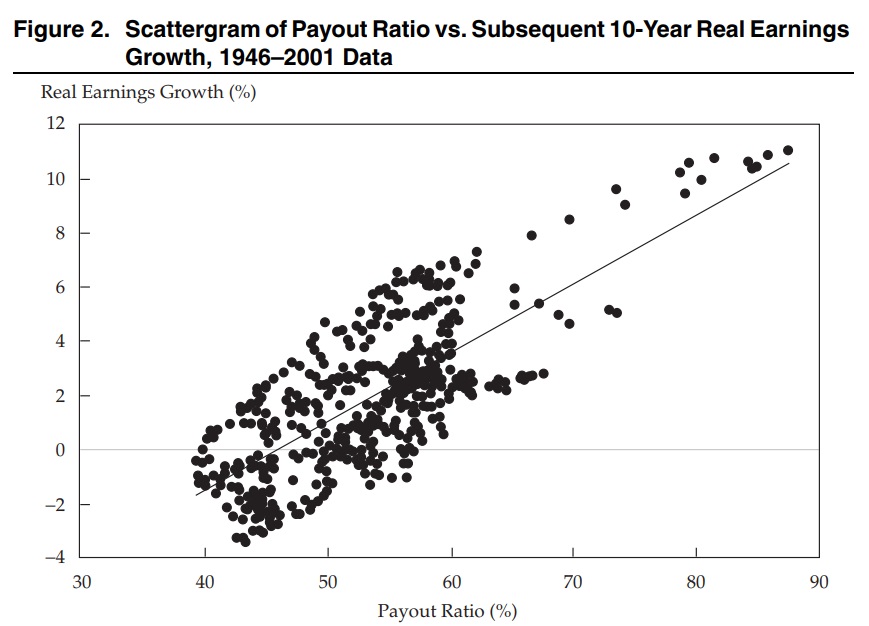

In their 2003 paper Surprise! Higher Dividends = Higher Earnings Growth by Robert D. Arnott and Clifford Asness they show that the more companies pay out in dividends the higher their earnings growth.

And another way to look at it.

There are two main reasons for this relationship.

The first is management loathes cutting a dividend once initiated. Increasing a dividend and increasing the payout ratio is a signal that earnings growth will be higher going forward.

The second reason is capital discipline. Every business has a capital budget for the year. This budget that determines how much capital the company has to invest in new projects. A company that returns some of its capital back to shareholders through dividends is forced to choose the best projects that generate the highest returns on investment and higher growth for the company.

Too much retained capital allows management to venture into empire building and investing in suboptimal projects that make the company bigger, not better.

eBay is guilty of poor capital discipline with investments into non-core businesses like Skype and Rent.com. By not investing and focusing on its core business, eBay missed strong eCommerce growth opportunities that would’ve added significant value.

Although prodded by activist shareholders, eBay’s new dividend policy is a sign that capital discipline is returning. The new policy is a sign that management knows it needs to refocus on improving its core business and seizing the still large opportunities in eCommerce.

Dividend History:

eBay is a New Dividend Payer. They have never paid a dividend until now. In February eBay announced they would start paying a quarterly dividend of $0.14 per share. This equates to an annual yield of 1.47% based on today’s price.

A reason why we like new dividend payers is the company starts its dividend at a low payout ratio to its earnings. As management and the board gets comfortable with the idea of paying a regular dividend they tend to raise their dividend at above-average rates. We expect New Dividend Payers to grow their dividend at 10-20%.

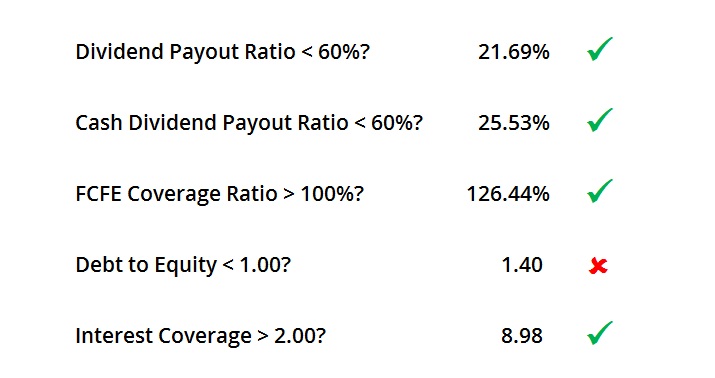

Dividend Safety:

eBay’s new dividend policy is well covered by its earnings and its free cash flow to equity (FCFE). eBay’s low payout ratio and high free cash flow to equity coverage ratio is a positive sign for potential above-average dividend growth.

Our only concern would be the debt to equity ratio. A company with too much debt has to divert cash flow to servicing that debt instead of paying it back to shareholders via dividends. Given eBay’s interest coverage ratio of 9x, its debt level is not a concern.

Catalysts for Dividend Growth & Capital Appreciation:

Activist Shareholder

eBay’s announcement that they were going to start paying a dividend initially peaked our interest. We’ve followed eBay for some time now. They own some very valuable assets. They also used to own PayPal before shareholder agitation forced them to spin off PayPal. The agitating shareholders felt that PayPal’s value was underappreciated as its potential was being overshadowed by eBay.

eBay currently owns StubHub the leading ticket reseller in the U.S. It also owns a very attractive collection of online classified businesses. Like PayPal the true value of these two assets are being overshadowed by eBay’s marketplace business. This may be coming to an end.

Elliott Management and Starboard Value are large hedge funds that have the asset size and the clout to agitate for change. Elliott Management owns 4% of eBay and they released a letter outlining what they want eBay to do. Starboard Value wants the same.

Elliott Management wants eBay to spin-off or sell both StubHub and its Classifieds Business. We think the odds of one or both spin-offs occurring is high.

eBay spun-off PayPal due to previous shareholder pressure. eBay initiated a new dividend because of the pressure from Elliott Management. Both Elliott Management and Starboard Value gained board seats and eBay’s management announced a strategic review of its business. Spinning off or selling the two businesses is also the right thing to do for shareholders. StubHub and the Classifieds Business are worth more on their own than as a part of eBay.

The following is mostly a confirmation of what Elliott Management outlined in their presentation Enhancing eBay

StubHub

At first glance, StubHub’s business of reselling tickets looks like it fits in with eBay’s core business. Early in the partnership eBay’s balance sheet and capital investments helped StubHub grow. StubHub could invest more aggressively in their platform and eBay’s backing helped StubHub close some big deals like its partnership with Major League Baseball. But after these early wins, the synergies trailed off.

eBay was hoping the two platforms would benefit further from cross promotions. StubHub is really good at reselling tickets and that should be its only focus. What products from eBay’s marketplace do you cross promote to a Cannibal Corpse ticket buyer? You can promote a used t-shirt of the band but then you’re that guy wearing a t-shirt of the band you’re about to see.

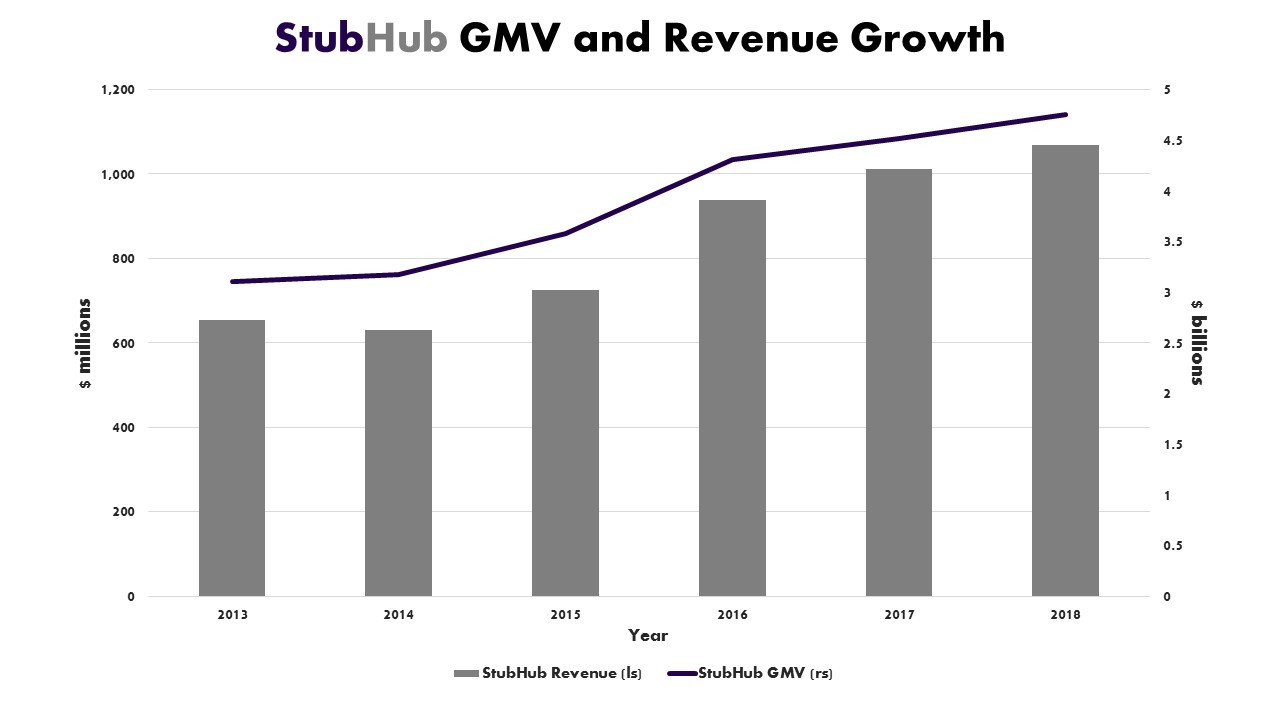

Two key metrics for StubHub’s business is Gross Merchandise Volume (GMV), the total dollar amount transacted on their platform, and Take Rate, the amount per transaction that flows into StubHub’s revenue.

Since 2013 GMV has grown from $3.1 billion to $4.75 billion, a compound annual growth rate of 8.4%.

During this time StubHub’s take rate has floated between 22-23%. Revenues have grown from $629 million in 2013 to $1.068 billion at the end of 2018, a compound annual growth rate of 11.17%.

Data from eBay’s SEC filings

StubHub’s EBITDA margin based on similar competitors and its business model should be around 30% at the minimum. Which means StubHub accounted for $320.40 million of eBay’s 2018 EBITDA. Based on management’s expectation of 6% growth in 2019 this means StubHub should produce about $339.62 million in EBITDA. Using a comparable Enterprise Value to EBITDA ratio of 14x, StubHub in 2019 is worth $4.754 billion and accounts for $5.50 per share of eBay.

StubHub probably operates at a higher EBITDA margin and it would likely command a higher EV/EBITDA ratio given its growth, margin profile, scale advantages, and its attractiveness as an acquisition target for Private Equity or for a company like Live Nation (LYV).

Classifieds Business

The most intriguing asset that eBay owns is its online Classifieds Business.

The most profitable section for newspapers in the pre-digital age was the classified section. Instead of paying a sales force to go out and find businesses to advertise in your newspaper, advertisers called you. Newspapers would charge high rates in relation to the ad size. The Internet has changed where we find classified ads but it hasn’t changed how profitable they are.

The classified section for newspapers was so profitable because they had local monopolies. If you wanted to sell your used car, your unexpected litter of kitten, or your “like new” Nordic Track in San Diego you had to place a classified ad within the Union-Tribune. With the advent of the internet age, you can place your ad anywhere but classified ad monopolies still exist because of network effects.

An online classified business only works if it can connect the most sellers with the most buyers. This creates a strong direct network effect.

The direct network effect occurs when the usage of a product or service by any user increases the product or service’s value for other users. The more people that sell their goods or services on a classified site increases the value for those looking to buy that good or service.

Once an online classified business has built a network effect it is hard to dethrone them. Look at Craigslist, it hasn’t changed much since 1999.

An online classified business requires very little reinvestment back into its business to maintain its leading position. This leads to very high returns on invested capital and returns on incremental invested capital.

eBay’s classified business holds an almost monopoly like position, more than 80% market share, in 10 countries.

Image from eBay’s investor presentation

Classified businesses come in two forms, horizontal and vertical.

A horizontal classified is just like the old classified section of the newspaper. It covers a wide range of categories: jobs, places to rent, services, used cars for sale, etc. A modern example would be Craigslist.

A vertical classified is focused specifically on one category like RV Trader or Motorcycle Trader. eBay’s classifieds group contains both horizontal and vertical classified businesses.

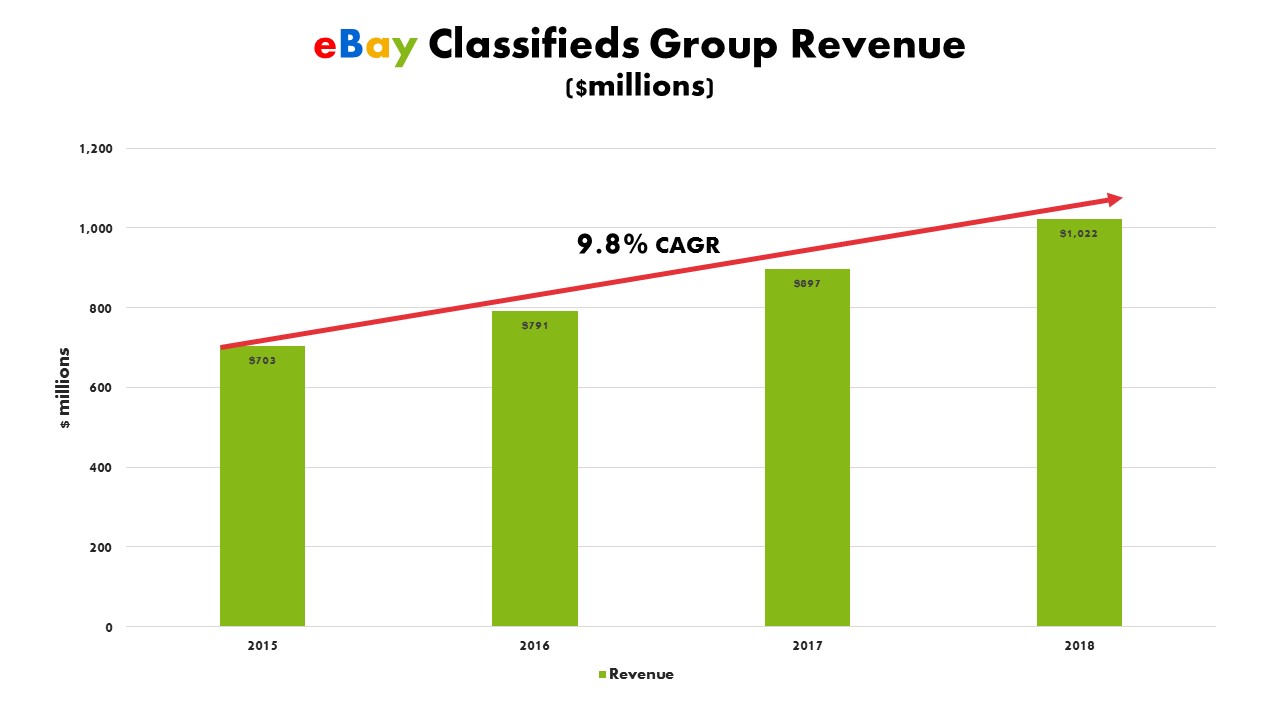

eBay’s Classifieds Group has been growing its yearly revenue at a compound annual growth rate of 9.8%.

Data from eBay’s SEC filings

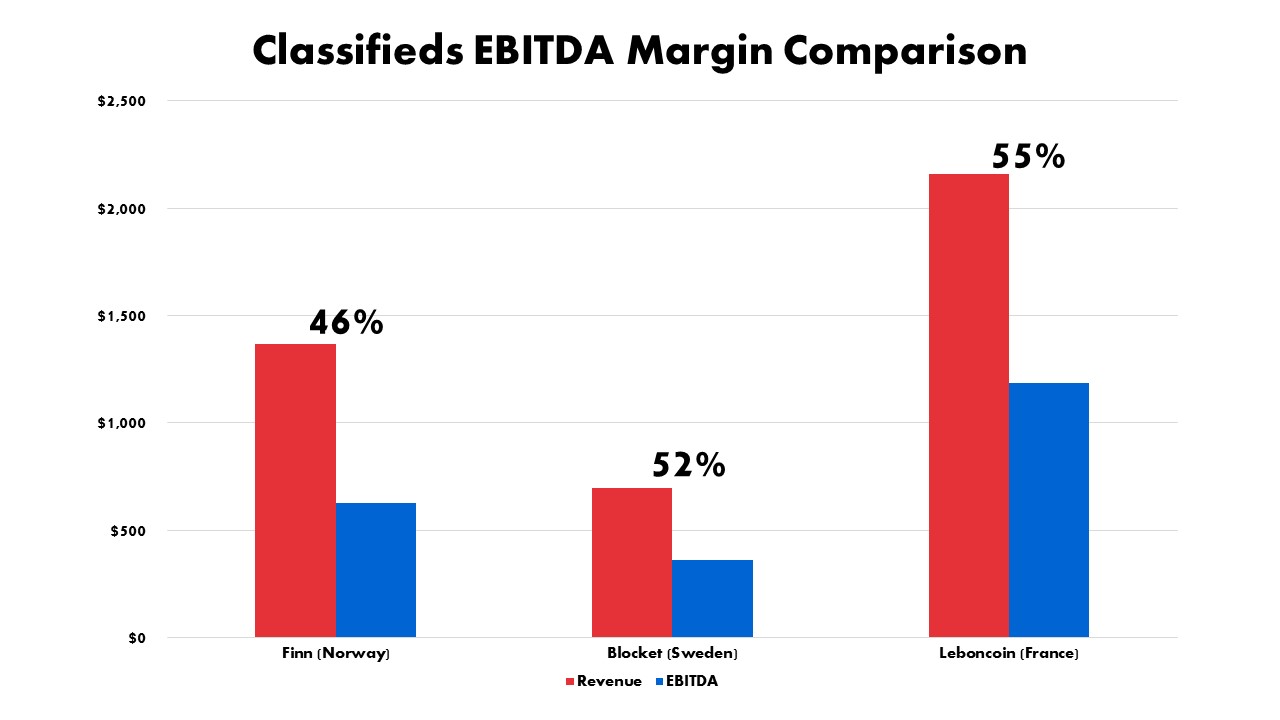

eBay doesn’t break out its Classifieds Business’s operating margins but we estimate its EBITDA margins should be around 45%. The chart below shows the margins for three Online Classified businesses. They are all single country horizontal classified businesses. All three are in developed Western countries and are the leading online classified company in that country. All are very similar to eBay’s collection of classifieds business.

The issue with this comparison is all three are owned by Schibsted and it could be a case of managerial and operational excellence that is leading to the high margins.

Data from Schibsted’s investor presentation

The EBITDA margin for all of Schibsted’s classifieds business is 33% because of its recent investments in new opportunities that haven’t reached the same margin profile as its more established platforms like the three below.

We estimate eBay’s Classifieds group will generate $505.89 million EBITDA in 2019. Using an EV/EBITDA multiple of 16x, we value eBay’s Classified Business at $8.1 billion or $9 of eBay’s current share price.

We think the Classifieds Business is a prized asset and would probably trade at a higher multiple if spun-off or attract a premium offer from a company like Schibsted.

Core Marketplace

The perception – given its market valuation – is eBay’s core marketplace business is an impaired business. The truth is eBay is a leading global eCommerce business usually right behind Amazon and even ahead of Amazon in a few countries.

Despite its poor marketplace perception eBay’s core marketplace continues to grow.

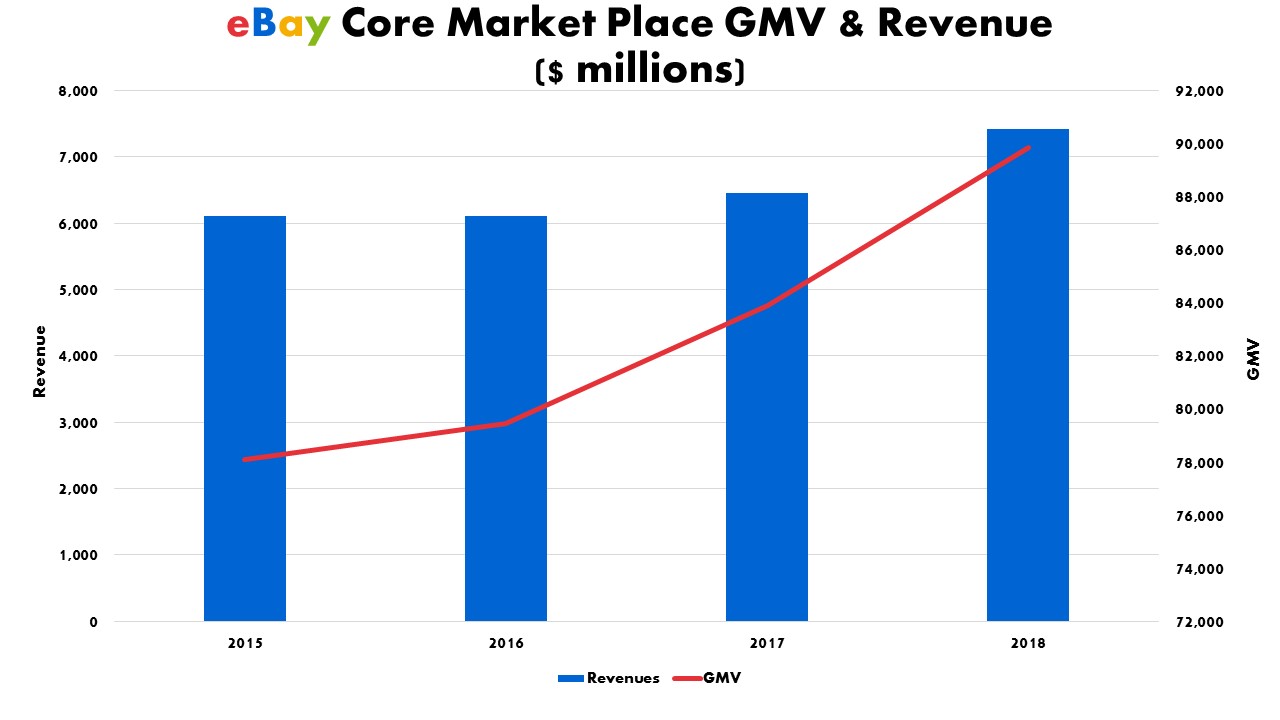

Since 2015 eBay’s GMV has grown at a compound annual growth rate of 3.56% and its revenue has grown at a compound annual growth rate of 5%.

Data from eBay’s SEC filings

While the core marketplace business is not impaired, it has not matched its closest competitors.

eCommerce is a global secular trend and eBay, a leading eCommerce business, should be benefiting a lot more from this trend. eBay’s closest competitors sure are.

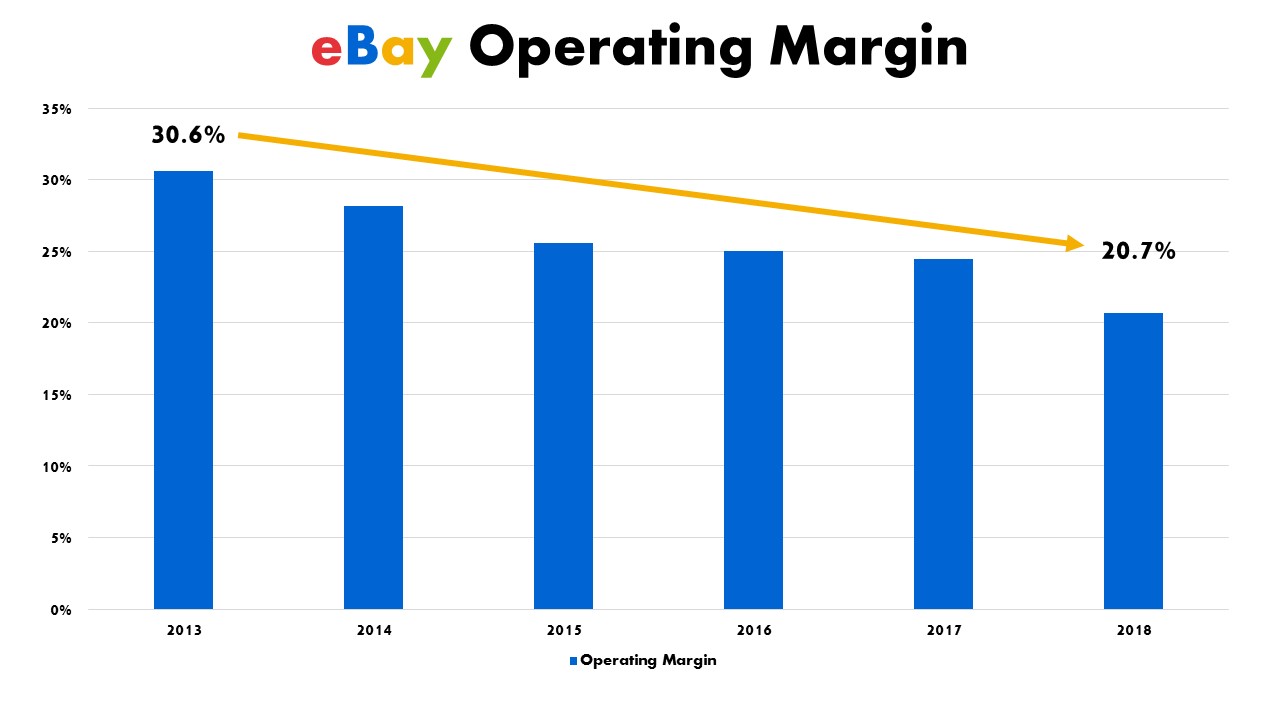

Part of the underperformance has been operational/technical. Another part has been management’s lack of focus on improving and expanding its core marketplace business.

In the past management has been sidetracked with investments in Skype, Magento, and Rent.com while missing out on niche eCommerce opportunities. This lack of focus allowed eBay’s cost structure to increase leading to deteriorating operating margins.

Data from eBay’s SEC filings

The good news for eBay is that the eCommerce trend is still in its early stages. eBay has a lot of opportunities to expand its core marketplace business while reducing excess operational costs and expanding its margins.

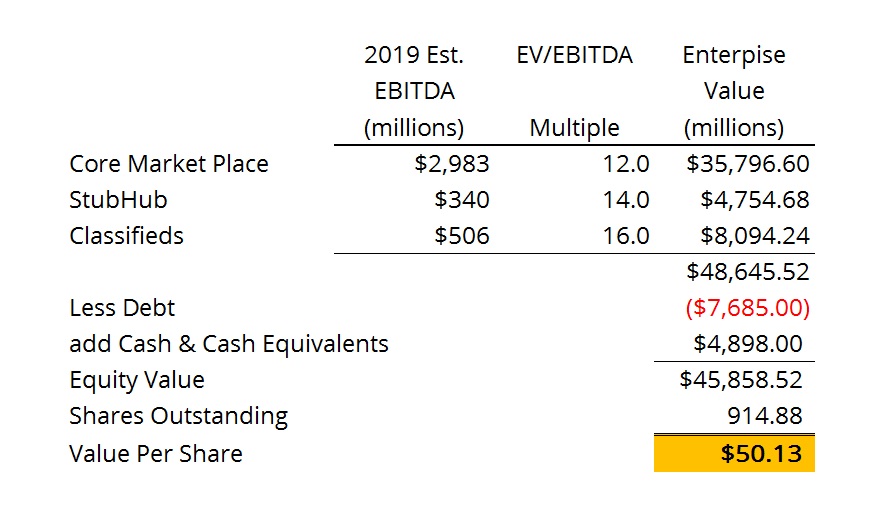

When we back out the EBITDA and enterprise value of StubHub and the Classifieds Business from eBay we’re left with $2.84 billion in EBITDA that is expected to grow 5% in 2019 and an Enterprise Value of $25.459 billion. The market is valuing eBay’s remaining core market place business at a 9x EV/EBITDA multiple. We think the core marketplace should trade at least at a 12x EV/EBITDA multiple to its expected 2019 EBITDA which gives us an enterprise value of $35.8 billion.

A more complete sum of the parts valuation in the Valuation section

If management can trim costs, expand margins, and grow its revenue higher than 5% then eBay’s core marketplace should command a higher EV/EBITDA multiple and a higher value per share.

Pre-Mortem (Potential Risks to our Thesis):

No Spin Off or Sale

The crux of our thesis is that eBay spins off or sells both StubHub and its Classifieds Business. If after its strategic review, eBay decides to keep both businesses then the catalysts for unlocking the value in eBay in the near term are gone.

The inherent value in all three businesses can still be revealed but it would likely take a much longer process. In the short-term eBay’s stock price would probably sell off as event-driven investors close their positions and other disappointed investors sell their positions too.

Given eBay’s track record of listening to activist shareholders and pursuing value enhancing transactions, e.g. PayPal spin off, we think the odds of eBay backtracking are low.

Also, Elliot Management and Starboard are activist investors known for fighting hard to get their way. In 2012 Elliot Management seized an Argentinian naval ship in Ghana to get Argentina to pay the money it owed Elliott on a 2001 Argentinian bond.

Weak Core

The other main aspect to our investment thesis is that eBay’s core marketplace business is worth more than what the market is currently valuing it at.

It will be up to current management to show the market that they are focused on cutting costs and expanding their margins. Their recent efforts to switch the merchant of record from PayPal to Ayden is a step in the right direction.

The merchant of record is the intermediary between the buyer and seller on eBay. When it was PayPal the buyers would pay PayPal and then PayPal would pay the seller. PayPal takes 3.5% from the buyer and pays a 1% fee to the merchant bank of the acquirer. The spread between the two is PayPal’s profit.

eBay’s new partnership with Ayden allows eBay to become the payment intermediary. The spread will tighten but instead of all the value from the spread going to PayPal, eBay will now earn most of it.

The Ayden deal should also lower costs for eBay and the sellers on its platform. Improving the overall marketplace platform experience will help eBay enhance its direct network effects.

Valuation:

We value eBay using a sum of the parts analysis.

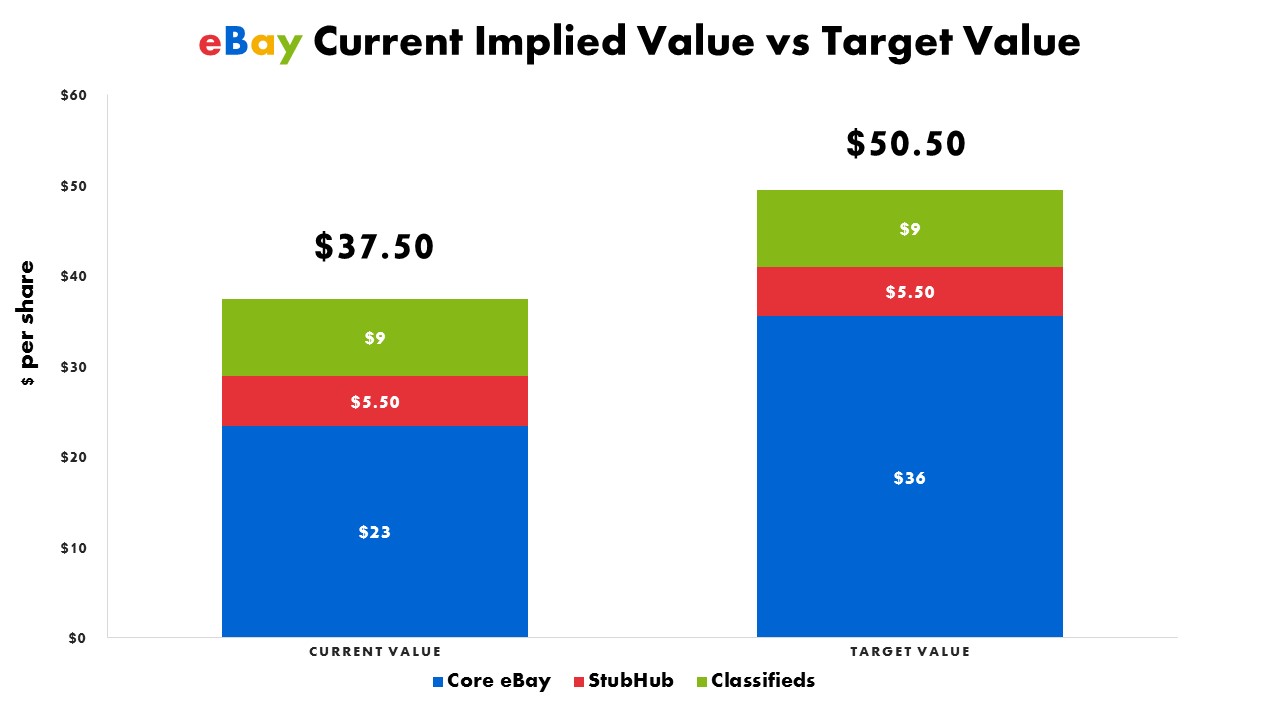

We value StubHub at $5.50 per share of eBay today and we value its Classifieds Group at $9 per share.

When we back out the 2019 estimated EBITDA from StubHub and the Classifieds Group we’re left with $2.983 billion in EBITDA for the core market place. This means eBay’s core business is being valued at 9x EV/EBITDA which is around $23 per share. A very low multiple for a company still growing, with high margins, and high returns on invested capital.

If we give eBay’s core market place a multiple of 12x EV/EBITDA, still well below its peers, then the core business is worth $36 per share and all of eBay combined is worth $50 per share. A 31.5% premium to eBay’s current trading price.

This is our base case.

If after spinning off or selling StubHub and its Classified business, management improves the core marketplace’s growth rate and its operational efficiency then the core eBay marketplace deserves a higher multiple and is worth much more.